Intel (NASDAQ:INTC) stock has been on a tear over the past year, surging 235% as a steady flow of developments and announcements at the chip giant fuels the rally. Yet, with shares now trading at elevated levels, valuation concerns are starting to come into focus.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Ahead of Intel’s Q1 earnings report on Thursday, Wedbush’s Matt Bryson, an analyst ranked among the top 1% on Wall Street, is urging caution. While he acknowledges the improving backdrop, Bryson believes the stock’s current valuation looks difficult to justify.

“INTC is trading at 60x our out year estimates,” the 5-star analyst said. “We don’t see industry trends supporting such an aggressive valuation with server compute units seemingly set to grow around 20% (or perhaps slightly better than that number), while PC compute likely falls off by a similar amount.”

But don’t get it wrong, despite that cautious stance on the stock, Bryson remains constructive on Intel’s near-term performance. The analyst sees the company as well positioned to outperform expectations, pointing out that the Q1 guide was “surprisingly light,” particularly on margins. With server demand improving and some pricing tailwinds in place, he believes Intel could come in ahead of both his estimates and those of the broader Street.

Looking ahead, that momentum could extend into the current quarter. With compute demand holding firm, Bryson thinks Intel is capable of at least meeting, and potentially guiding above, Q2 expectations, depending on how conservative management chooses to be.

Investors, meanwhile, have been focusing on several supportive themes, including packaging opportunities such as EMIB-T orders that could reach into the billions, renewed optimism around the foundry business with 18A builds back in focus, and signs of improving CPU demand tied to inference-driven workloads. Even so, in Bryson’s view, much of that optimism already appears reflected in the stock.

For Bryson to get more constructive, the analyst thinks there needs to be “more evidence of a recovery to value new opportunities.” As he claims to have repeatedly stated, the “single largest factor dictating Intel’s future” remains its ability to regain competitiveness in fabrication, with chip design parity now arguably a “close second.”

The shift in sentiment over the past three months appears less driven by concrete improvements in Intel’s execution and more by tightening availability of leading-edge manufacturing capacity, largely due to the continued rapid expansion of AI data centers.

Even if certain initiatives prove successful, such as EMIB packaging emerging as a credible alternative to offerings from TSMC, the analyst expects the incremental value contribution to be “far more modest than the stock’s appreciation would suggest.”

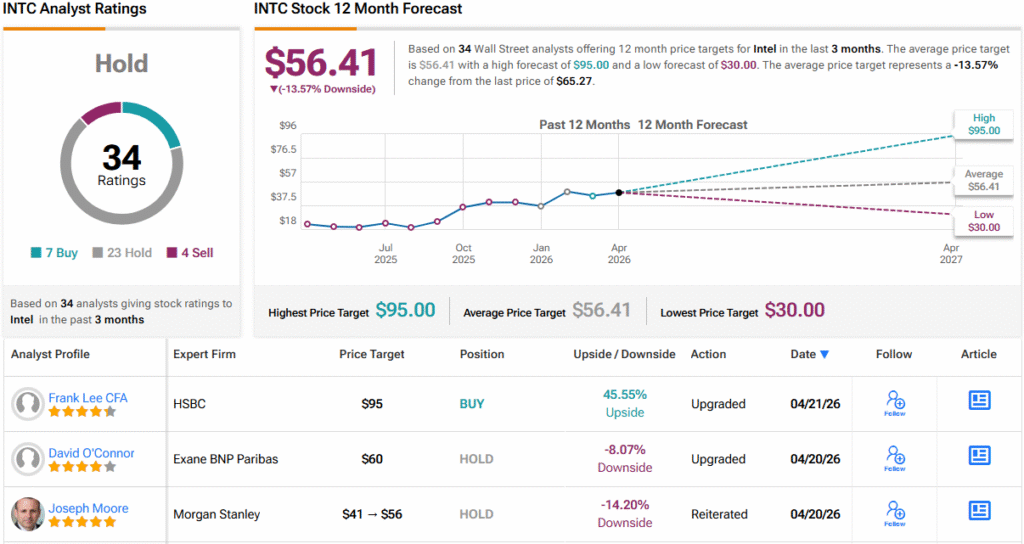

To this end, Bryson assigns a Neutral rating on Intel shares, although that might as well be a Sell, given his $30 price target suggests the shares are overvalued by 54%. (To watch Bryson’s track record, click here)

Elsewhere on the Street, the stock claims an additional 22 Holds, 7 Buys and 4 Sells, for a Hold (i.e., Neutral) consensus rating. Most other analysts also think the shares are now overvalued; at $56.41, the average price target implies the stock will post a 12-month decline of 13.5%. (See INTC stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.