Despite missing third-quarter expectations, Vertiv (NYSE:VRT) shares are up by double digits today after the digital infrastructure solutions provider raised its full-year outlook. The company expects net sales for the full Fiscal year 2023 to be in the range of $6,826 million to $6,851 million, with EPS for the year anticipated to fall between $1.68 and $1.73.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The company’s third-quarter revenue rose by 17.6% year-over-year to $1.74 billion, although it fell short of expectations by $10 million. EPS of $0.24 also missed the cut by $0.08. Impressively, an 11% year-over-year jump in orders pushed the company’s order backlog to a record $5 billion, indicating robust market demand. Vertiv continued to benefit from favorable pricing, volume, and productivity gains.

As a pure-play data center infrastructure company, Vertiv stands to benefit from rising demand for data center infrastructure amid the current AI boom. For the upcoming quarter, Vertiv expects net sales to be in the range of $1,828 million to $1,853 million, with EPS for the period anticipated to range between $0.48 and $0.52.

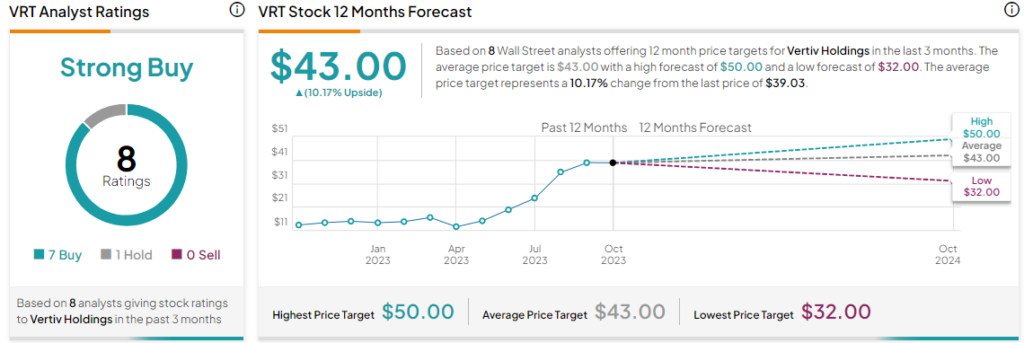

What Is the Target Price for VRT Stock?

Overall, the Street has a Strong Buy consensus rating on Vertiv. The average VRT price target of $43 implies a modest 10.2% potential upside. That’s on top of a mega 183% rally in Vertiv shares over the past year.

Read full Disclosure