It’s been quite a ride for Apple (NASDAQ:AAPL) under CEO Tim Cook, who took over the reins of the iconic company in 2011. In the fifteen years he’s been running the show, Cook has elevated Apple’s valuation from around $350 billion in 2011 to roughly $4 trillion today.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Investors can therefore be forgiven for wondering whether the CEO’s planned exit on September 1st could signify that the company’s best days are in the rearview mirror. Some cracks have already been forming in the Apple story over the past few years, with worries over the company’s AI progress (or lack thereof).

And yet, despite the well-publicized shortcomings of its initial AI efforts, the company just lodged its best quarter in history. In its fiscal second quarter, Apple reported GAAP EPS of $2.01, beating expectations by $0.07, while revenue reached $111.18 billion, up 16.5% year over year and ahead of estimates by $1.6 billion.

With Apple shares now up about 3.5% in after-hours trading following the release, one top investor, known by the pseudonym Stone Fox Capital, argues this could be an opportune moment to follow Tim Cook to the exit.

“Investors should use any pop on a strong FQ2 post-earnings rally as an opportunity to cash out at a premium valuation while risks mount under a new CEO,” counsels the 5-star investor, who is among the top 4% of stock pros covered by TipRanks.

Looking at revenue drivers, Stone Fox worries that the iPhone replacement cycle appears to be coming to a close. The investor cites reported delays with the foldable iPhone, the company’s struggles with Apple Vision Pro sales, and the global memory chip shortage.

That leaves a rocky road for incoming CEO John Ternus, notes Stone Fox, pointing out that revenue estimates reflect dwindling sales growth for the next few years. Making this more concerning, AAPL still trades at a premium valuation of 31x FY2026 EPS, calculates the investor.

“Unless Apple changes this scenario, the stock is outrageously priced with a new CEO taking over,” adds Stone Fox, who rates AAPL a Strong Sell. (To watch Stone Fox’s track record, click here)

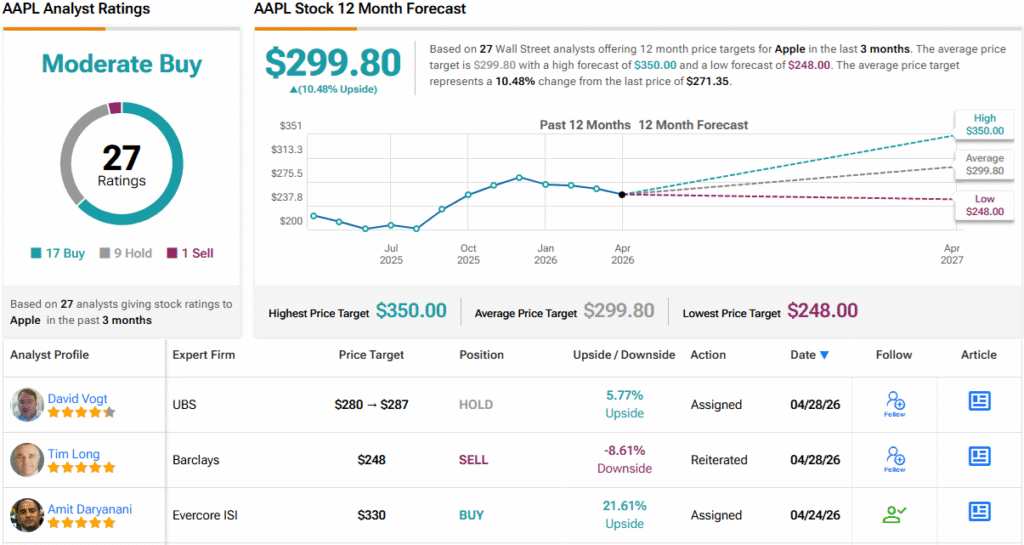

Wall Street, however, isn’t quite as ready to head toward the exits. With 17 Buys, 9 Holds, and 1 Sell, AAPL enjoys a Moderate Buy consensus rating. Its 12-month average price target of $299.80 points to 10.5% from Thursday’s closing price. (See AAPL stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.