Roblox (NYSE:RBLX) fell off a cliff late last week, as lowered guidance proved to be a bridge too far for many an investor. The company, which reported its Q1 2026 earnings last week, severely disappointed the market by cutting its outlook for the current year.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The video game maker is now expecting revenues to increase by 20% to 25% and bookings to jump by 8% to 12% for 2026. Previously, the company had shared guidance of 23% to 29% growth for revenues and 22% to 26% growth for bookings, respectively.

The company cited “safety headwinds” (i.e. its age-check roll-out) for the changing outlook. RBLX’s share price fell by 18% in Friday’s trading session.

Still, there were some bright spots in Roblox’s earnings report. Q1 2026 revenue was $1.4 billion, up 39% year-over-year, while bookings grew to $1.7 billion, a 43% year-over-year increase. The company also reported growth in cash flow, with $629 million in operating cash flow representing an increase of 42% year-over-year.

It wasn’t enough to satisfy jittery investors.

Friday’s cascading share price is the continuation of a losing trend for RBLX, which has lost close to 70% since late September. Is this drop in value creating an opportunity for investors?

Not according to top investor Daniel Sparks, who isn’t convinced that the recent dip represents a buying window.

“The case for staying on the sidelines goes beyond one bad quarter,” states the 5-star investor, who is among the top 1% of stock pros covered by TipRanks.

Sparks appreciates the company’s growing revenues and bookings last quarter. He also notes that Roblox increased its number of daily active users to an average of 132 million, an increase of 35%, while its international daily active users outside the U.S. and Canada grew at an even greater pace of 40%.

However, he’s worried about what lies ahead, especially what would amount to “a stark deceleration” in the Q2 with bookings.

“Bookings grew 63% in the fourth quarter of 2025 and 43% in Q1,” notes Sparks. “A step down to 8% to 12% would be jarring.”

Though he acknowledges that the long-term outlook remains “compelling,” slowing growth, “a rich multiple,” and an expected consolidated net loss of more than $1 billion this year have convinced Sparks to tread cautiously.

“Until age-verification headwinds show clear signs of stabilizing and the stock is priced more attractively, I’d rather wait this one out,” he concludes. (To watch Sparks’ track record, click here)

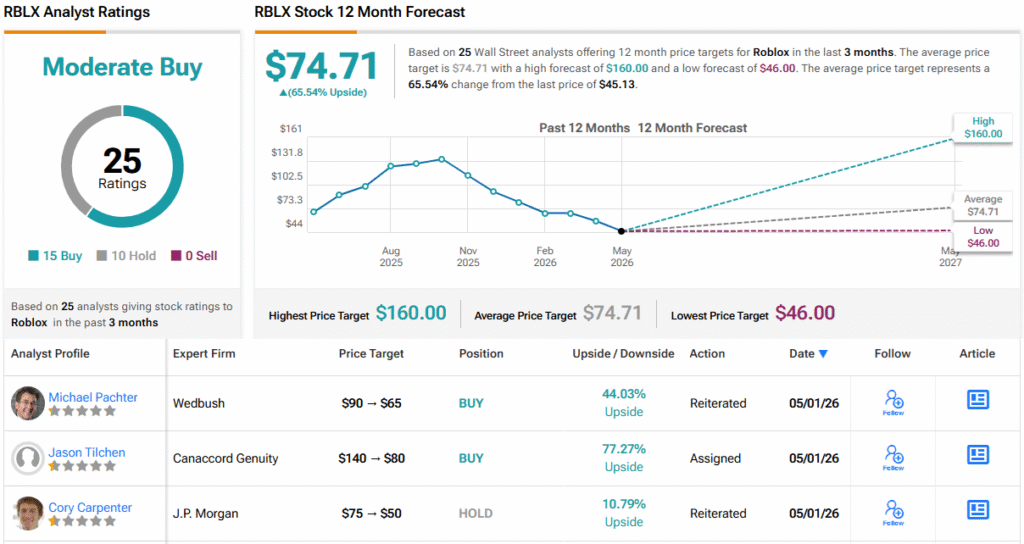

Wall Street isn’t feeling quite as cautious. With 15 Buys and 10 Holds, RBLX carries a Moderate Buy consensus rating. Its 12-month average price target of $74.71 points to an upside of ~66%. (See RBLX stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.