I am bullish on Teladoc Health (TDOC) as it has a strong competitive position within the telemedicine industry, a very strong growth outlook, reasonable valuation multiples, and substantial upside potential relative to its average price target.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Teladoc Health, founded in 2002 and headquartered in the United States, is a multinational virtual healthcare company that has set the ball rolling in the telemedicine industry with clients in approximately 130 countries.

The company is a global leader in the innovative healthcare products sector with numerous high-profile clients, including Aetna, Blue Cross Blue Shield, and United Healthcare.

In this article, we will list two reasons why we are bullish on TDOC stock at current prices

Early Mover & Massive Scale Advantages

Teledoc has been continually increasing its clientele among several market segments in the healthcare industry. If it continues on the same trajectory, the company is expected to achieve a revenue target of $2.6 billion in 2022. The increasing reliance on telemedicine products has enhanced revenues for Teladoc.

Its extensive client base entails over 37 million active users around the globe. Among these clients, a significant chunk comes from the Fortune 500 businesses, followed by small enterprise businesses and a network of almost 300 hospitals. A significant percentage of its revenue is earned through cross-selling products to an existing customer base.

The company has been making it easier for patients and healthcare professionals to access virtual visits through its platforms. Additionally, since there are high barriers to entry, not many businesses can enter the telemedicine market. As a result, Teledoc will likely continue to be a leader in the market for many years to come.

Teladoc’s strengths have been fueling strong growth momentum. For example, in its most recent earnings release, the company boasted solid year-over-year growth in the fourth quarter of 2021 at a rate of 45%.

For the full fiscal 2021, revenue growth was a whopping 86%. Total visits increased by 41% to $4.4 million, and the company’s basic and diluted per share net loss was also reduced from $3.07 in Q4 2020 to $0.07 in Q4 2021 as it scales rapidly towards profitability. The adjusted EBIDTA also increased significantly with a year-over-year increase of 53%.

Discounted Stock Price

TDOC stock looks attractively priced at the moment. Its EV/EBITDA ratio is very low relative to its history at 32.09 compared to its historical average of 106.7.

With a lengthy growth runway ahead of it (EBITDA is expected to grow at a ~35% CAGR over the next five years), TDOC could generate outstanding total returns over the coming half-decade.

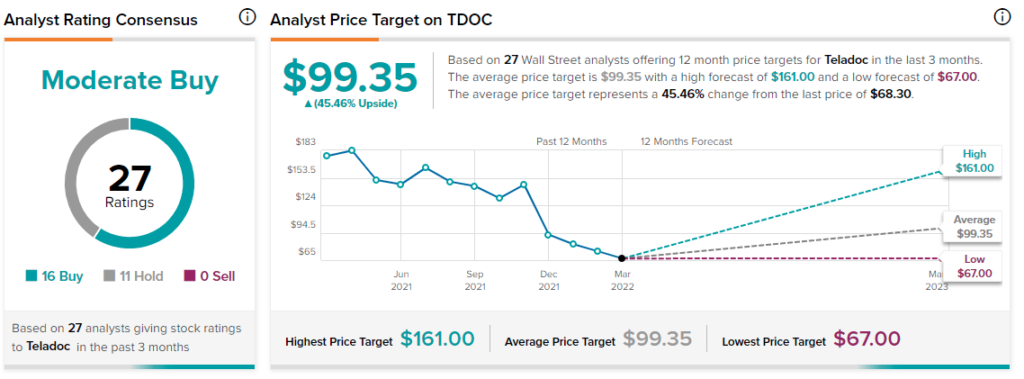

According to Wall Street analysts, TDOC earns a Moderate Buy analyst consensus based on 16 Buy, 11 Hold, and zero Sell ratings in the past three months. Additionally, the average analyst TDOC price target of $99.35 puts the upside potential at 45.5%.

Summary and Conclusions

Teladoc Health operates in a high-growth, high-upside, and disruptive industry. There are few industries with more inefficiencies than healthcare, making it a very attractive industry to disrupt.

Furthermore, given that healthcare is deemed an essential service for the well-being of society, TDOC’s mission to improve the quality and efficiency of healthcare is a noble one, giving investors a potential double bottom line that could include profits and improving mankind’s way of life.

Best of all, analysts are generally bullish on the stock, the average price target implies massive upside over the next year, and the valuation multiples look quite cheap compared to growth rates and historic valuation multiples.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure