Palantir (NASDAQ:PLTR) remains one of the market’s best-performing stocks over the past three years. Even with this year’s pullback, the stock is still up 1,750%, powered by a run of strong quarterly results as its AI offerings gain traction.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Valuation concerns, however, have consistently hovered over the story. Oppenheimer analyst Param Singh is pushing back on that view, laying out a case for why the current premium may be more justified than it appears.

“We believe a meaningful premium is warranted for the company given its defensible moat for US government revenue (anchored by long-duration IDIQ contracts and recurring task order flow), accelerating US commercial revenue, and expanding operating margins,” Singh opined.

Singh’s bullish thesis is based on several factors. First, its Ontology serves as a “platform differentiator.” The company develops a tailored Ontology that acts as the “underlying framework” for the applications it delivers to clients. These ontologies map an organization’s people, processes, and assets to help inform operational decision-making. Once this framework is integrated, the cost and complexity of switching to another system become very high. “We view Ontology as an architectural moat, which deepens with each additional workflow that customers build on top of it,” Singh explained.

Another bullish driver is rising government spending. The US and allied militaries are increasingly shifting toward AI-driven software and autonomous capabilities. Meanwhile, Palantir has positioned itself as a preferred provider for delivering AI-based solutions. Government spending on software and services is expected to increase from $490 billion in 2025 to $666 billion by 2029, representing 8% annual growth, and this remains an “under-penetrated opportunity for the company.”

Moreover, on the commercial side, the company’s “land and expand” approach continues to gain traction. Palantir has grown its commercial customer base from 375 in 2023 to 780 in 2025, while also increasing the value delivered per client, with revenue per customer rising from $5.6 million to $8.7 million. Despite this progress, with an estimated $2.1 trillion commercial TAM (total addressable market) by 2030, Singh thinks there is a “long runway for Palantir to deliver accelerated commercial growth.”

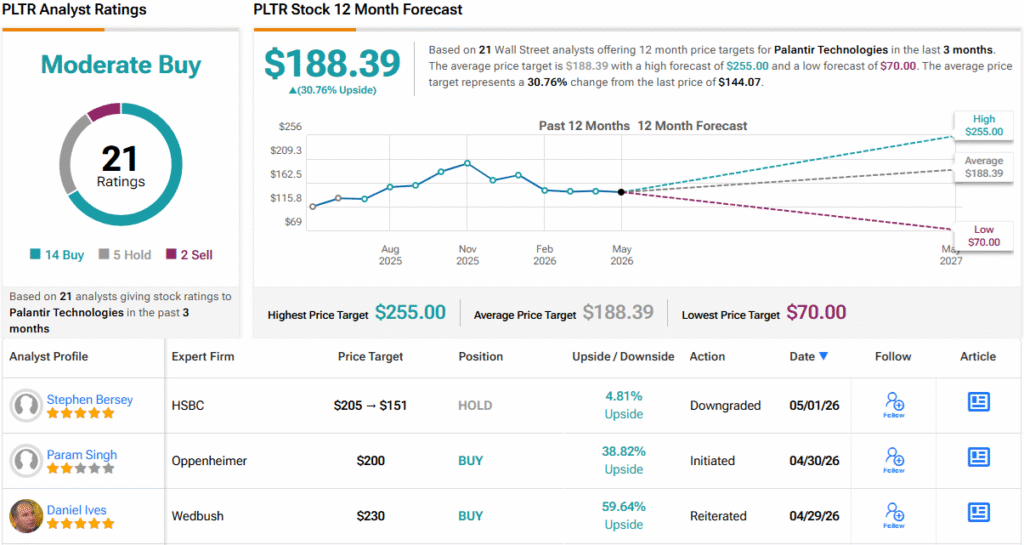

Accordingly, Singh initiated coverage of Palantir with an Outperform (i.e., Buy) rating and a $200 price target, implying the stock will gain 38% in the year ahead. (To watch Singh’s track record, click here)

So, that’s Oppenheimer’s view, but what does the rest of the Street make of PLTR’s prospects? Based on an additional 13 Buys, 5 Holds and 2 Sells, the analyst consensus rates the stock a Moderate Buy. Going by the $188.39 average price target, a year from now, shares will be changing hands for a 31% premium. (See PLTR stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.