Arista Networks (NYSE:ANET) stock is plunging 16% on Wednesday after investors reacted negatively to the company’s updated outlook despite another quarter of strong AI-driven growth. While the networking giant delivered better-than-expected quarterly revenue and earnings, management’s raised 2026 revenue growth forecast still fell short of the lofty expectations that had built around the stock following its ~90% rally over the past year.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Management’s discussion surrounding supply bottlenecks and near-term margin pressure also raised concerns among investors already looking for near-perfect execution.

The actual quarterly results hardly looked weak, with revenue climbing 35% year over year to $2.71 billion, beating Wall Street expectations by $90 million. Adjusted earnings per share came in at $0.87, topping expectations by $0.06. Looking ahead, Arista guided for second-quarter revenue of approximately $2.8 billion, slightly above consensus expectations of $2.78 billion, alongside non-GAAP diluted earnings per share of approximately $0.88 versus forecasts of $0.86.

Morgan Stanley analyst Meta Marshall believes the latest quarter reinforced the idea that Arista’s current challenge revolves less around customer demand and far more around obtaining enough supply to satisfy that demand. The analyst pointed to wafers as “the most incremental supply constraint,” while adding that supply bottlenecks have now expanded into “a broader wafer, silicon, CPU, optics, and memory bottleneck.”

Despite the selloff, Marshall remains constructive on Arista’s longer-term positioning within AI networking. The analyst argued that the company’s advantages extend beyond hardware throughput and include “reliability, EOS, automation, and better token economics in environments where downtime or congestion is highly costly.” Marshall also believes that the latest neo-cloud customer win was important because it supports the view that Arista’s value proposition is no longer limited to raw networking performance.

According to Marshall, Arista remains “one of the cleanest ways to own the AI networking cycle,” while the quarter also reinforced that “the debate is less about demand and more about how much supply the company can secure.” The analyst further stated that AI demand is broadening “from scale-out into scale-across, and eventually scale-up,” which he sees as an encouraging sign for Arista’s longer-term opportunity set.

Marshall also acknowledged that supply constraints are likely to “weigh on gross margins near term,” particularly as shipment timing issues continue affecting the business. Still, the analyst believes Arista has “proven in the past more able to handle these challenges.”

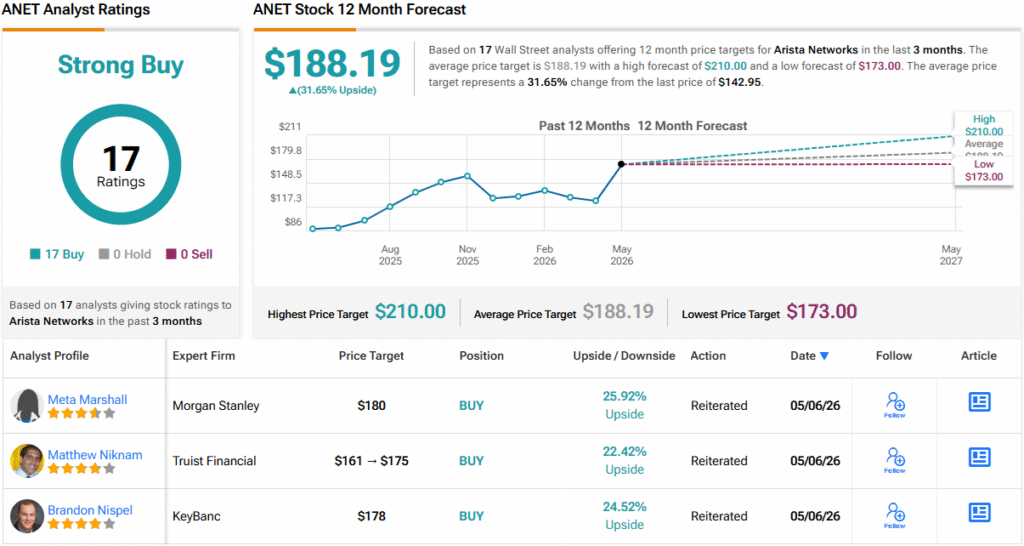

To this end, Marshall assigns an Overweight (i.e., Buy) rating on ANET, while giving the stock a $180 price target that implies about 26% upside from current levels. (See ANET stock forecast)

The rest of Wall Street also remains highly bullish on Arista shares despite Wednesday’s selloff. ANET currently boasts a Strong Buy consensus rating based on 17 Buy recommendations and zero Holds or Sells. Meanwhile, the average analyst price target stands at $188.19, implying potential upside of ~32% from current levels. (See ANET stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.