Last week, stocks held near highs as gains in tech helped offset mixed macro news. The S&P 500 (SPY) rose 0.29% to 7,230, while the Nasdaq (NDX) gained 0.94% to $27,710. In contrast, the Dow Jones (DJIA) slipped 0.31% to 49,499. At the same time, the U.S. 10-year yield edged down to 4.37%, indicating that rate pressure remains but is not rising quickly.

Meet Samuel – Your Personal Investing Prophet

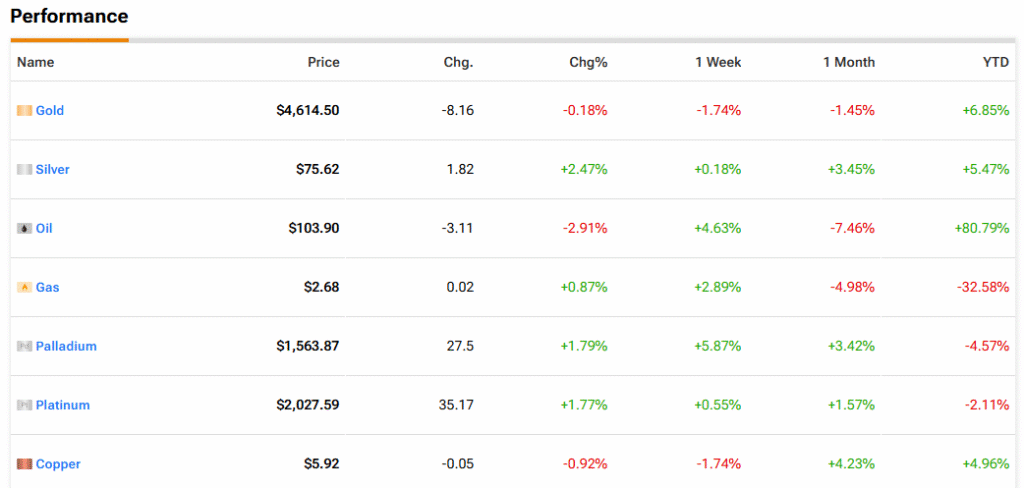

High conviction IBM bulls now have this Tradr ETFMeanwhile, oil (CM:CL) stayed volatile after a sharp jump tied to supply risk. Crude traded near $104 after a spike earlier in the week. Gold (CM:XAUUSD) held near $4,615, while Bitcoin (BTC-USD) broke $78,000, but dipped slightly afterward. Overall, the market showed a steady tone, led by tech strength, even as energy and policy risks stayed in focus.

Big Tech Earnings and AI Spend Take Center Stage

First, earnings from major tech firms shaped the week. Alphabet (GOOGL) reported cloud revenue growth of 63% to $20.02 billion, with a backlog of $460 billion. The firm also raised its 2026 capital spend plan to as much as $190 billion.

At the same time, Microsoft Corporation (MSFT) posted strong results, with Azure growth at 40% and a similar capex outlook near $190 billion. Amazon (AMZN) also beat estimates, as AWS grew 28% to $37.6 billion, showing steady cloud demand.

However, not all reactions were positive. Meta Platforms Inc. (META) raised its capex range to $125 billion to $145 billion, which weighed on shares. This reflects a broader shift, as firms keep cutting costs in some areas while raising spending on AI and data centers.

Elsewhere, Apple Inc. (AAPL) delivered solid results, reporting revenue of $111.2 billion and announcing a new $100 billion buyback. This move helped support shares and signaled strong cash flow.

In AI, deal activity also picked up. Reports said Anthropic may raise up to $50 billion at a high valuation, backed by Alphabet. At the same time, Microsoft reset its OpenAI deal to a non-exclusive model, while keeping Azure as the main cloud partner.

Macro, Energy, and Policy Drive the Bigger Picture

Beyond tech, macro news played a key role. The Federal Reserve held rates at 3.5% to 3.75%, but the decision included four dissents. This rare split shows that views on policy are starting to diverge.

In energy, oil jumped after the Strait of Hormuz stayed shut, with Brent near $126 at one point. This lifted focus on firms like Exxon Mobil Corporation (XOM), while also pushing fuel costs higher. In a related move, the United Arab Emirates said it will leave OPEC, adding more uncertainty to supply plans.

In health care, Eli Lilly and Company (LLY) raised its outlook on strong demand for its weight loss drugs. At the same time, the FDA moved to limit compounded versions of these drugs, a step that may support firms like Novo Nordisk A S (NVO) and Eli Lilly.

In the industry, General Motors Company (GM) and Ford Motor Company (F) both beat estimates and raised outlooks, helped in part by tariff refunds. In contrast, rail and airline deals faced hurdles, as Union Pacific Corporation (UNP) renewed its bid for Norfolk Southern Corporation (NSC), while merger talks between United Airlines Holdings Inc. (UAL) and American Airlines Group Inc. (AAL) fell through.

The Week Ahead

Looking ahead, Fed policy will stay in focus after the rare dissent split. Investors will watch for any shift in tone that may signal a change in the path of interest rates.

