Tesla (NASDAQ:TSLA) stock fell 4% on Tuesday as investors pulled money from high-growth tech names following a hotter-than-expected inflation report. Rising oil prices tied to Middle East tensions also added to concerns that inflation could remain elevated for longer, pushing Treasury yields higher and increasing fears that the Federal Reserve may keep interest rates elevated well into next year.

Claim 55% Off TipRanks

Looking for exposure to SpaceX & Anthropic? Check out AGIX ETF

The pullback also comes after an enormous run in Tesla shares during recent months, leaving valuation back at the forefront of Wall Street discussions. One analyst who still believes Tesla deserves a premium valuation, while also suggesting expectations may already be approaching aggressive territory, is Piper Sandler analyst Alexander Potter.

Potter recently published a revamped version of his “Definitive Guide” for Tesla, expanding his valuation framework to include 17 separate business lines ranging from insurance and Supercharging to robotaxis and Full Self-Driving subscriptions. According to the analyst, Tesla’s existing businesses alone can support a valuation near $400 per share, while investors are receiving Tesla’s Optimus humanoid robot ambitions almost for “free” at current levels.

Potter acknowledges his 2026 and 2027 estimates sit below Wall Street consensus forecasts due to weaker deliveries and lower regulatory credit contributions. Yet, the analyst argues investors are becoming far more focused on robotaxi adoption and Full Self-Driving progress than traditional automotive metrics, saying that “historically relevant metrics are growing less important.

While Potter assigns TSLA a $500 price target, he does not believe Tesla stock deserves valuations far beyond that level unless projects such as Optimus become massive commercial successes. As noted above, Tesla’s existing businesses justify about $400 per share in the analyst’s view, meaning the remaining $100 in his target reflects future opportunities tied to humanoid robots and other AI-related initiatives. Potter also acknowledged that forecasting products capable of transforming labor markets and global economic activity remains highly speculative, though he added that valuing those opportunities at only $100 per share may be far too low for some investors, a conclusion he said he is “inclined to agree” with.

Despite the valuation debate, Potter remains bullish on Tesla’s long-term outlook and continues to assign TSLA shares an Overweight (i.e., Buy) rating. (To watch Potter’s track record, click here)

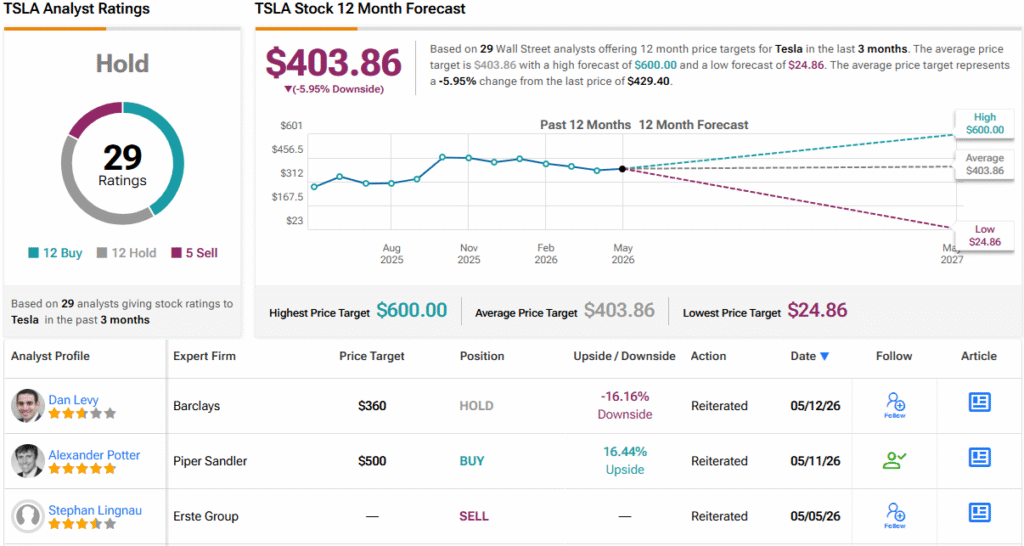

11 other analysts are also TSLA bulls, but with an additional 12 Holds and 5 Sells, the consensus view is that TSLA is a Hold (i.e., Neutral). Going by the $403.86 average price target, a year from now, shares will be changing hands for a 6% discount. (See TSLA stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.