Microsoft (NASDAQ:MSFT) shares are down about 4% in Thursday’s trading, extending their year-to-date decline to 16%, as investors look past better-than-expected fiscal third-quarter results and focus on what didn’t quite land. While the company delivered a solid beat and Azure growth came in stronger than anticipated, the overall reaction suggests the report still fell short of the market’s elevated expectations.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Azure revenue increased 40% vs. the year-ago period (39% in constant currency), and Microsoft guided to roughly 40% Azure growth in the fourth quarter, which is above the 37% analysts were expecting. That will represent the second straight quarter of 40% growth, as broad-based customer demand continues to outpace available supply.

But the problem, as it was in the previous quarter, appeared to be the level of spend on the buildout of AI infrastructure.

J.P. Morgan analyst Mark Murphy notes that the CY2026 CapEx guide of ~$190 billion, compared with Street expectations of roughly $150–160 billion, is a “big development,” as it signals materially higher spending earlier than investors had anticipated and may take time for the market to fully absorb.

While Murphy points out that sometimes large upside revisions to the CapEx guide “gives investors pause in the short term,” he thinks it more strongly reflects a “decidedly positive” demand backdrop, and he expects the market will increasingly recognize this over time.

Murphy also concedes that from a “high-level optics perspective,” Amazon, Google, and Oracle are currently showing faster cloud growth acceleration than Azure (in the latest quarter, GCP accelerated by roughly 16 percentage points, OCI by about 15 points, AWS by around 4 points, while Azure was up about 1 point).

That said, Murphy had previously argued that “patience will be rewarded as the recent step-up in Microsoft’s CapEx & RPO should eventually flow into the top line,” and there are early signs that this is starting to play out. Azure’s FYQ4 (June) cc growth guidance points to another uptick despite a difficult comp, coming in above expectations and helped by earlier-than-expected capacity additions.

“Our view is that investors should breathe a sigh of relief: Microsoft is guiding FQ4 Azure CC growth above street consensus ~37%, and directional commentary suggests 2H CY26 should also land above current expectations, probably by a couple-few points,” Murphy said.

Separately, Murphy had expected strong M365 Copilot adoption to support Microsoft 365 Commercial revenue, and that has been confirmed, with M365 Commercial growth accelerating from 14% cc to 15% cc, which is a “notable achievement” for a SaaS product at this scale.

“Overall,” the analyst summed up, “in our view, Microsoft is checking the boxes on two of the most important aspects: Azure growth trending in the right direction with FQ4 Azure guidance above consensus, and M365 Copilot momentum building as it creates an increasingly meaningful tailwind to the $100B M365 Commercial business.”

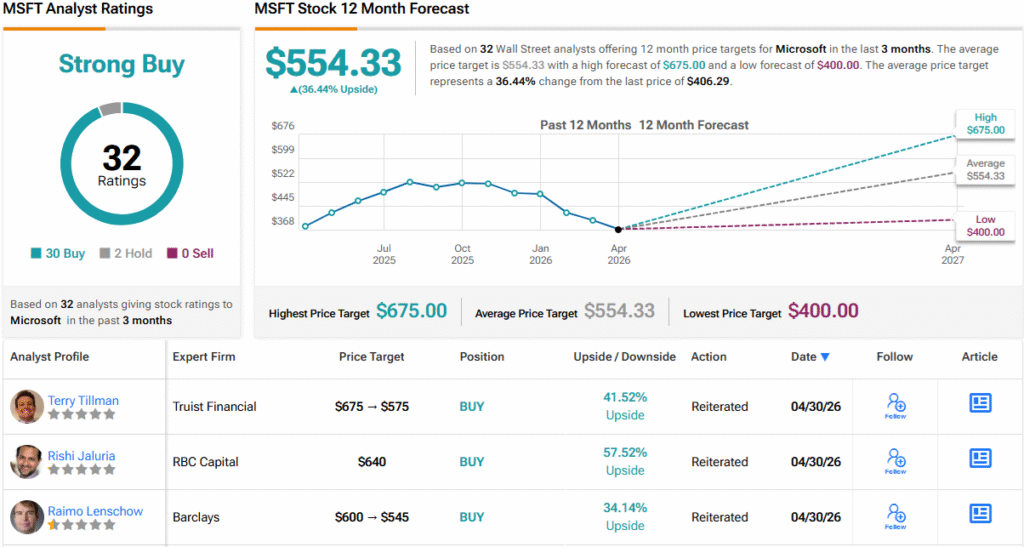

As such, Murphy assigns MSFT shares an Overweight (i.e., Buy) rating alongside a $550 price target. The implication for investors? Upside of 36% from current levels. (To watch Murphy’s track record, click here)

The Street’s average price target sits slightly higher at $554.33, implying potential one-year upside of about 36%. Overall, the stock boasts a Strong Buy consensus, based on 30 Buys versus just 2 Holds. (See MSFT stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.