The rapid spread of AI has been the main driver of the tech industry over the past several years. Recently, the big headlines have revolved around its impact on the software segment – as enterprise customers adopt AI tools, they may begin doing in-house what they previously purchased from software providers.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

But there are other facets to the rise of AI adoption, and they are more likely to drive upside going forward. A recent report from Venu Krishna, a strategist at Barclays, on top tech ideas and their disruptive potential this year, lays out the case and points to cybersecurity as a likely winner.

“As we think about the relative positioning within software, we think the cybersecurity space is best positioned to see increased spending prioritization as AI expands the attack surface and can lead to a greater volume and sophistication of cyber attacks, and we believe the growing use of AI tools and agents in the enterprise creates a near-term revenue opportunity for security vendors with AI security offerings,” Krishna noted.

Barclays analyst Saket Kalia has done the follow-up research, and picked out two cybersecurity stocks that stand to benefit from AI adoption. We opened up the TipRanks platform and looked up his choices; here are the details, and the analyst’s comments.

CrowdStrike (CRWD)

The first cybersecurity stock we’ll look at here is CrowdStrike. This company, well-known for its flagship Falcon platform, was formed in 2011 and has, in a relatively short time, become a $119 billion leader in the cybersecurity field. CrowdStrike’s leading platform products are described as a ‘multi-tenant, cloud-native, intelligent security solution,’ capable of securing everything from laptops, desktops, servers, virtual machines, and IoT devices against the wide range of threats that are ‘out there’ in the digital world.

CrowdStrike focuses its efforts on endpoints, where digital networks meet the outer world through the users’ hands. This view colors everything CrowdStrike does, including its work with AI.

That’s the interesting feature. CrowdStrike is building agentic AI into its platform, having noted that AI has boosted the automation and sophistication of malicious attacks – but having also noted that this is a case where one can fight fire with fire. AI makes it possible to improve security defense through simulation and automation, and CrowdStrike has made AI tech an integral part of the Falcon product for both threat detection and response.

This past March, CrowdStrike reported its fiscal 4Q26 results, delivering a solid set of numbers. Annual recurring revenue – a key gauge of future growth – increased by $331 million during the quarter, bringing total ARR to $5.25 billion, up 24% year over year. Revenue reached $1.31 billion, also up nearly 24% annually and ahead of expectations by $7.9 million. Profitability followed suit, with non-GAAP EPS of $1.12, marking a 38% jump from a year ago and coming in two cents above consensus.

For Barclays analyst Saket Kalia, the core takeaway is CrowdStrike’s strong footing in the market and its clear ability to keep pace with the rapidly evolving cybersecurity threat landscape.

“CrowdStrike has established itself as a large-scale, unified security platform, and we believe the company is on track to become durable, mission-critical infrastructure for both securing and enabling global AI adoption. As enterprises increasingly deploy AI tools, browsers, and agents, much of this activity runs directly on user devices, elevating the strategic importance of where and how security controls are enforced. In this context, the endpoint serves as a critical anchor point within a broader platform architecture, positioning CrowdStrike to naturally benefit. Zooming out, CRWD’s broader platform is likely to benefit from the expanding attack surface and growing demand for new security tools,” Kalia noted.

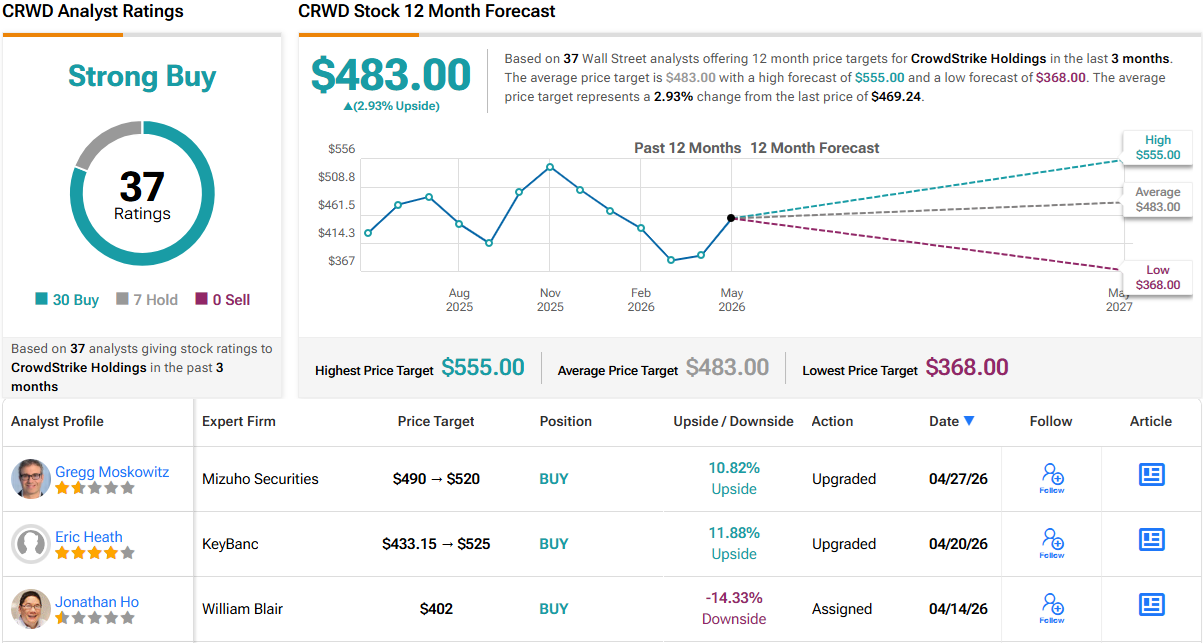

That outlook underpins Kalia’s Overweight (i.e., Buy) rating on CRWD, with his $550 price target pointing to a potential 17% upside over the next year. (To watch Kalia’s track record, click here)

