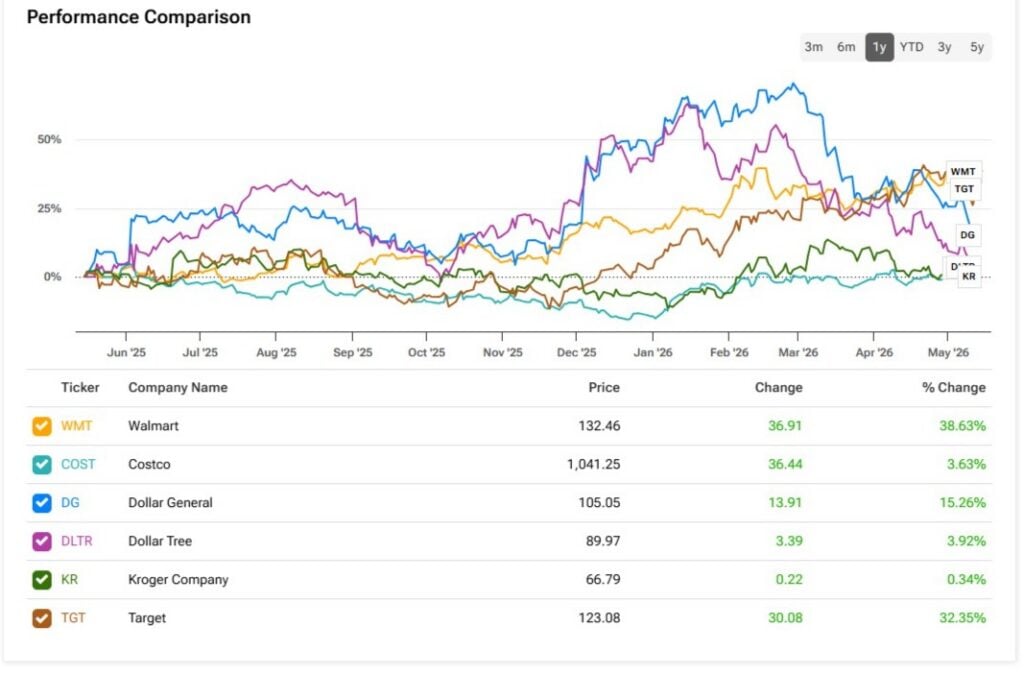

Walmart (WMT) stock looks expensive ahead of its Q1 earnings report, scheduled for May 21, but I think it appears expensive for a reason. With a trillion-dollar market cap, Walmart has become one of the clearest beneficiaries of an uneven U.S. economy. It is winning on both ends of the consumer spectrum: lower-income shoppers are trading down, while higher-income consumers are increasingly using Walmart for convenience, grocery delivery, and better pricing.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

At the same time, Walmart’s earnings profile continues to transform. From e-commerce to advertising, marketplace, and fulfillment services, the company is becoming increasingly less dependent on traditional low-margin retail. So, even though the valuation is demanding, I believe the bull case still holds as long as Q1 confirms that revenue remains resilient and operating income continues to grow faster than sales. This is why I maintain my Buy rating on WMT.

Walmart Is Winning across the Entire Consumer Spectrum

Walmart has arguably been the biggest beneficiary of an uneven U.S. retail landscape. In other words, the company has managed to capture demand in virtually every macro scenario. When budgets tighten, low- and middle-income consumers often trade down from more expensive supermarkets and retailers to Walmart. The company is typically able to undercut competitors thanks to its massive scale and strong bargaining power with suppliers.

At the same time, higher-income consumers, or those earning more than $100,000 per year, have also been migrating to Walmart. This is not only due to a product overhaul, but largely because Walmart now arguably offers the best grocery e-commerce platform in the U.S. To put this into perspective, the most relevant data point is that e-commerce already accounts for about 23% of Walmart U.S. sales, a record high.

