Picking stocks is at the heart of investing. Without a clear approach, it’s hard to build a portfolio that holds up over time. There’s no single way to do it either – some investors focus on growth, others on momentum or dividends, and each approach has its place.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

That said, some prefer to lean more on data. The market isn’t one simple system – it’s the combined activity of thousands of investors making millions of trades every day. That creates a huge amount of information, but the useful signals can easily get lost in the noise.

That’s where the TipRanks Smart Score comes in. It pulls together different data points and uses them to rate stocks based on factors that tend to matter for future performance. At the end, each stock gets a simple score from 1 to 10. A “Perfect 10” points to companies that check the right boxes across those metrics.

We used the platform to find two stocks with that top score – here’s a closer look at what’s behind them.

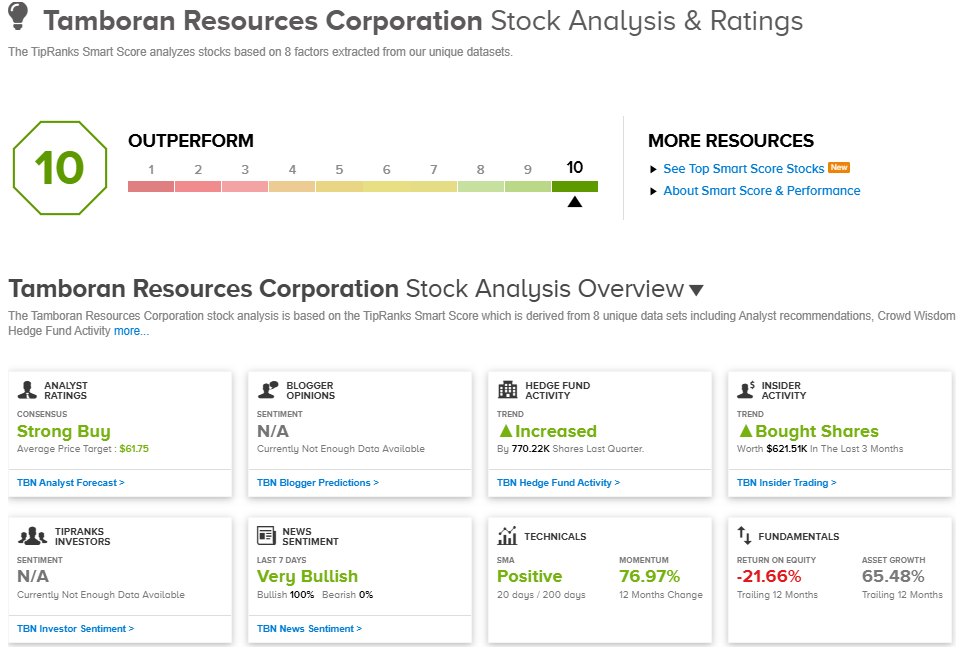

Tamboran Resources (TBN)

The first Perfect 10 we’re looking at here is Tamboran, an energy stock that is based in Australia. Tamboran was founded in 2009, and is exploring unconventional natural gas deposits of Australia’s Northern Territory, specifically in the Beetaloo Basin. The company has a leadership and technical team that is drawn from the cream of the North American gas industry – important, because the Appalachian gas deposits are world-class and have put the US on the global gas-sector map.

Tamboran’s operational plan is to put that North American expertise to work in the unconventional plays of Northern Australia. The company is looking to supply energy customers in East Asia. The acreage holdings in the Beetaloo, where Tamboran is the largest such holder, are a major asset and total some 1.9 million acres. In commercializing those assets, the company will necessarily become a major supplier to Australia’s liquefied natural gas (LNG) export industry.

An important point to note about Tamboran is that the company has not yet begun commercial gas production operations. The company is still at an advanced pre-production stage, drilling appraisal wells, including a major horizontal drilling operation. The company expects to commence commercial operations later this year.

To fund its operations, Tamboran held a stock offering in early April, putting almost 3 million shares on the market at $35, and raising approximately $103 million in gross proceeds. These figures are in US dollars.

Tamboran has caught the attention of RBC’s Scott Hanold, a 5-star analyst who notes the strength of the underlying acreage holdings as the key point.

“We believe the sizable contiguous acreage in the Beetaloo Basin position offers an increasingly rare world-class resource opportunity for investors. The early stage of initial development could provide the ability to participate in the long-term potential. This earlier stage may entail a higher risk profile compared to revenue-generating E&P counterparts but indicates a unique opportunity to get in on the ground floor before significant value becomes fully realized, in our view,” Hanold opined.