The broader Street is largely in agreement. CrowdStrike carries a Strong Buy consensus based on 37 recent analyst calls, including 30 Buys against just 7 Holds. Still, expectations are more measured beyond the top-end targets – with shares currently at $455.64, the $483 average price target suggests a more modest 3% upside in the months ahead. (See CRWD stock forecast)

Varonis Systems (VRNS)

Next on our list is Miami-based Varonis Systems, a company that’s been working in cybersecurity for over two decades. Varonis offers its customers a cloud-native proprietary data security platform, optimized to protect data, a pressing need in the digital world. Varonis uses AI to power automated processes, allowing critical data protection in real time.

Varonis’s services include a wide range of vital security aspects, including database activity monitoring, data loss prevention, data classification, data access governance, data security posture management, threat detection and response, and identity protection. Automated AI processes allow the company, or the platform users, to efficiently allocate resources while proactively protecting data. This makes Varonis a customer-centered, flexible choice, capable of operating in cloud and hybrid cloud environments, on servers, and even in SaaS systems. Varonis describes its orientation as protecting data first, rather than last, and boasts that it can meet any major cybersecurity threat.

In recent months, Varonis has been moving from an on-site legacy software system to the SaaS model, and the transition has not been smooth. The company’s conversion has been slower than expected, and both analysts and investors are worried that Varonis will not meet its revenue guidance projections. The stock suffered a 49% drop last October, when the company missed badly on its quarterly results, and VRNS shares are down approximately 16% so far this year.

At the same time, Varonis’ fiscal 1Q26 results showed revenues of $173.13 million, up 27% year-over-year, and some $7.63 million better than had been anticipated. In its Q1, Varonis realized earnings of 6 cents per share in non-GAAP measures, beating the forecasters’ estimates by 11 cents per share.

In his notes on Varonis, analyst Kalia is impressed by the company’s capabilities, and paints an upbeat picture.

“Varonis is a market leader in the data security space with dedicated Microsoft 365 Copilot and ChatGPT Enterprise SKUs allowing it to directly monetize the growing demand for data security as more enterprises adopt these AI tools. Varonis also recently acquired AllTrue (now Varonis Atlas), which extends Varonis’ AI capabilities, giving it the ability to inventory and monitor an organization’s AI tools, workloads, models, agents, etc, and provide guardrails around it all. We think these factors create both a near-term revenue opportunity as Varonis sells its dedicated AI Security SKUs and a long-term opportunity as AI could expand the total addressable market (TAM) in data security, creating a broader opportunity for VRNS to go after,” Kalia opined.

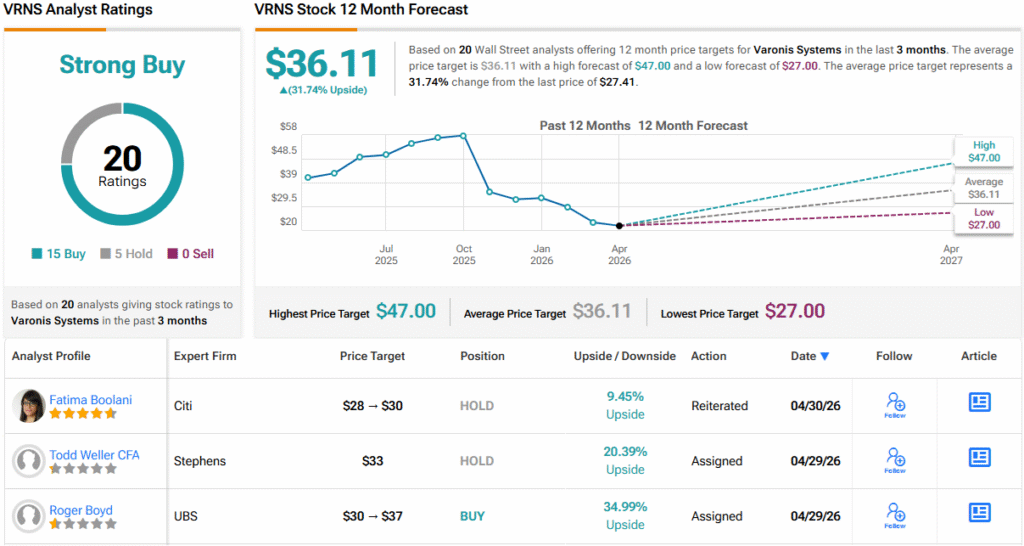

To quantify his stance, the Barclays analyst sets an Overweight (Buy) rating on VRNS, along with a $33 price target that suggests an upside of 20% by this time next year.

Despite Varonis’ recent difficulties, the market has not given up on the stock. The stock’s Strong Buy consensus rating is backed up by 20 reviews that include 15 Buys and 5 Holds. The shares are priced at $27.41, and the $36.11 average price target implies a ~32% upside potential in the next 12 months. (See VRNS stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.