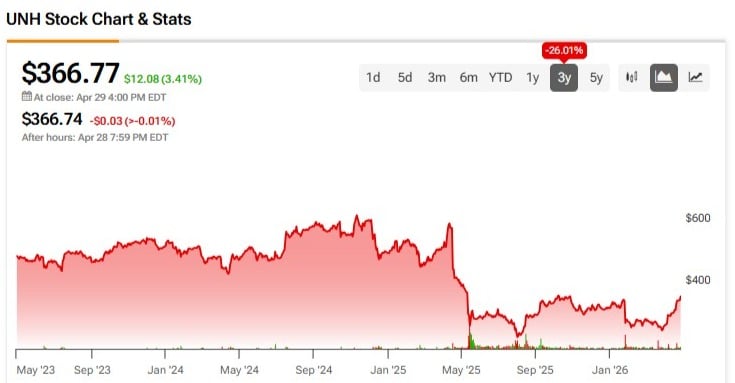

UnitedHealth Group Incorporated (UNH) looks ready for a turnaround after a long stretch of pressure, weighed down by regulatory headwinds and uneven performance, and the stock is down sharply from its 2024 highs. While the Q1 results were not perfect, it was good enough, with a raised full-year earnings outlook and signs that the core business is stabilizing, helped by regulatory developments, artificial intelligence (AI) investments, and a renewed focus on the domestic market.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

I am bullish on UnitedHealth’s prospects, as I believe the health insurance and care services company is back on track to deliver strong returns in the coming years.

Medicare Advantage Payment Increase Bodes Well for UnitedHealth

One of the biggest factors behind my bullish stance on UnitedHealth is the improving regulatory outlook. Earlier in April, the Centers for Medicare & Medicaid Services (CMS) finalized a 2.48% Medicare Advantage rate increase for 2027, significantly higher than the 0.09% payment increase proposed in January. With this, the CMS now projects additional payments of approximately $13 billion to Medicare Advantage (MA) plans in 2027, compared to just $700 million projected in January.

The surprising boost to MA payments will materially benefit UnitedHealth, as additional payments will help the company more closely align its funding plans with the recent increases in healthcare costs. One of the main reasons behind UnitedHealth’s recent margin compression is elevated healthcare costs. The newly proposed payment increase allows UnitedHealth to price its MA policies more aggressively in 2027, paving the way for a recovery in margins.

AI Investments Will Boost Operating Efficiency

My bullish stance on UnitedHealth is strengthened by the company’s aggressive AI investments, which promise to fundamentally and permanently boost the operating efficiency of the business. For 2026, UnitedHealth has allocated $1.5 billion in AI-related investments. Some of these investments are directed toward building AI-first products. Optum Real is the first product of this line. Optum Real helps automate several key functions of the managed care process, including claim evaluation and coverage validation.

According to management remarks, Optum Real has the potential to reduce manual contact costs by up to 76%, which marks a big win for the company. Alongside Optum Real, UnitedHealth is investing in automating provider workflows as well, which should reduce friction and open the door to greater long-term cost savings. Optum Rx also reported a 25% decrease in call center volume thanks to automated customer support functions introduced by the company, which highlights the long-term cost savings on the cards.

From a financial performance perspective, UnitedHealth’s AI investments will be a drag on margins in the short run. This was clear in Q1, when the operating cost ratio rose to 13.8% from 12.4% a year ago. However, these investments are likely to drive long-term margins higher, paving the way for UnitedHealth to command premium valuation multiples in the future as a fully transformed business operating at higher profitability.

The Strategic Exit from International Markets Seems Prudent

In addition to the reasons discussed above, I believe UnitedHealth’s refocus on the domestic market will also boost its financial performance in the foreseeable future. On the Q1 earnings call, the management confirmed that the company is shifting its focus back to its core U.S. healthcare markets while exiting non-U.S. businesses. As part of these efforts, UnitedHealth exited the UK market by selling Optum UK in early March 2026. UnitedHealth is already in the process of exiting its remaining businesses in South America as well.

The decision to exit non-core international markets will boost UnitedHealth’s valuation multiples in the long run. This is because international markets operated at lower margins and faced greater regulatory friction, forcing the market to value international business at low multiples. Also, the company is likely to reallocate freed-up capital to increase shareholder returns, boosting the investor sentiment toward the company. The resumption of the share repurchase program in Q2 is an early indication that reallocated capital will boost shareholder returns.

Attractive Valuation amid Tailwinds

Even on the back of a post-earnings rally, UnitedHealth is valued at a reasonable forward P/E multiple of 19x. I believe this makes the company attractively valued at a time when the regulatory outlook is finally improving. Given that the company is likely to see a margin expansion aided by its aggressive AI investments and the strategic exit from international markets, I believe a notable expansion in earnings multiple is likely over the next few years.

Is UnitedHealth a Buy, According to Wall Street Analysts?

Based on the ratings of 23 Wall Street analysts, the average UnitedHealth price target is $384.59, implying an upside of 4.86% from the current market price.

Takeaway

UnitedHealth gained momentum in the market after reporting decent Q1 earnings and boosting its full-year guidance. Behind the scenes, I believe the company is making the right strategic decisions to boost its long-term earnings power. Aided by the improving regulatory outlook and operational efficiencies stemming from AI investments, UnitedHealth seems well-positioned for a strong comeback in 2027. This makes the company attractively valued today, offering investors an opportunity to bet on the company before a full recovery.