For investors seeking a clear market signal, the last few weeks have been frustrating at best. So far this year, the main stock indexes are down – the S&P 500 has fallen just over 7%, while the NASDAQ is still in correction territory, with a 12% year-to-date loss. However, the market bounced back starting last week. We saw a week of solid gains that saw stocks make a strong rebound from their low points. The result: for the month of March, the S&P is up 3.9%, while the NASDAQ has gained 3.3%.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

This kind of volatility among conflicting long- and short-term trends makes it difficult for the average retail investor to make sense of what’s going on. What’s needed is a clear lead that will cut through the market’s signal confusion.

One strategy is to follow the insiders. These are the corporate officers who combine and ‘inside’ view of company ops with accountability to shareholders and boards for bringing in profits. They know what’s likely in store for their companies – and they’ll trade company stock on that knowledge. To keep the field level, governmental regulators require them to regularly publish their trading activity. The result is a mine of solid data for investors willing to dig into it.

We’ve gotten that digging started, using the TipRanks Insiders’ Hot Stocks tool to look up three stocks that have ‘Strong Buy’ ratings from the Wall Street analysts along with significant ‘informative buys’ from the insiders. Let’s take a closer look.

Aspen Aerogels (ASPN)

First up is Aspen Aerogels, an industrial technology company specializing in aerogel insulation products. Aerogels are a light-weight, high-end, multi-use product, in which liquid-filled pore space has been filled with gas, resulting in a solid with ultra-low density that retains structural strength while showing remarkably low thermal conductivity ratings. Aerogels have found uses in construction, in LNG storage, and in petrochemical refining – and more recently, in the EV battery manufacturing niche.

That last is worth a look. EVs – electric vehicles – are clearly a ‘coming thing,’ and they are benefiting from both societal and government pressures for expanded production and use. Aspen’s aerogel technology brings several advantages to battery makers, including a valuable combination of low weight and high energy density, along with passive fire resistance.

Looking into Aspen’s financial performance, we find that the company reported strong revenues and weak earnings in its most recent quarterly, for 4Q21. At the top line, Aspen showed $31.5 million revenues, up 36% since the year-ago quarter. This gain did not translate into EPS, which declined from a 23-cent loss one year ago to a 50-cent loss in the recent Q4. The company’s share price didn’t seem to react to the EPS loss. Aspen’s stock is up ~43% since the 4Q21 report was released.

Some other factors to consider are the company’s overall 21% gain in annual revenue year-over-year, to $121.6 million, and its selection of a location for its second US manufacturing facility.

Looking at the insiders, we find that Board member Robert Gervis made the most recent ‘informative buy’ – and his purchase demands notice. Gervis spent $4.5 million to purchase 135,870 shares in the company. He now holds a stack in Aspen worth over $7.6 million.

Gervis is not the only one bullish here. This stock is covered by Eric Stine, 5-star analyst with Craig-Hallum, who believes that the company’s technological application in the EV industry is the key to its growth.

“With each passing day, we believe it becomes more obvious that the light-duty passenger vehicle market is going electric, with ASPN a top name for us and critical to the adoption ramp. Despite being deeply engaged with OEMs across the automotive industry, we believe that ASPN still remains a relative unknown to investors and an under-the-radar electrification name but think this will change as 2022 progresses,” Stine explained.

Stine rates ASPN shares a Buy, with a $65 price target that suggests room for ~75% growth in the coming months. (To watch Stine’s track record, click here)

Overall, Wall Street finds itself in broad agreement with the bullish view on Aspen; the stock’s 7 recent reviews are all positive, for a Strong Buy consensus rating. The shares are selling for $37.06 and their $56.43 average price target implies ~52% upside from current levels. (See ASPN stock forecast on TipRanks)

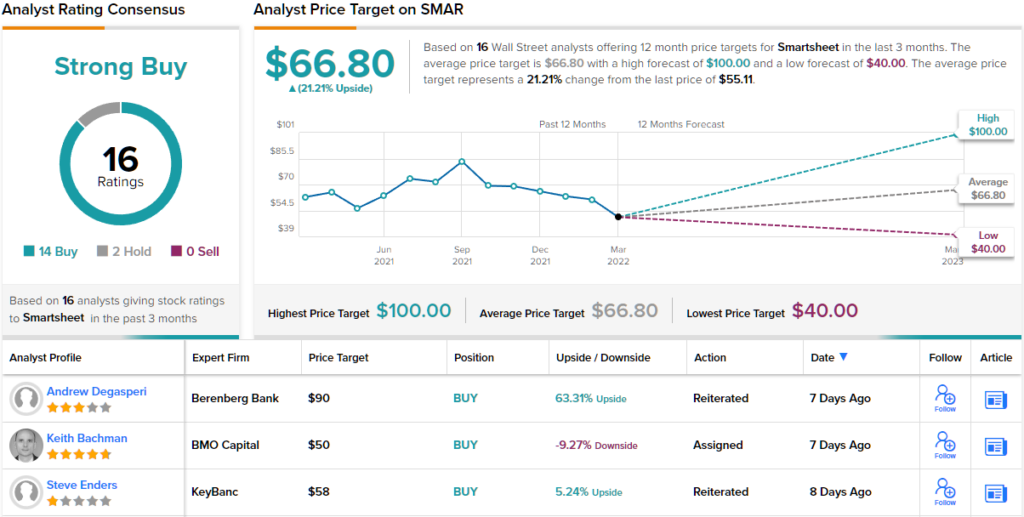

Smartsheet (SMAR)

Next up is Smartsheet, a cloud-based software firm offering products to enchase workspace management and collaboration – a product line with clear applications and advantages in today’s white-collar office environment. Smartsheet’s platform is available to enterprise customers on the SaaS model, and can handle tasks ranging from content collaboration to resource management to integrations and multiple views to administration. The company counts approximately four-fifths of the Fortune 500 firms in its customer base.

