Vertiv (NYSE:VRT) was recently identified by Bank of America (NYSE:BAC) as the real artificial intelligence (AI) stock darling since the boom. The data center equipment manufacturer has seen its share price surge by nearly 295% over the past 12 months. Personally, I’m bullish on Vertiv and believe it can keep rising, noting its price-to-earnings-to-growth (PEG) ratio of 0.7x (1.0x or lower is generally considered to be attractive). However, I accept that all investors need to be wary of forecasts, especially when the AI revolution is unchartered territory for all of us.

Claim 30% Off TipRanks

New trading tool for NVDA bears

Vertiv: The Darling of AI

Vertiv is one of several stocks tied to the AI segment that has outperformed Nvidia (NASDAQ:NVDA) over the past 12 months. While Nvidia’s GPUs (graphics processing units) have been central to the AI revolution, Vertiv creates the essential infrastructure that supports AI technologies. The Ohio-based company provides power management, thermal management, and IT infrastructure solutions for data centers. Data Center revenue is now 75% of total sales.

Specifically, Vertiv designs and services critical infrastructure like precision cooling equipment and racks for optimal data center performance. These facilities have become vitally important, with some estimates suggesting that data centers will be so in demand that they will account for 20% of global power consumption in 2025.

According to Ohsung Kwon, an equity & quant strategist at BofA Securities, “GPUs need 2-2.5x more power than CPUs, and expected power usage for US data centers under construction is equivalent to more than 50% of the power currently used by US data centers.” With the bank forecasting power consumption from AI applications to compound at 25%-33% annually over the medium term, it’s clear that there is a huge and growing market for data center construction and servicing.

Vertiv stock jumped on Tuesday, June 18, after the company announced a partnership with Ballard Power Systems (NASDAQ:BLDP) to deliver backup power applications for data centers and critical infrastructures. Vertiv has integrated Ballard fuel cell power modules within its uninterruptible power system (UPS) and has demonstrated proof of concept. The companies said that the partnership would leverage specific capabilities to offer effective and low-carbon power solutions.

Just How Big Is Vertiv’s Market?

While estimates vary, the data center market could compound at an annual growth rate of 10.5% during 2024-2030 to reach $622.4 billion by 2030. Geographically, 40% of this market is in North America, and the market here is expected to grow at 9% annually.

There are currently 2,600 data centers in the U.S., and many of them are based in California near the respective tech hubs. However, other parts of the world will inevitably catch up in volume terms. Data centers need to be close to their end markets to minimize latency, ensuring faster data transmission and response times. Latency is fundamentally limited by the speed of light and the physical distance data must travel.

In Q1, Vertiv’s North American revenue came in at $925 million — up 7.3% year-over-year — European revenue was $381.8 million — up 10.4% year-over-year — and APAC (Asia Pacific) revenue was 332.3 million — up 6.3% year-over-year.

This geographic diversity is good to see and should allow the company to ride data center CapEx trends around the world. Some of the fastest markets outside the U.S. include the UK, India, Brazil, and Saudi Arabia. This may also be beneficial if we are witnessing hyperscalers frontloading their data center spending in the U.S.

Is Vertiv Stock Good Value?

Up 295% over 12 months and even more over 18 months, it is hardly surprising that Vertiv is looking a little expensive on near-term metrics. After all, earnings per share (EPS) haven’t grown by 308% over the past 12 months; earnings grew by 79% from Q1 of 2023 to Q1 of 2024. The stock is currently trading at 48.4x non-GAAP TTM earnings and 39.9x non-GAAP forward earnings, putting it at a considerable premium to the industrial sector.

As is commonly the case with stocks soaring on the AI boom, we need to look at growth forecasts. According to analysts, Vertiv’s EPS will grow by a phenomenal 61.1% annually over the next three to five years. In turn, this leads to a PEG ratio of 0.7x. In almost any sector, this would suggest buying conditions.

Is Vertiv Stock a Buy, According to Analysts?

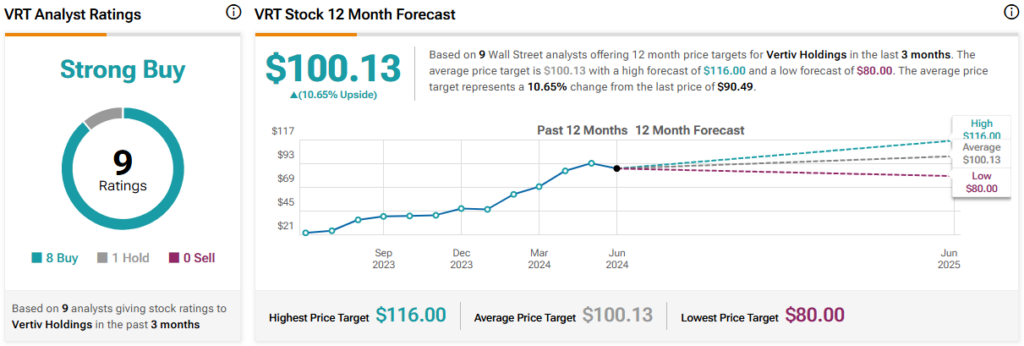

On TipRanks, VRT comes in as a Strong Buy based on eight Buys, one Hold, and no Sell ratings assigned by analysts in the past three months. The average Vertiv stock price target is $100.13, implying 5.03% upside potential.

The Bottom Line on Vertiv Stock

Vertiv stock looks expensive using near-term metrics. At 39.9x non-GAAP forward earnings, it trades at a premium to the industrials sector. However, we’ve come to expect these premiums with AI-focused stocks, and, as always, growth is key. A projected 61.1% growth rate for the medium term brings us to a PEG ratio of just 0.7x. Given the long-term trends in this sector, coupled with this very exciting PEG ratio, I can’t help but be bullish on VRT stock.