Rivian Automotive (NASDAQ:RIVN) shares edged about 2% lower in after-hours trading Thursday, as investors weighed a better-than-expected first-quarter report against ongoing losses and the near-term costs tied to scaling production of the upcoming R2 vehicle.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

From an operational standpoint, performance remained relatively steady. Rivian produced 10,236 vehicles and delivered 10,365 during the quarter, broadly in line with recent trends, while maintaining its full-year 2026 delivery outlook of 62,000 to 67,000 units.

Revenue came in at about $1.38 billion, rising 11.3% year over year and topping expectations by roughly $10 million. On the bottom line, Rivian reported a GAAP loss of $0.33 per share, which was $0.39 better than the Street had anticipated. Still, profitability remains a work in progress, with adjusted EBITDA at around -$472 million as the company continues to invest in scaling its operations.

Liquidity declined modestly but remains solid. Rivian ended the quarter with approximately $5.4 billion in total liquidity, down from about $6.1 billion at the end of 2025. Ongoing support from strategic partners and recent capital inflows should help fund the R2 ramp and broader growth plans.

However, one investor, known by the pseudonym ValueAnalyst, won’t be paying too much attention to these financials.

“I recommend ignoring all headlines related to top-line and bottom-line beats and misses and instead focusing on any specific data and management commentary around the ongoing R2 production ramp,” counsels the investor.

Calling the R2 the “path to salvation,” ValueAnalyst agrees with Rivian bulls who are placing their hopes and dreams on its potential success. However, the investor also argues that big questions regarding its performance – i.e., mileage and price tag – won’t become fully known until late 2027.

That means that its true demand and profitability will remain opaque for quite some time, leaving RIVN exposed to short interest and volatility for the better part of two years, predicts ValueAnalyst. As evidence of this dynamic, the investor points out that more than 11% of Rivian’s outstanding shares are currently held in short positions.

Moreover, ValueAnalyst worries that Rivian’s market capitalization is a shade too optimistic, seemingly discounting any production risks with the R2 ramp. That’s further reason the investor is content to sit this one out.

“The optimism regarding the R2 program (is) already embedded in the $20 billion market cap,” concludes ValueAnalyst, who rates RIVN a Sell. (To watch ValueAnalyst’s track record, click here)

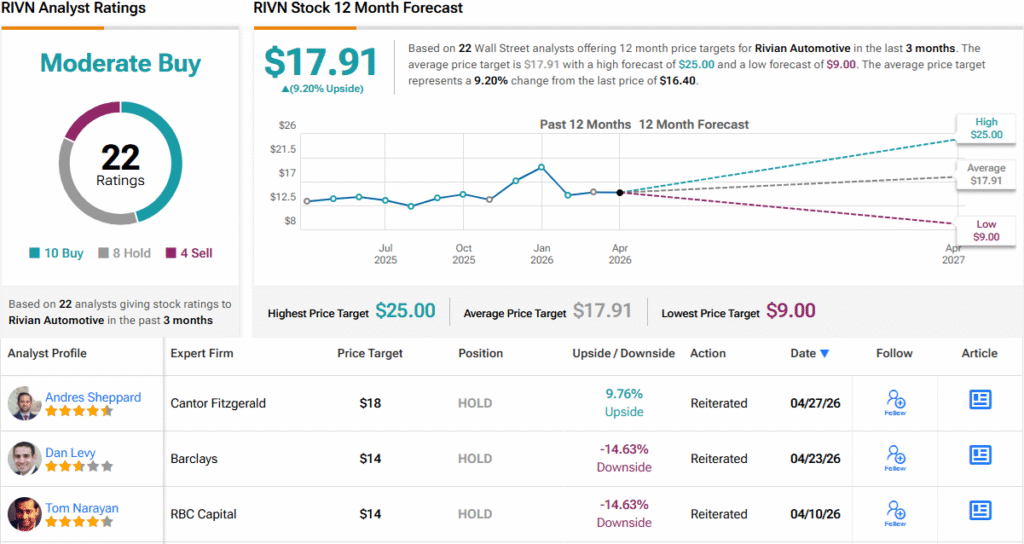

Wall Street, however, is leaning slightly more constructive. With 10 Buys, 8 Holds, and 4 Sells, RIVN stock carries a Moderate Buy consensus, while the average 12-month price target of $17.91 implies potential upside of about 11%. (See RIVN stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.