Palantir (NYSE:PLTR) shares have been a standout in 2024’s ongoing AI-feeding frenzy, skyrocketing by 283% this year alone. Unlike many fleeting AI trends, Palantir’s meteoric rise is underpinned by a solid foundation of real-world achievements.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

In its Q3 2024 earnings report released earlier this month, the company reported a 30% year-over-year revenue growth, reaching $725.5 million and surpassing estimates by ~$22 million. Additionally, free cash flow margins experienced a dramatic increase, rising to 60% compared to 25% during the same period last year.

Bolstering the case for PLTR bulls, the breakdown of this growth reveals impressive gains across key segments: U.S. commercial revenue surged 54% year-over-year, while government revenue increased by 40%.

However, not everyone is convinced the momentum will last. One investor, known by the pseudonym Hataf Capital, has expressed skepticism about the sustainability of Palantir’s rapid growth trajectory.

“While Q3 results showed strong growth and improved profitability, the stock’s current price assumes flawless future execution, creating an unfavorable risk-reward scenario,” argues the investor.

Hataf attributes much of Palantir’s recent rally to “market euphoria.” With a forward P/E ratio of 158x and an EV/Sales multiple of 46x, Hataf contends that “the market is effectively pricing in not just continued excellence but perfect execution for years to come.”

Concerns also stem from Palantir’s investor base, where retail investors make up roughly 50%. Hataf warns that this composition could increase instability, suggesting that even minor disappointments might trigger sharp sell-offs.

“This ownership structure could amplify volatility in both directions, potentially leading to rapid multiple compression if market sentiment shifts,” the investor opined.

Adding to the apprehension, Palantir itself has acknowledged challenges in sustaining profitability long-term. Meanwhile, the company’s CEO has sold over $1.2 billion worth of stock in the past three months – a red flag that Hataf urges investors to weigh carefully.

“Now is an opportune time to at least trim positions and lock in profits,” concludes Hataf Capital, who gives PLTR a Sell rating. (To watch Hataf Capital’s track record, click here)

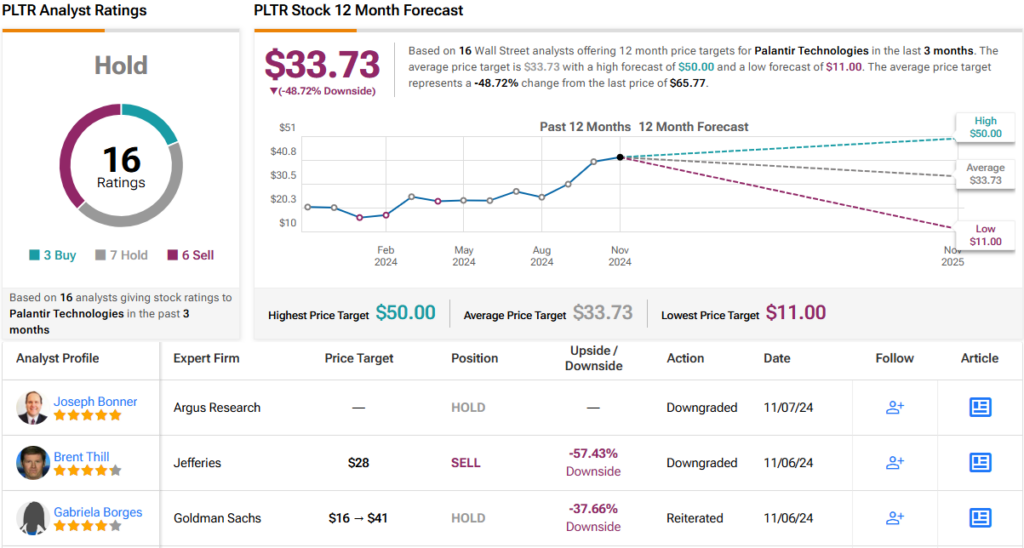

Analyst sentiment mirrors this skepticism. Palantir claims a Hold (i.e. Neutral) consensus rating, based on 3 Buy, 7 Hold, and 6 Sell recommendations. The average 12-month price target of $33.73 implies a ~49% downside from current levels. (See PLTR stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.