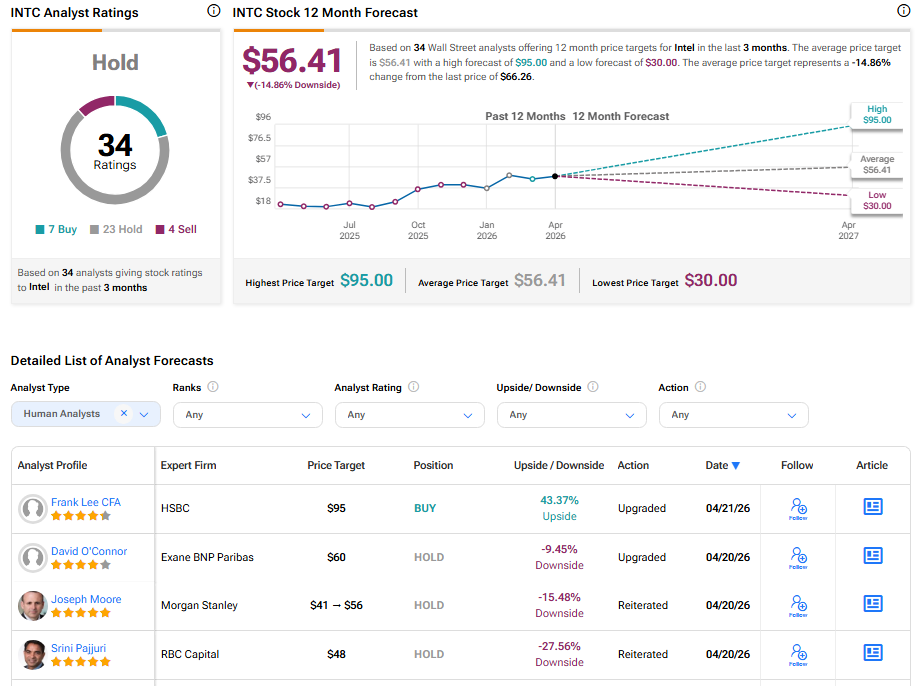

Intel (INTC) stock has been on a strong run, jumping about 40% since April 1 as a series of strategic moves boosted sentiment. Now, ahead of its April 23 Q1 earnings, HSBC sees more upside, upgrading the stock to Buy from Hold and raising its price target to a Street-high $95 (from $50), implying roughly 45% upside.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Server CPU Demand Drives the Upgrade

Top HSBC analyst Frank Lee believes the market is overlooking Intel’s biggest growth engine: the server CPU business. He expects this segment to be the primary driver for earnings growth in the coming months.

- Production Shift: Intel has moved a significant portion of its chip production away from PCs and toward its high-end Xeon server chips. This change follows a surge in demand that Intel highlighted in its previous earnings call.

- The 20% Growth Target: Lee expects server CPU shipments to grow by 20% annually in both 2026 and 2027.

- Pricing Power: Because supply is currently tight, Intel has the power to raise prices. HSBC forecasts average selling prices to rise 20% in 2026 and another 10% in 2027.

This mix of higher volume and higher prices could push margins well above current estimates. HSBC also expects strong growth in Intel’s Data Center and AI unit, with revenue forecasts above Wall Street views for both 2026 and 2027.

Overall, the bank sees meaningful upside in Intel from current levels. If server CPU growth slows to 10% in 2027, the stock could still rise about 38% from current levels, according to HSBC.

Is INTC a Good Stock to Buy?

Turning to Wall Street, analysts have a Hold consensus rating on INTC stock based on six Buys, 24 Holds, and four Sells assigned in the past three months. The average INTC price target of $54.93 per share implies a downside of 16.39%.