These comments support Hanold’s Outperform (i.e., Buy) rating here, while his price target, set at $55, indicates room for a one-year upside potential of 53%. (To watch Hanold’s track record, click here)

Overall, all four of the recent analyst reviews on TBN are positive, making the Strong Buy analyst consensus rating unanimous. The stock is currently selling for $35.89, and its $61.75 average price target implies a gain of 72% in the next 12 months. (See TBN stock analysis)

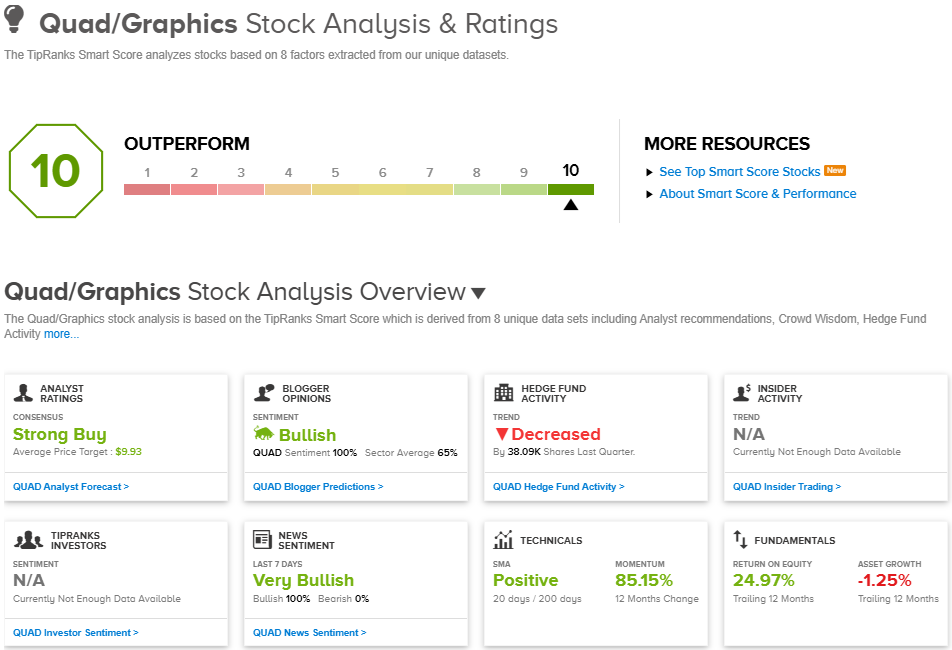

Quad/Graphics (QUAD)

Quad, the second Perfect 10 we’re looking at here, describes itself as a marketing experience company that offers its customers solutions for every aspect of the marketing world. Quad has tools and solutions suites for data intelligence, creative content work, production, media, and tech. The company can produce a wide range of marketing deliverables, from retail media to branded packaging to market research to direct mail to branded goods to print materials. More than 2,100 brands use Quad, including such names as SiriusXM, Red Bull, and Kroger.

All of these capabilities are delivered through an integrated model. Quad doesn’t work on them in a vacuum; rather, it puts them together to meet the customers’ own business objectives and needs. Quad’s capabilities are flexible, so that customers can request and receive the services they need most, whether it is a specific discipline or a multi-solution campaign. The company boasts that its marketing experience suite can match any scale.

Some numbers will show the scale of the operation. As noted, Quad has over 2,100 customers—it also has some 10,000 employees around the world, in 50 dedicated client teams, to meet those customers’ needs. Quad operates some 30 global offices and last year realized $2.4 billion in net sales. Of that total, 22% came from net sales of integrated solutions.

Quad recently released its 1Q26 financial results, and the results showed a decline in revenue and a beat in earnings. At the top line, the $581 million in revenue was down 7.7% year-over-year and missed the forecast by a modest $66,700. At the bottom line, Quad’s non-GAAP EPS of 25 cents was up 25% from 1Q25 and was 3 cents per share better than had been expected.

Benchmark analyst Mark Zgutowicz covers this marketing firm and sees plenty of runway for Quad to make gains. He writes, “The market values QUAD as a structurally impaired print company, a much too narrow frame that ignores an underlying accretive revenue mix shift and durable FCF growth. While the print industry is clearly in secular decline, QUAD’s grossly conservative valuation ignores the fact that the company continues to grow share in this fragmented industry, largely by its unique and scaled end-to-end services platform. At ~4x ‘26E EV/Adj. EBITDA, we see an attractive entry-point in a low-levered and consistent cash generating model, where modest stabilization in targeted print and marketing services and sustained FCF, will enable the stock to comfortably maintain its present EV/EBITDA multiple…”

Quantifying this stance, Zgutowicz rates the stock as a Buy. The analyst sets a $10 price target that suggests about 19% gain over the next 12 months. (To watch Zgutowicz’s track record, click here)

Overall, QUAD carries a unanimous Strong Buy consensus, with all three recent analyst reviews coming in positive. Shares are currently priced at $8.43, while the $9.93 average price target points to ~18% upside over the next 12 months. (See QUAD stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.