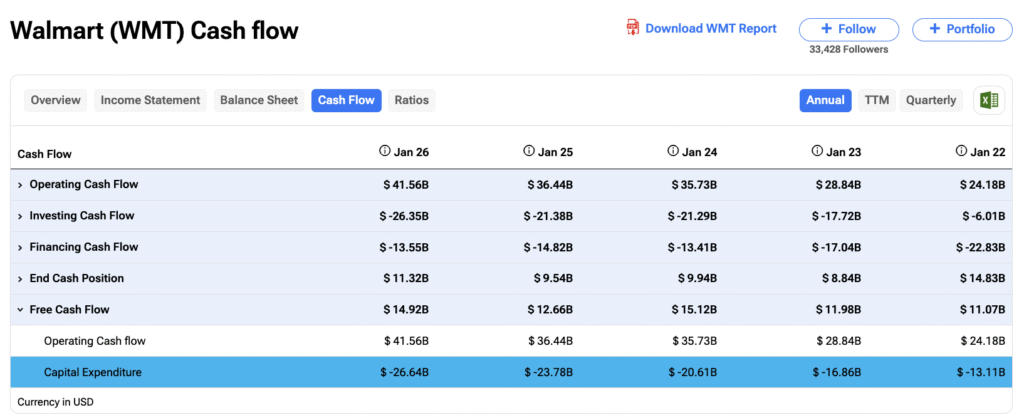

Walmart’s U.S. e-commerce business grew 27% in FY2026 and was profitable in every quarter of the year. Better yet, this is a higher-margin channel. Walmart Connect (advertising), the third-party marketplace, and Walmart+ allow the company to expand profits even while traditional retail remains under pressure. This has been the result of excellent execution and years of investment in technology and fulfillment. In fact, capex has roughly doubled over the past five years, rising to approximately 3.8% of revenue in FY26 from about 1.9% in FY21.

Walmart Heads into Q1 with a Higher Bar to Clear

As Walmart remains part of the small group of trillion-dollar companies, I would say the company heads into its Q1 earnings report with a very favorable — but also far more demanding — setup.

The company has guided for Q1 net sales to grow 3.5% to 4.5% in constant currency and for adjusted earnings per share (EPS) of $0.63 to $0.65, which implies year-over-year growth of roughly 6%. For FY27, some analysts raised an eyebrow at what appeared to be relatively soft guidance. Management is forecasting sales growth of 3.5% to 4.5% and adjusted EPS of $2.75 to $2.85.

The clearest evidence that the setup is demanding is that consensus estimates are already slightly above management’s Q1 guidance. Analysts currently expect revenue to grow 6.5% in Q1 and EPS to increase 7.8%. For FY27, consensus EPS stands at $2.92, which would imply double-digit growth in the bottom line — quite demanding. Historically, Walmart has tended to guide conservatively. That is why I believe the market is treating management’s outlook with a healthy degree of skepticism rather than taking it at face value.

Expensive for a Reason

As Walmart has transformed into a business that serves virtually all income levels, demographics, and shopping channels, the stock now trades at roughly 49x trailing earnings. That represents a premium compared to its five-year average P/E of about 35x.

In fact, the remarkable run of the past few years has allowed Walmart to close much of its historically wide valuation gap with Costco (COST). That premium has traditionally been justified by Costco’s purer membership economics and more affluent customer base. Costco currently trades at around 53x trailing earnings, only modestly above Walmart’s current multiple.

Although some investors may be spooked by the elevated multiple, I do not believe valuation alone breaks the bull case. The key point is that Walmart is no longer being valued solely as a low-margin brick-and-mortar retailer. Instead, the company is increasingly being valued as a scaled omnichannel platform. Higher-margin businesses such as advertising, marketplace, and fulfillment services are gradually reshaping Walmart’s earnings profile.

That said, I expect the bullish momentum — and Walmart’s $1 trillion market capitalization — to remain intact as long as the company continues to prove three things: revenue growth remains resilient, operating income continues to grow faster than sales, and higher-margin businesses keep becoming a larger part of the overall profit mix.

Is WMT a Buy, According to Wall Street Analysts?

The consensus rating on Wall Street for Walmart shares is a Strong Buy. Of the 30 analyst ratings issued over the past three months, 28 are Buy, and only two are Hold. Several analysts raised their price targets for WMT in March, bringing the average target price to $140.35. That implies a potential upside of approximately 5.95% from current levels.

Walmart’s Story Still Has Room to Run

I view the current environment as still favorable for Walmart ahead of its Q1 earnings. Even though the bar is clearly high, I do not believe the momentum is likely to fade as long as the company continues to provide concrete evidence that its earnings profile is structurally improving.

Perhaps most importantly, analysts have continued to raise revenue expectations, and the consensus still projects earnings growth above management’s own guidance. In other words, the market is not simply paying a premium for a defensive retailer. I believe that is probably the clearest way to frame the thesis today, and it is ultimately what underpins my Buy rating on WMT.