Twilio Inc. (TWLO) is set to report its Q1 results later today, with investors watching both growth and profit trends. The stock is trading near $141 after a steady rise since the last report, as the company continues to show better cost control and stable demand.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

In the last quarter, Twilio delivered strong results. Revenue reached $1.4 billion in Q4, while full-year revenue came in at $5.1 billion. At the same time, the company posted its first full year of GAAP profit and improved its operating margin. Free cash flow also stood out, reaching $945 million for the year, up 44% from the prior year.

Growth Drivers Remain Strong, but Margins Face Pressure

Looking ahead, Twilio continues to benefit from growth in key areas. Voice revenue rose at a faster pace, while AI-related products grew over 60% year-over-year in Q4. In addition, large customer deals increased, with the number of contracts above $500,000 up 36%.

At the same time, the company is seeing more customers adopt multiple products, which helps drive higher spend per user. This trend supports steady revenue growth and better long-term value.

However, there are still some cost pressures. Twilio noted that higher carrier messaging fees are expected to impact margins. The company said these costs are mostly passed through, but they still reduce overall margin rates. For 2026, management expects these fees to lower gross margin by about 170 basis points.

There is also a near-term impact on cash flow. Twilio expects Q1 free cash flow to be about $100 million, including a planned $140 million cash bonus.

What to Expect from Q1 and Wall Street View

For Q1, Twilio guided revenue to a range of $1.335 billion to $1.345 billion, which reflects about 10% to 11% organic growth. The company also expects non-GAAP operating income between $240 million and $250 million.

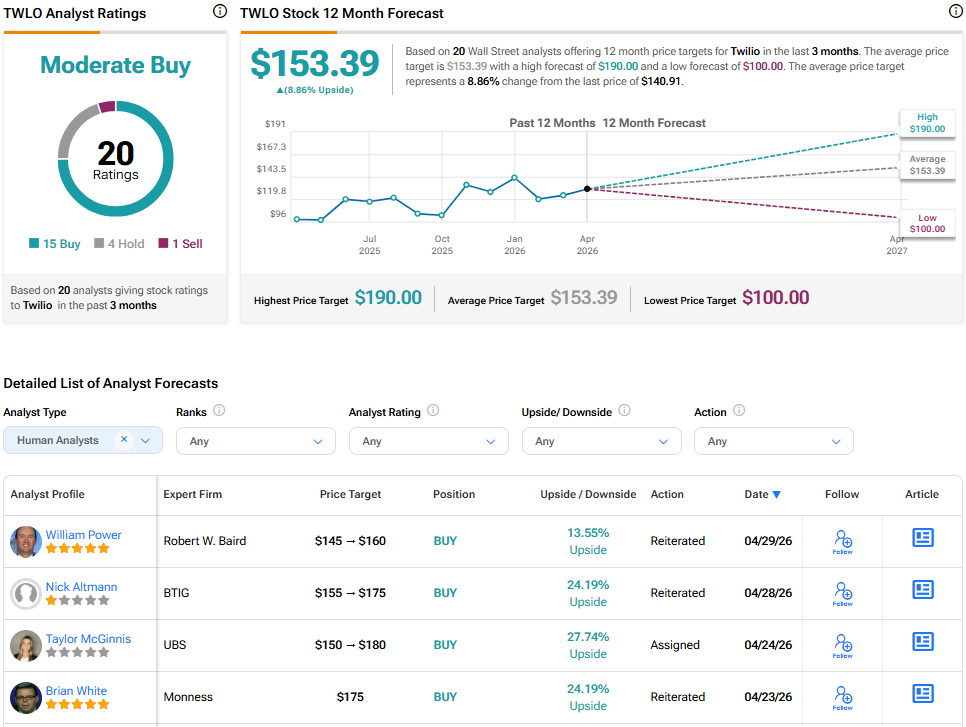

Recently, five-star analyst William Power raised its price target to $160 from $145 and kept a Buy rating. The firm said it “remains positive on improving growth,” which reflects confidence in the company’s current path.

Twilio enters this earnings report with steady growth, rising AI demand, and better cost control. At the same time, margin pressure and lower short-term cash flow remain key points to watch.

Is Twilio Stock a Buy or Sell?

Wall Street remains positive but measured. Twilio has a Moderate Buy rating based on 20 analyst reviews. The average TWLO stock price target is $153.39, which suggests about 9% upside from current levels.