Anyone shopping for a used car lately may have considered buying from Carvana (CVNA), home of the car vending machine.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

With good reason, too; the company was up 13.3% in premarket trading on Monday, and kept those gains going into Monday’s session.

I can’t help but look at the macro environment, and the last 12 months of Carvana performance. I’m bearish as a result, and think that Carvana has quite a ways to go before it can make any real headway.

The last 12 months for Carvana started off nicely, but quickly turned sour. In the space between August 2021 and today, the company fell from just over $370 per share to just over $42 per share.

The latest news gave Carvana a shot in the arm. The company offered up a forecast for 2023 that saw “significant core earnings” ahead, and also offered insight on its plans to cut costs. The company plans to reduce spending on advertising and expansion efforts.

It will do so gradually, cutting the budget each quarter until it hits $50 million in the fourth quarter. It will then hold at that level for each quarter thereafter.

Wall Street’s Take

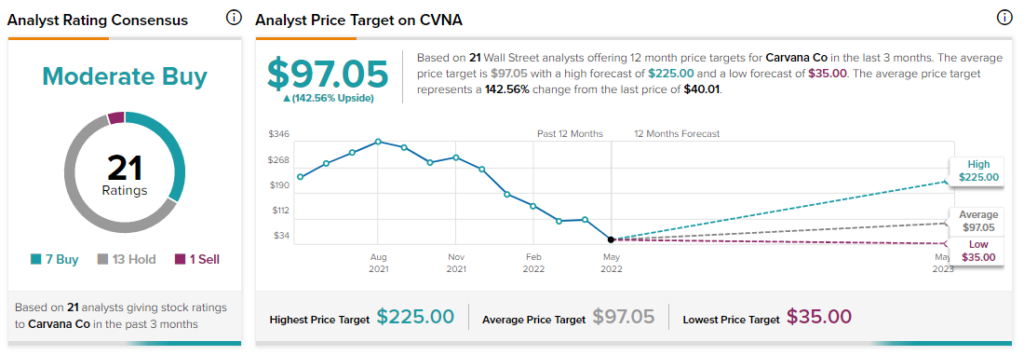

Turning to Wall Street, Carvana has a Moderate Buy consensus rating. That’s based on seven Buys, 13 Holds, and one Sell assigned in the past three months. The average Carvana price target of $98.89 implies 142.6% upside potential.

Analyst price targets range from a low of $35 per share to a high of $225 per share.

Investor Sentiment, on Average, is Awful

Carvana may have a plan for recovery, but it will have to go a long way to convince investors. Right now, Carvana has a Smart Score of 1 out of 10 on TipRanks, which puts it in the lowest class of “underperform.” It is the lowest Smart Score a company can receive.

That’s a sentiment echoed throughout the investor sentiment metrics. Hedge funds, based on the latest word from the TipRanks 13-F Tracker, have all but completely abandoned the company. In the space between December 2021 and March 2022, hedge funds went from owning just over 15 million shares to owning just under 600,000 shares.

Insider trading is almost completely selling transactions. In the last three months, sell transactions led buy transactions 26 to three. In the last 12 months, meanwhile, that ratio expands to 267 sell transactions to 17 buy transactions.

About the only bright spot for Carvana investor sentiment comes from retail investors, at least those who hold portfolios on TipRanks. In the last seven days, portfolios containing Carvana stock have risen 2.7%. In the last 30 days, it’s up 7.6%.

Cost-Cutting

The universal equation for profitability has not changed in centuries. Decreasing expenses, while increasing or maintaining revenue, yields increased profitability. The good news here is that Carvana is definitely working on reducing its expenses.

Well, sort of. The company did announce a “workforce reduction” of 2,500 employees just about a week ago. The problem is, about that same day, Carvana announced plans to spend $2.2 billion to pick up KAR Auction Services Inc.’s wholesale vehicle auction operations, Adesa U.S.

Worse, however, came with an email leaked by a Reddit post. Said post detailed some of the other macro issues facing the company. Carvana noted:

- Inflation and interest rates are up.

- Supply chains are badly disrupted.

- Consumer and investor sentiments have shifted.

All of these together combine to produce an absolutely terrible field for anyone selling used cars. Record high prices, fewer cars than ever, and buyers much less willing to buy because they can’t afford it. Right now it is absolutely a seller’s market for used cars.

I checked the Kelley Blue Book figure on my own car and discovered, after owning it for three years, it’s almost worth what I paid for despite years of depreciation.

How is a seller’s market terrible for sellers? Simple; eventually buyers stop showing up. They know they can’t get anywhere because the available supply is so low that they have to pay inflated prices to get a car.

It’s the same story with the housing market right now, though there are signs that’s turning around. Used car buyers are putting off those purchases until the market evens out, and that means a further hit to Carvana likely to come.

Concluding Views

Carvana is priced at a bargain-basement level, but it’s about to go into a macroeconomic field that is pretty much a disaster for the entire industry.

There are some signs that Carvana may well end up a meme stock. Just last Thursday, the company gained 25%. Trading was halted several times. With almost one in three Carvana shares sold short, that opens up some noteworthy possibilities all its own.

However, I’m bearish on the company. It’s experiencing conditions that probably won’t improve in the short term.

That means the company likely still has farther to fall.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure