SoundHound AI (NASDAQ:SOUN) shares fell 11% in Thursday’s after-hours session after the company reported mixed quarterly results. While the voice AI company delivered another quarter of strong sales growth, investors appeared far more concerned about continuing losses, acquisition-related costs, and uncertainty surrounding the company’s organic growth.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The market reaction also reflects a broader shift taking place across the AI sector this year. Investors have become far more selective about companies spending aggressively while profitability remains distant, particularly when acquisitions play a large role in driving revenue higher. SoundHound has spent the past year expanding through deals, including its acquisition of Amelia AI and its planned purchase of LivePerson, moves designed to broaden the company’s reach across enterprise conversational AI markets.

For the quarter, SoundHound posted a non-GAAP loss of $0.06 per share, missing Wall Street expectations by $0.02. Revenue climbed 51.7% year-over-year to $44.2 million, beating consensus estimates by $1.64 million. Management also reaffirmed its full-year 2026 revenue outlook of $225 million to $260 million, compared to analyst expectations of approximately $232.8 million.

Investor David Jagielski believes the company’s growth story looks less convincing once acquisitions are taken into account. Jagielski warns that “an easy way for a company to expand its top line is to acquire other businesses,” while arguing that “what’s ultimately most important for growth investors is how well the business is growing, organically, not just due to acquisitions.”

Jagielski thinks SoundHound’s dealmaking activity has made it more difficult for investors to evaluate the company’s actual momentum. The investor points out that “acquisitions have muddied the picture growth story for SoundHound AI,” because they have boosted revenue figures in ways that may not reflect the company’s true underlying expansion.

While the company has delivered strong revenue growth over recent years, Jagielski says that “its actual quarterly growth rate has fluctuated considerably from one period to the next,” something that may raise concerns about consistency and long-term execution.

Profitability also remains a significant concern in Jagielski’s view. The investor argues that “profitability… remains elusive for SoundHound AI,” while adding that continually buying businesses “add costs and complexities along the way,” making it more difficult for the company to improve its financial position anytime soon.

According to Jagielski, investors now want more than revenue growth from AI companies, particularly after speculative enthusiasm surrounding the sector cooled this year.

Although Jagielski does not dismiss the company’s long-term potential entirely, he remains cautious regarding the stock’s near-term outlook.

“There’s no rush to buy the stock, as a wait-and-see approach with SoundHound AI may be appropriate,” Jagielski summed up. (To watch Jagielski’s track record, click here)

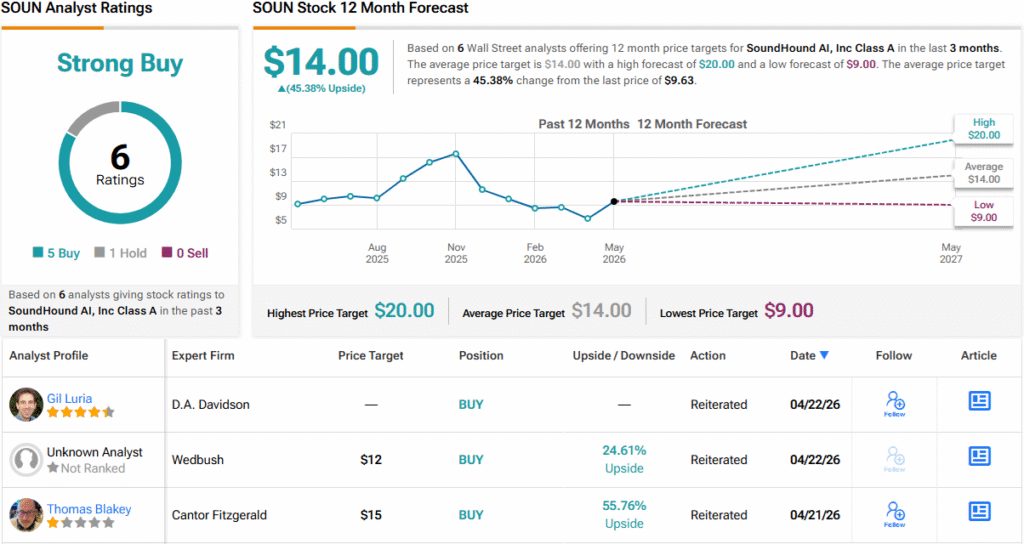

While Jagielski prefers to stay on the sidelines for now, Wall Street has not lost confidence in SOUN. The stock still carries a Strong Buy consensus rating based on 6 recent analyst reviews, with 5 recommending Buy and just one remaining on the sidelines. Analysts currently see the shares climbing to an average price target of $14 over the coming year, representing potential upside of about 45% from Thursday’s closing price. (See SOUN stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.