While SMAR shares were falling through much of February and March, the stock got a boost on March 15, with the fiscal 4Q22 report. The report showed that the business continues to grow – Smartsheet reported its eighth consecutive quarter of sequential revenue growth. The Q4 top line of $157.4 million was up 43% year-over-year.

Looking forward, the company guided toward fiscal 1Q23 revenue between $162 million and $162 million, which would represent y/y growth of 38.5%, in line with expectations. Smartsheet is predicting 36.5% revenue growth for 2023 as a whole, with a year-end top line between $750 million and $755 million.

Smartsheet has a strongly positive insider sentiment, pushed that way by two sizable recent transactions. Paul Porrini, the Chief Legal Officer Emeritus, spent $309K buying 32,500 shares, while Matthew McIlwain, of the Board of Directors, spent $496K on a total of 10,000 shares.

Berenberg analyst Andrew DeGasperi was impressed by Smartsheet’s growth, and it guidance toward continuing that pace. He writes of the company’s prospects: “We believe Smartsheet is a market-leading platform, yet it only has 0.6% of global knowledge workers as users. We believe Excel, the primary work/project management platform, is ill suited to meet the increasing needs of a collaborative workplace environment… Given the nascent market, we believe Smartsheet has a significant opportunity to grow its user base. We believe Smartsheet’s high dollar-based net revenue retention ratio, growing customer base, and economics of its platforms will drive demand.”

These comments support DeGasperi’s Buy rating on the stock, while his $90 price target implies a one-year upside of ~63%. (To watch DeGasperi’s track record, click here)

Tech stocks tend to attract a lot of attention, and Smartsheet is no exception – the stock has 16 share reviews on record, and they include 14 Buys against just 2 Holds to give the company its Strong Buy consensus recommendation. The shares have an average price target of $66.80, indicating room for 21% growth from the current price of $54.99. (See SMAR stock forecast on TipRanks)

Kezar Life Sciences (KZR)

We’ll wrap up with a clinical-stage bioscience researcher, Kezar Life Sciences. This company is involved in the fields of oncology and immunology, and is developing new treatments for cancers and autoimmune diseases. The company’s pipeline features first-in-class small molecule drug therapies with activity in protein degradation and protein secretion.

Kezar’s pipeline features two clinical-stage drug candidates, KZR-261 and zetomipzomib. The first of these has recently advanced from the discover stage and the company has initiated a Phase 1 open-label dose-escalation study. The drug candidate is being studied as a potential treatment for solid tumor cancers.

The real excitement for this company comes from the two Phase 2 trials of zetomipzomib. This is an autoimmune drug, under investigation as a treatment for Lupus, among other conditions. The company in December released interim results from its MISSION trial of zetomipzomib, showing that the drug candidate demonstrated clinically meaningful benefits in patients suffering from Lupus nephritis. The patient pool was small, only 5, but 4 patients showed positive results. In addition, the drug continued to show a ‘favorable’ profile for safety and tolerability, extended over 6 months. Top-line data from the MISSION trial expected in 2Q22.

Kezar also has the PRESIDIO trial ongoing, investigating zetomipzomib against active dermatomyositis (DM) or polymyositis (PM). The Phase 2 trial is described as a ‘randomized, placebo-controlled, double-blind, cross-over clinical trial,’ and has enrolled 24 patients. Topline data from PRESIDIO is also expected in the second quarter of this year.

Kezar also shows a recent ‘million +’ insider trade. Franklin Berger, of the company’s Board, made a purchase worth $1.299 million earlier this week. His buy totaled 80,000 shares, and it brought his stake in Kezar up to an impressive $14.28 million.

This stock has also attracted the notice of H.C. Wainwright analyst Raghuram Selvaraju, who points out that the multiple upcoming catalysts are a strong inducement for investors. Selvaraju writes, “In our view, positive data for zetomipzomib from both the MISSION and PRESIDIO trials ought to establish Kezar as a triple-threat across SLE/LN, DM and PM and position the compound for advancement into late-stage clinical development. Depending upon the strength of the data, Kezar might also ultimately be considered an attractive potential acquisition target, in our opinion.”

These comments are used to back up a Buy rating on the stock, and Selvaraju’s $22 price target indicates potential for ~22% upside this year. (To watch Selvaraju’s track record, click here)

Overall, this stock has a unanimous Strong Buy consensus rating based on 4 positive reviews. The shares are selling for $18.05 and the average price target, at $20.50, suggests ~14% upside from that level. (See KZR stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.