On the surface, everything seems to be going well for homebuilding specialist Toll Brothers (NYSE:TOL). Despite a tough environment for the housing sector and the economy overall, Toll beat earnings expectations in its latest earnings report. That should have put its shares on solid ground. Instead, the bears attacked the company. Therefore, I am bearish on TOL stock due to the worrying disparity between expectations and outcomes.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Toll Beats, Yet TOL Stock Stumbled

On May 21, the homebuilder disclosed its results for the second quarter of Fiscal Year 2024. Earnings per share landed at $4.55, handily beating analysts’ consensus view of $4.14 per share. According to TipRanks reporter Vince Condarcuri, the beat “included a $1.17 per share boost related to the sale of land to a commercial developer.”

That’s an interesting point because, without this sale, EPS would have slipped to $3.38. It’s quite possible that investors took this into consideration and penalized TOL stock accordingly.

Another element to consider is the revenue profile. Against the prior-year quarter, Toll’s revenue expanded by 6% to hit $2.65 billion. As Condarcuri noted, Toll delivered 2,641 homes at an average selling price of $1 million thanks to what management referred to as a “resilient economy.” In addition, the chronically low supply of available residential units lifted demand.

Nevertheless, analysts had targeted revenue of $2.66 billion. Therefore, the homebuilder technically posted a mixed performance for Q2. Still, the sharp decline in TOL stock following the earnings print was curious. Contextually, the consumer economy has been wrestling with sticky inflation and elevated interest rates. By logical deduction, people at large simply don’t have the funds to acquire big-ticket items.

Providing evidence for this assessment is the EV sector. During the worst of the COVID-19 pandemic, EV sales soared amid short supply, skyrocketing demand, and government stimulus checks. Now that circumstances have steadily returned to normal, companies in the electric mobility space are competing aggressively with each other.

If the consumer economy were so robust, you wouldn’t anticipate a sector price war. Yet, that’s exactly what we’ve seen in recent years.

Obviously, EVs and residential real estate represent two completely different categories. However, the point is that if consumers have difficulty acquiring the cheaper of the big-ticket item, it’s doubtful that they collectively have the resources to pile into new homes.

Watch the Labor Market for Clues

If you listen to what I would term housing apologists, they insist that a sector crash isn’t likely to happen. That’s because foreclosure rates – while slowly rising – remain well below levels seen during the runup to the 2008 financial crisis and subsequent Great Recession. However, investors should be careful about using this narrative to pile into TOL stock.

To be clear, I’m not calling for a housing crash. However, a correction would not be out of the question. Indeed, it would be strange if a correction did not occur. The recent volatility in TOL stock likely reflects the market’s anticipation of a downside move.

No, it’s not all doom-and-gloom conspiracy stuff. Rather, it’s about following the logic. According to the U.S. Bureau of Labor Statistics, the agency outlined 20 occupations with the highest projected growth rate between 2022 to 2032. When filtered for median pay, computer and information research scientists won out with an average salary of $145,080 per year.

Coming in second were software developers at $132,270 per year, followed by physician assistants at $130,020. Looking at the list, it’s clear that, for the most part, if you want to earn enough to be able to afford a home, you need to be in tech or healthcare.

We have two problems. First, big tech companies have continued to lay off their workers this year. Plus, math and science in one country are the same as in any other country. With so much focus on remote work, enterprises can easily outsource their tech needs to developing nations for pennies on the dollar.

Second, unhappiness in the healthcare sector is rising. A report late last year indicated that nearly half of all health workers want to quit their jobs. Taken together, this framework implies that homebuilders have a lower addressable market than many realize. Thus, TOL stock could end up paying the toll.

Technical Assessment Points to a Dilemma

Technical analysis as a discipline is a tricky subject due to a lack of standardization and vulnerability to open interpretation. Assessing what a chart pattern looks like is akin to a Rorschach test. People see what they want to see.

On the other hand, the market price is the ultimate arbiter. And right now, TOL stock is telling investors that despite the underlying company beating earnings amid major economic challenges, it needs to be valued 6% lower than it was the previous week.

Interestingly, TipRanks shows that the overall technical consensus for TOL stock based on a one-day reading sits at Neutral. That’s not exactly an attractive signal, especially amid the aforementioned economic challenges.

Is TOL Stock a Buy, According to Analysts?

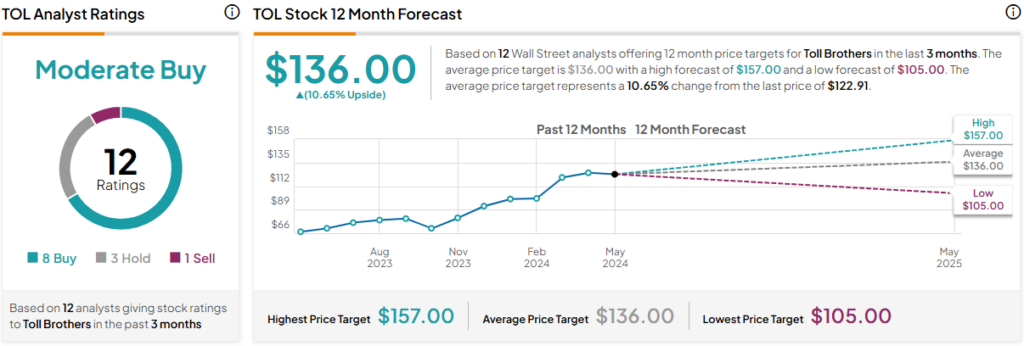

Turning to Wall Street, TOL stock has a Moderate Buy consensus rating based on eight Buys, three Holds, and one Sell rating. The average TOL stock price target is $136.00, implying 10.65% upside potential.

The Takeaway: Sustainability Concerns May Have Brought Down TOL Stock

Although Toll Brothers may have beaten earnings expectations for its Fiscal Q2 report, TOL stock suffered, likely due to a fading addressable market. Primarily, concerns center on labor. Essentially, the fastest-growing jobs that command salaries large enough to buy homes are in tech and healthcare. Unfortunately, these sectors face significant challenges, potentially leading to fewer highly compensated workers. That’s not great news for TOL, which is reflected in its pensive technical profile.