Since bottoming out in early summer, shares of SoFi Technologies (NASDAQ:SOFI) have been on an excellent run, surging 77%. Despite this strong performance, the stock is only up 12% year-to-date, underscoring a generally mixed sentiment toward the neo bank in 2024.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Citi analyst Andrew Schmidt, however, firmly sides with the bulls. Schmidt is not entirely surprised by SoFi’s recent gains, viewing the stock’s upward trend as a natural response to the company’s strengths.

“We think recent momentum in the stock is justified, owing to an improving 2025 setup, particularly as it relates to upside potential improving refinancing/debit consolidation trends,” Schmidt opined.

But with the company readying to announce Q3 results on Tuesday (October 29), will investors see continued upside, or might the stock face renewed challenges?

Of course, that remains to be seen but ahead of the print, Schmidt strikes a generally positive tone, expecting the readout will reflect “another solid quarter for SoFi, and we are modestly above consensus overall.”

For the second half of 2024, Schmidt anticipates ongoing GAAP profitability and a gradual increase in overall loan sales. Although due to shifting expectations on interest rates the analyst has slightly reduced his forward projections, Schmidt believes SoFi can continue to capture market share and maintain deposit growth. “Furthermore,” he goes on to say, “the steady cross-buy success should also continue, in our view, resulting in growing originations as well as financial products over time.”

Schmidt also thinks SoFi’s $2 billion loan platform agreement with Fortress, which provides referral fee revenue for loans directed to origination partners, offers a “potentially lucrative off-balance opportunity.” However, Schmidt also notes that he would be keen to learn more about the profit-sharing terms within the agreement, as well as which party retains ownership of the customer relationship.

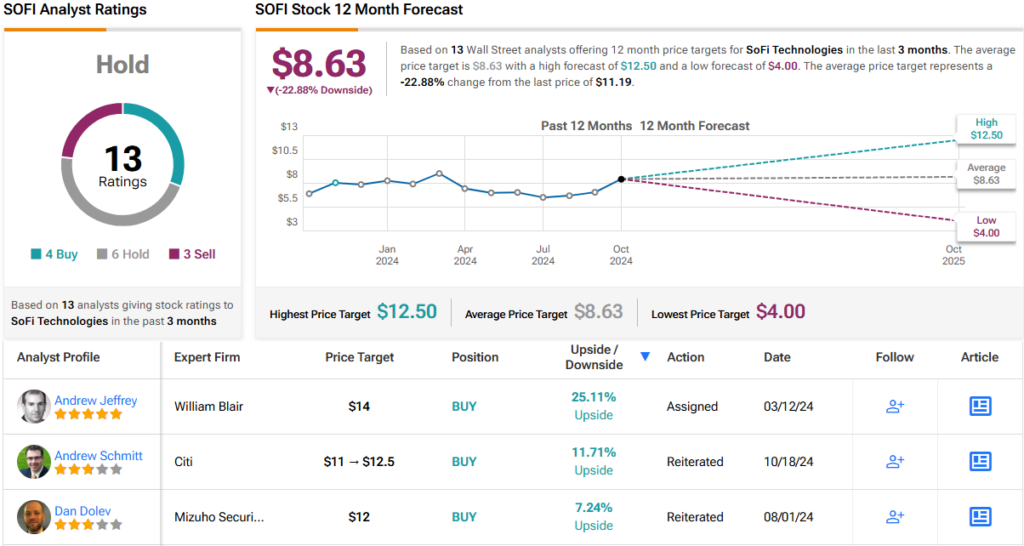

Bottom line, Schmidt rates SoFi shares a Buy, while raising his price target from $11 to $12.5, suggesting the stock will climb ~12% higher over the coming months. (To watch Schmidt’s track record, click here)

The rest of the Street is less confident, however; based on 4 Buys, 6 Holds, plus 3 Sells, SOFI stock has a Hold consensus rating. Moreover, the recent gains have taken the stock beyond what most consider its fair value; at $8.63, the figure represents a possible downside of ~23% over the next 12 months. (See SoFi stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.