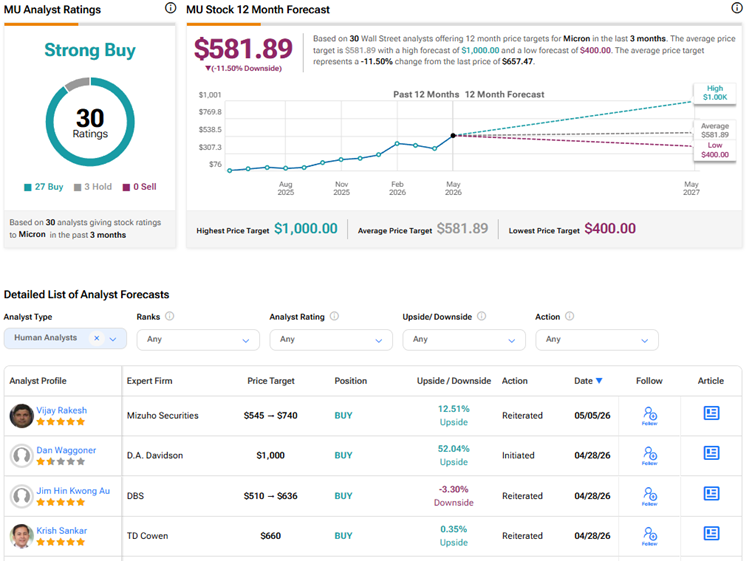

Micron (MU) stock has rallied more than 125% year-to-date and continues to rise, thanks to AI-driven demand for memory and higher pricing as demand continues to outstrip supply. In his latest research note on semiconductors, top Mizuho analyst Vijay Rakesh reiterated a Buy rating on Micron stock and raised his price target to $740 from $545, noting that agentic AI is driving memory demand higher.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Rakesh raised his estimates and price targets for Intel (INTC), Micron, ARM Holdings (ARM), DELL (DELL), SanDisk (SNDK), Seagate (STX), and Western Digital (WDC), as he continues to see robust AI inferencing-led demand for CPU (central processing unit) and memory companies.

Meanwhile, on Tuesday, Micron announced that it has started to ship its 245-terabyte Micron 6600 ION Data Center SSD (solid-state drive), which it touted as “the world’s highest capacity commercially available SSD.”

Mizuho Sees Further Upside in Micron Stock

Rakesh expects Micron to gain from solid catalysts in both DRAM and NAND, with Fiscal 2027 revenue and EPS (earnings per share) expected to grow by 66% and 80%, respectively, year-over-year. The 5-star analyst kept his estimates for the May quarter intact, but boosted revenue estimates for Fiscal 2026, 2027, and 2028 to $109 billion, $181 billion, and $179 billion, respectively, from $108 billion, $165 billion, and $164 billion. Also, he raised his EPS estimates for Fiscal 2026, 2027, and 2028 to $58.16, $104.74, and $94.40, respectively, from $57.21, $95.04, and $85.35.

Additionally, Rakesh now expects Fiscal 2026, 2027, and 2028 HBM (high-bandwidth memory) revenue to be $19.1 billion, $30.7 billion, and $35.7 billion, respectively. Notably, the analyst projects HBM revenue to grow at a 40% CAGR (compound annual growth rate) to surpass $100 billion by 2028, given that AI demand looks solid, with continued strength seen at least into 2027.

He also highlighted near-term tailwinds in traditional DRAM/NAND nodes, as AI fuels higher content in consumer end markets and drives higher pricing, consequently boosting near-term profitability.

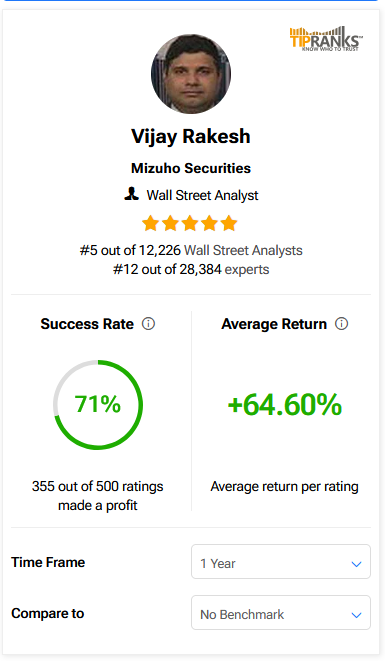

Interestingly, Rakesh ranks No. 5 out of more than 12,200 analysts ranked on TipRanks. He has a success rate of 71%, with an average return per rating of 64.6% over a one-year period.

Is MU Stock a Good Buy Right Now?

Given impressive AI-driven demand tailwinds, Wall Street has a Strong Buy consensus rating on Micron Technology stock based on 27 Buys and three Holds. Following the solid year-to-date rally, the average MU stock price target of $581.89 indicates a downside risk of 11.5% from current levels.