Micron (MU) stock still has room to run, in my view, as artificial intelligence (AI) demand continues to reshape the memory cycle. The market still appears to treat Micron like a traditional memory cyclical, while the bigger story is that AI and high-bandwidth memory (HBM) demand could extend the cycle and support a broader re-rating. Even after massive triple-digit gains year-to-date, it seems to me that valuations are still anchored to a traditional cycle framework.

Claim 55% Off TipRanks

Explore AMZO for 2X short leverage on AMZNThe latest earnings report reinforced that shift. Supply constraints in critical memory components are driving a meaningful step-change in profitability, suggesting the semiconductor giant’s earnings profile may be structurally stronger than investors are used to seeing. For these reasons, which I will explore in more depth in this article, I continue to view MU stock as a bullish, asymmetric opportunity.

Validation Came Faster than Expected for Micron

Few moments are more favorable for a semiconductor company than a supply shortage of a critical component. In Micron’s case, that component is High Bandwidth Memory (HBM), while demand for AI is structural, concentrated, and relatively inelastic.

HBM is memory stacked in layers and placed very close to the AI accelerator, such as GPUs from Nvidia (NVDA), AMD (AMD), or custom chips. It basically exists to feed the chip with data much faster.

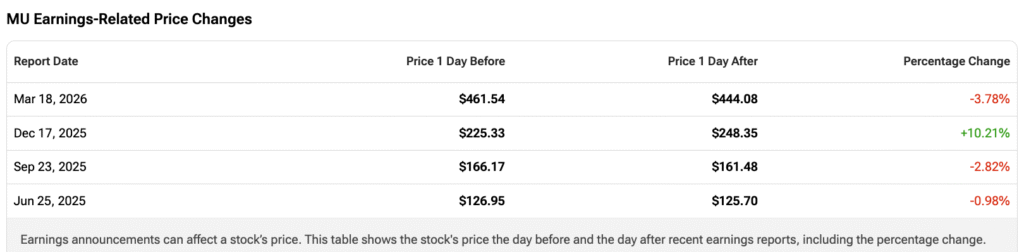

When that setup is in place, the result tends to show up in the numbers, and fast. The latest earnings report posted by Micron on March 18 was far more than a simple all-around beat. To start, revenue came in at $23.8 billion, a nearly 200% year-over-year increase and about 21% above consensus expectations.

The chart below makes it clear that dynamic random-access memory (DRAM), where HBM sits, is doing most of the heavy lifting, accounting for $18.77 billion in revenue in the last quarter. The inflection has been dramatic — moving from roughly $2–$3 billion per quarter before the AI boom in 2023 to nearly $19 billion today. That kind of step-change strongly supports the idea that this may not be a typical cycle peak.

Strong Guidance, but Rising Capex Concerns

Beyond the strong Q2 results, the real shock came from the guidance. Micron guided Q3 revenue to reach $33.5 billion plus or minus $750 million, with gross margins expected to jump to an incredible 81%. Non-GAAP EPS guidance of $19.15, plus or minus $0.40, would imply an increase of nearly 900% versus the same quarter last year.

However, there was one key point that spooked investors. To support all this demand, Micron will need to significantly ramp up its infrastructure investments. The company guided to more than $25 billion in capex for Fiscal 2026 — about $5 billion higher than prior expectations. It doesn’t stop there. Management also indicated that capex will “step up meaningfully” again in FY27, pointing to roughly $10 billion in additional construction-related spending over time.

That’s where the concern comes in. In a historically cyclical industry like memory, a multi-year investment cycle often raises the risk of future oversupply. For that reason, the immediate market reaction following Micron’s strong Q2 results was not entirely straightforward.

The Re-Rating Was Not Random

After reaching $321 per share on March 30 — about two weeks after reporting its Q2 results — Micron shares embarked on a new rally, nearly doubling the company’s market value.

I believe this explosive re-rating reflects a relief from those initial fears of a cycle peak, driven by three key factors: tech earnings season, further evidence of resilient AI capex, and the perception that Micron’s elevated capex is more “backed by demand” than indicative of irresponsible excess capacity.

Major hyperscalers like Amazon (AMZN), Microsoft (MSFT), and Alphabet (GOOGL) signaling aggressive spending on AI infrastructure — in the hundreds of billions for buildouts by 2026 — reinforced the view that demand for Micron’s memory, particularly HBM, is structural and far from peaking.

Just as importantly, Big Tech has been signaling higher spending, and memory costs are increasingly being cited as a meaningful component of AI infrastructure spending. That is highly relevant for Micron, as it turns what might otherwise look like a headwind for hyperscalers into clear evidence of pricing power for memory suppliers.

Finally, the idea that Micron’s capex may not signal future oversupply but rather a necessary response to already committed demand has helped unlock the recent re-rating of the stock. Micron itself highlighted that its advanced HBM3E and HBM4 products are sold out through 2026, with solid visibility into 2027. That alone reduces the risk that the company is simply building capacity “in the dark,” easing concerns around its elevated capex.

Valuation Still Assumes a Normal Cycle

When we look at valuations, consensus estimates still point to a fairly typical memory cycle for Micron. Micron’s earnings per share (EPS) is expected to surge from $58 in FY26 to $101 in FY27 — implying nearly 75% growth on top of an already extraordinary year. However, the consensus path then points to a sharp reversal, with EPS moderating to roughly the low‑$20s by FY28–FY29. This path helps explain why Micron looks so cheap on forward multiples today, with the forward P/E compressing to as low as about 5.7x at peak earnings.

That being said, if HBM-driven demand proves more durable, as recent quarters seem to suggest, that implied earnings “cliff” may be overstated. Assuming a more normalized EPS of around $60 — well below peak, but structurally above past cycles — and applying a conservative 12x through-cycle multiple, Micron would justify a price target of roughly $720 per share.

Is MU a Buy, According to Wall Street Analysts?

The consensus among analysts on MU shares is a Strong Buy. Of the 30 analysts covering the stock over the past three months, 27 rate it a Buy and three a Hold. However, there is also a clear sense that valuations may be getting stretched. The average price target stands at $581.89, which implies roughly 10% downside from the current share price.

When a Cyclical Story Starts to Look Structural

Given that HBM has been a clear bottleneck in AI infrastructure, and demand shows multi-year visibility, I believe Micron is no longer just a memory-cycle story. The company appears to be entering a different stage of earnings power, while the market still seems anchored to a classic boom-bust framework based on its valuation.

Recent results suggest that something more structural may be unfolding within what has historically been a cyclical thesis. As long as that holds, I continue to view Micron as an asymmetric bullish opportunity.