Palantir (NASDAQ:PLTR) stock is pulling back about 5% in Tuesday’s session, and the decline says more about expectations than execution. The company delivered another strong set of results, beating on revenue, earnings, and guidance, yet the reaction points to a market that had already priced in near-flawless performance. After all, shares are still up about 1,750% over the past three years, leaving little room for anything short of a clear step higher in the outlook.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

One area drawing closer scrutiny is the pace of growth in the U.S. commercial segment, which many investors view as the clearest indicator of how well Palantir is turning its AI momentum into sustained business expansion. In Q1, U.S. commercial revenue surged 133% year over year to $595 million, but came in below expectations of $604 million.

More broadly, the quarter itself leaves little to criticize. Revenue climbed 85% year over year and 16% sequentially to $1.63 billion, accelerating from 70% growth in the prior quarter and topping estimates by about $90 million. U.S. revenue surged 104% year over year and 19% quarter over quarter to $1.28 billion, driven by ongoing AIP demand, while U.S. government growth picked up to 84% from 66% in Q4. Margins stayed elevated, with adjusted operating margin at 60% and free cash flow margin at 57%, pushing the Rule of 40 score to 145% from 127% last quarter. On the bottom line, adjusted EPS came in at $0.33, beating expectations by $0.05.

The company executed on the guide too, raising the outlook for 2026 across all metrics. Management expects revenue growth of 71% year-over-year, raised from the previous 61%, with revenue now expected between $7.650 and $7.662 billion compared to the Street at $7.28 billion. U.S. Commercial growth guidance was lifted to over 120% from 115%, while the adj. operating income outlook implies a 58% margin, even as the company continues to invest heavily in AIP and technical hiring.

So what do you do with the stock now? Jefferies analyst Brent Thill thinks it may be time to say goodbye.

While Thill agrees with CEO Alex Karp that Palantir “remains at the forefront of AI conversations” and recognizes its strong growth trajectory, the analyst thinks the key issue is valuation. Even assuming roughly $12 billion in calendar year 2027 revenue, the stock is trading at about 31x EV/CY27E revenue, which to Thill appears stretched. The analyst also sees a potential risk that Palantir’s roughly 60% margin profile could indicate underinvestment, particularly in go-to-market efforts, which might constrain its ability to “fully capture the broader opportunity.”

And that results in a downbeat assessment as far as the investment case goes. “We continue to view risk/reward as unfavorable. PLTR’s fundamentals are exceptional, but the stock requires a heroic durability assumption to justify the current multiple at 31x CY27 rev,” the 5-star analyst summed up. “We believe PLTR remains vulnerable to any moderation in AI enthusiasm or even modest headline deceleration.”

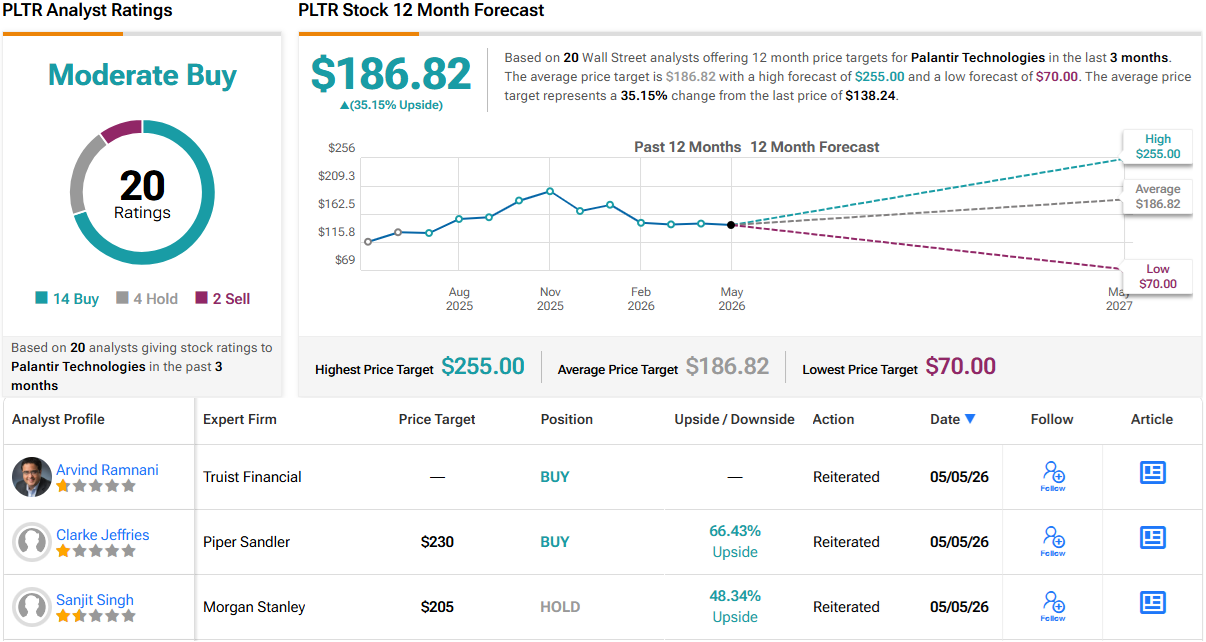

To this end, Thill assigns PLTR shares an Underperform (i.e., Sell) rating, backed by a Street-low price target of $70, a figure that points toward 12-month losses of 49%. (To watch Thill’s track record, click here)

Thill, however, is among a minority on Wall Street. While 1 other analyst joins him in the bear camp, with an additional 14 Buys and 4 Holds, the consensus view is that this stock is a Moderate Buy. Going by the $186.82 average price target, a year from now, shares will be changing hands for a 26% premium. (See PLTR stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.