Home goods retailer Williams-Sonoma, Inc. (WSM) smashed earnings expectations driven by accelerated customer demand for entertaining and home furnishings needs. Shares popped 4.2% in extended trading on Wednesday.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The company reported earnings of $2.93 per share, increasing 296% year-over-year, and outpacing the Street’s estimate of $1.83 per share.

Revenue climbed 41% to $1.75 billion from the year-ago period and surpassed analysts’ estimates of $1.52 billion.

Williams-Sonoma is the world’s largest digital-first, design-led and sustainable home retailer.

Year-over-year, comparable brand revenue grew 40.4%, including Pottery Barn growth of 41.3%, West Elm growth of 50.9%, Williams Sonoma growth of 35.3%, and Pottery Barn Kids and Teen growth of 27.6%. (See Williams- Sonoma stock analysis on TipRanks)

Laura Alber, President, and CEO of the company said, “As we look ahead, we are confident in our runway for growth and profitability. The goals we have set are driving incremental growth faster than anticipated… We are the only home furnishings retailer that’s able to serve customers at scale online and provide the experience and convenience of physical retail with exclusive sustainable products – giving us the unique advantage to gain share for many years to come.”

Based on favorable macro trends, the company now forecasts Fiscal 2021 net revenue growth in the low double-digit to mid-teen range, increased from the earlier outlook of mid-to-high single-digit revenue growth.

Following the company’s strong Q1 performance, Wells Fargo analyst Zachary Fadem lifted the price target to $180 (from $175) while maintaining a Hold rating on the stock. This implies 5.1% upside potential to current levels.

“In our view, the home furnishings’ bonanza continues; and these results provide further evidence that WSM’s design-forward model is resonating with consumers and taking robust share in a period featuring elevated demand, stimulus benefits, and a customer base that remains largely at home,” Fadem said.

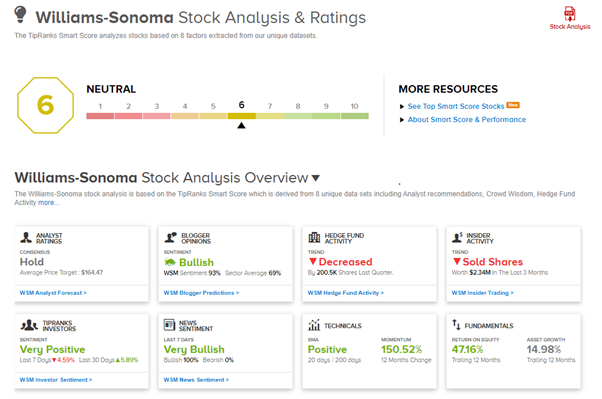

The stock has a Hold consensus rating based on 7 Buys, 8 Holds, and 3 Sells. The average analyst price target of $166.53 implies 2.8% downside potential to current levels. Shares have gained 66.4% year-to-date.

According to TipRanks’ Smart Score system, William-Sonoma gets a 6 out of 10, which indicates that the stock is likely to perform in line with market averages.

Related News:

Snowflake Reports Better-than-Expected Q1 Revenue, EPS Miss; Shares Dip

Columbus McKinnon Delivers Solid Q4 Results; Provides Upbeat Guidance

Bed Bath & Beyond Partners with DoorDash to Expand Same-Day Delivery