At the same time, AI spend will remain a key theme. Big Tech is set to keep raising capex, and the market will track whether this leads to steady returns or margin pressure.

In addition, oil and geopolitics will be key drivers. Any change in supply routes or OPEC policy could move prices fast and affect inflation.

Finally, earnings momentum will stay in view. Strong results from tech have supported the market, but rising costs and policy risk may shape the next move.

Upcoming Earnings and Ex-Dividend Announcements

The first week of May brings a surge of earnings across the tech, health care, energy, and consumer sectors. At the same time, a wide range of global firms will trade ex dividend, offering steady income and near-term payouts. Investors will watch demand trends, cost pressure, and margin strength, while income-focused traders will track yield and payment timing.

Earnings Preview

On Monday, May 4, Palantir Technologies (PLTR) will take center stage and is set to report $0.28 per share and a revenue of $1.54 billion. Vertex Pharmaceuticals Incorporated (VRTX) is also set to report earnings of $4.24 per share on revenue of about $2.99 billion. In addition, ON Semiconductor Corporation (ON) will report $0.61 per share on revenue near $1.49 billion, which may give a read on chip demand. Tyson Foods Inc. (TSN) is also due to post $0.78 per share on revenue of about $13.63 billion, offering insight into food demand trends.

On Tuesday, May 5, Advanced Micro Devices Inc. (AMD) will report earnings of $1.28 per share on revenue of about $9.88 billion, which may reflect AI chip demand. PayPal Holdings Inc. (PYPL) is set to post $1.27 per share on revenue near $8.05 billion. At the same time, Pfizer Inc. (PFE) will report $0.72 per share, while Super Micro Computer Inc. (SMCI) is expected to post $0.62 per share on revenue of about $12.39 billion, offering a view on AI server demand.

On Wednesday, May 6, The Walt Disney Company (DIS) will report earnings of $1.49 per share on revenue of about $24.84 billion. Uber Technologies Inc. (UBER) is expected to post $0.69 per share on revenue near $13.28 billion, which may reflect mobility and delivery demand. In the same way, Novo Nordisk AS (NVO) will report $0.88 per share, while ARM Holdings PLC (ARM) is set to post $0.58 per share, giving a read on chip licensing trends.

On Thursday, May 7, Coinbase Global Inc. (COIN) will report earnings of $0.15 per share on revenue of about $1.51 billion, which may reflect trends in crypto trading. McDonald’s Corporation (MCD) is set to post $2.75 per share on revenue near $6.47 billion, while Block Inc. (XYZ) will report $0.68 per share. In addition, Shopify peer firms like Trade Desk Inc. (TTD) will report $0.09 per share, offering a read on ad demand.

On Friday, May 8, Enbridge Inc. (ENB) will report earnings of $0.70 per share on revenue of about $8.70 billion. Nintendo Co. Ltd. (NTDOY) is set to post $0.10 per share on revenue near $2.65 billion, which may reflect game demand. At the same time, Brookfield Asset Management Ltd. (BAM) will report $0.42 per share, while AngloGold Ashanti PLC (AU) is expected to post $2.27 per share, offering a view on gold sector trends.

Ex-Dividend Dates This Week

Several large firms across sectors will trade ex-dividend during the week, with a mix of steady yields and near-term payouts.

On Monday, May 4, Citigroup Inc. (C) will trade ex-dividend with a $0.60 payout due in about 19 days. Kinder Morgan Inc. (KMI) will offer $0.30 in about 12 days, while Blackstone Inc. (BX) will pay $1.16 in about 8 days. In addition, Oneok Inc. (OKE) will offer $1.07 in about 12 days.

On Tuesday, May 5, Texas Instruments Incorporated (TXN) will trade ex-dividend with a $1.42 payout due in about 16 days. SAP SE (SAP) will offer $2.13 in about 12 days, while Baker Hughes Company (BKR) will pay $0.23 in about 12 days. In addition, Synchrony Financial (SYF) will offer $0.30 in about 12 days.

On Wednesday, May 6, EQT Corporation (EQT) will trade ex-dividend with a $0.17 payout due in about 29 days. Waste Connections Inc. (WCN) will offer $0.35 in about 18 days, while Prada S p A (PRDSF) will pay $0.19 in about 16 days. In the same way, Yangzijiang Shipbuilding Holdings Ltd. (YSHLF) will offer $0.16 in about 11 days.

On Thursday, May 7, D R Horton Inc. (DHI) will trade ex-dividend with a $0.45 payout due in about 11 days. FirstEnergy Corp. (FE) will offer $0.47 in about 29 days, while DHL Group (DHLGY) will pay $0.76 in about 19 days. In addition, MERLIN Properties SOCIMI S A (MRPRF) will offer $0.24 in about 22 days.

On Friday, May 8, Pfizer Inc. (PFE) will trade ex-dividend with a $0.43 payout due next month. Walmart Inc. (WMT) will offer $0.25 in about 23 days, while International Business Machines Corporation (IBM) will pay $1.69 next month. In addition, Energy Transfer LP (ET) will offer $0.34 in about 17 days.