Alphabet (NASDAQ:GOOGL) is set to deliver its Q1 results after today’s market close, kicking off a closely watched round of updates from the top hyperscalers. Within this group, Alphabet has emerged as one of the biggest AI winners over the past year, with the stock surging a spectacular 121% over the period.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

With the print about to hit, ROTH’s Rohit Kulkarni sees room for upside across Search, Cloud, and AI-driven products, particularly if execution comes in clean. The analyst argues the setup is relatively favorable, noting the stock is less crowded than peers and often used as a hedge against Amazon and Meta Platforms. That dynamic could work in Alphabet’s favor, as a solid report – especially with Search growth above 18% and Cloud growth north of 60% – may push shares higher.

The question now is whether Amazon can deliver that kind of “clean beat.” For now, even Kulkarni’s own forecasts stop short of those thresholds, suggesting expectations, while constructive, aren’t fully priced for that level of upside.

The analyst expects Search revenue to grow around 17% to 18% year-over-year, slightly ahead of the Street estimate of roughly 16.5%. Google Cloud continues to be the “key upside driver,” with potential growth in the high-50% range compared with about 50% expected by the Street, although, as noted above, Kulkarni thinks investor expectations may have already moved higher to 60%+ growth in Q1. Operating income is likely to come in around $38 billion to $39 billion, suggesting a “meaningful beat.” YouTube, with growth hitting low double digits, could also provide a positive surprise.

For Q2, Kulkarni thinks management will signal that momentum in both Cloud and Search is likely to persist. However, he believes investor focus will increasingly turn toward whether supply can keep up, how effectively backlog is converted into revenue, and what AI-related investments mean for margins.

The analyst also expects the Capex guide, currently set at $175 billion to $185 billion, to stay unchanged in the near term, although he thinks there is a growing likelihood that it could be revised higher later in the year.

As for the main debates, Search faces limited near-term risk from AI disruption but potential longer-term pressure. On Google Cloud growth, Kulkarni thinks the company can sustain growth above 50% in the near term. As for AI monetization, the tech is currently only partially offsetting the associated costs rather than fully covering them. On whether OpenAI should be viewed as a genuine competitive threat, Kulkarni believes so, but thinks it is “manageable.” Finally, the analyst sees some concern that click trends could weaken in the second half of the year due to tougher comparisons ahead.

So, what does all this ultimately mean for investors? Ahead of the print, Kulkarni rates GOOGL shares a Buy, while his $395 price target points to one-year upside of 13%. (To watch Kulkarni’s track record, click here)

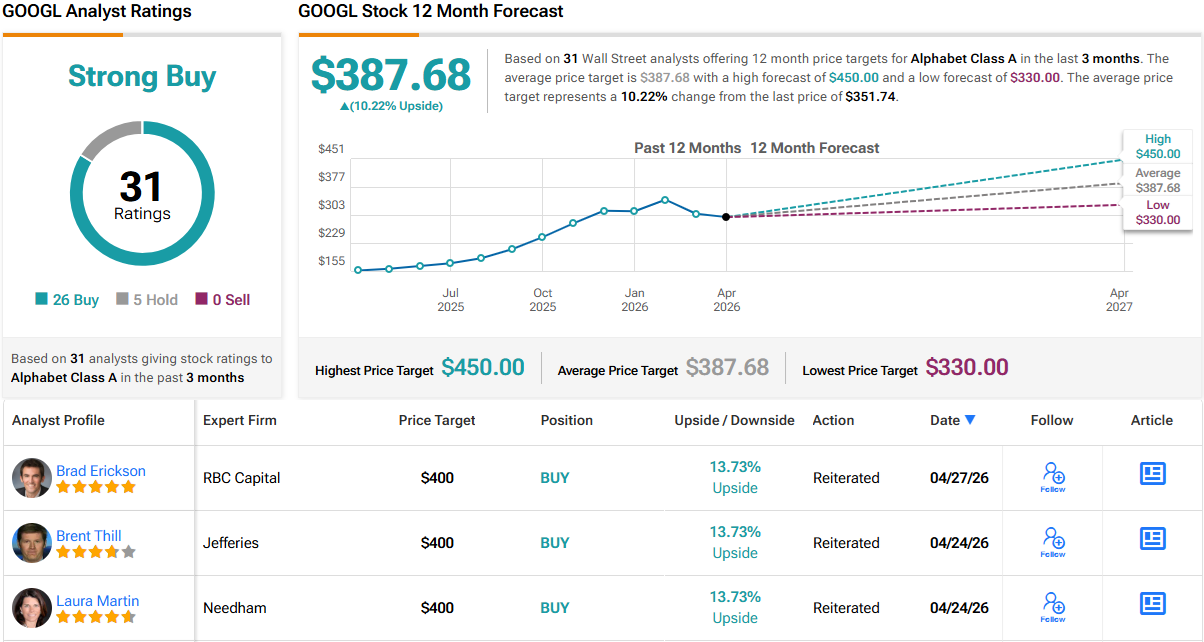

Elsewhere on the Street, GOOGL shares claim an additional 25 Buys and 5 Holds, for a Strong Buy consensus view. Going by the $387.68 average price target, a year from now, shares will be changing hands for a 10% premium. (See GOOGL stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.