Apple (NASDAQ:AAPL) has been the latest to the AI game among tech giants, but it is now hoping to make the most of the opportunity with its Apple Intelligence platform.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

According to Jefferies analyst Edison Lee, Apple’s unique advantage as the only player combining hardware and software integration allows it to leverage proprietary data, offering affordable, personalized AI services – making it an exciting prospect.

However, when it comes to fueling a significant new growth phase for the company, Lee advises investors to temper their expectations for the time being.

“Smartphone hardware needs rework before being capable of serious AI, with likely timeline of 2026/27,” Lee explained. “The high expectations for iPhone 16/17 are premature, in our view.”

While Apple has its fingers in many pies, the iPhone remains its main breadwinner by some distance and accounted for 52% of FY23 revenue. However, it also drives sales of other Apple devices and therefore also boosts service revenue growth. But Lee thinks a “lack of material new features and limited AI coverage” suggests anticipated 5%-10% growth in unit sales for the iPhone 16 is unlikely to be achieved. Lee’s analysis indicates “weaker-than-expected initial demand,” with the analyst expecting iPhone 16 sales volume in the second half of CY24 to be similar to iPhone 15 levels, with only 2.5% growth in the iPhone 16’s total lifecycle volume.

Smartphones, unlike AI servers, do not have high-speed memory or advanced packaging technologies that enable rapid data transfer between the AP and memory, which restricts their AI capabilities. While every smartphone manufacturer is working to improve this, commercialization likely won’t happen until 2026 or 2027. Therefore, expecting an “accelerated smartphone replacement cycle” based on AI advancements is “premature.” That said, Apple is expected to release a slimmer model (iPhone 17 Air) in 2025, which could drive higher upgrade demand.

Bottom line, while Lee considers AAPL the “leader in mobile AI tech,” and is excited about the long-term AI potential, the real opportunity still remains in the distance for now.

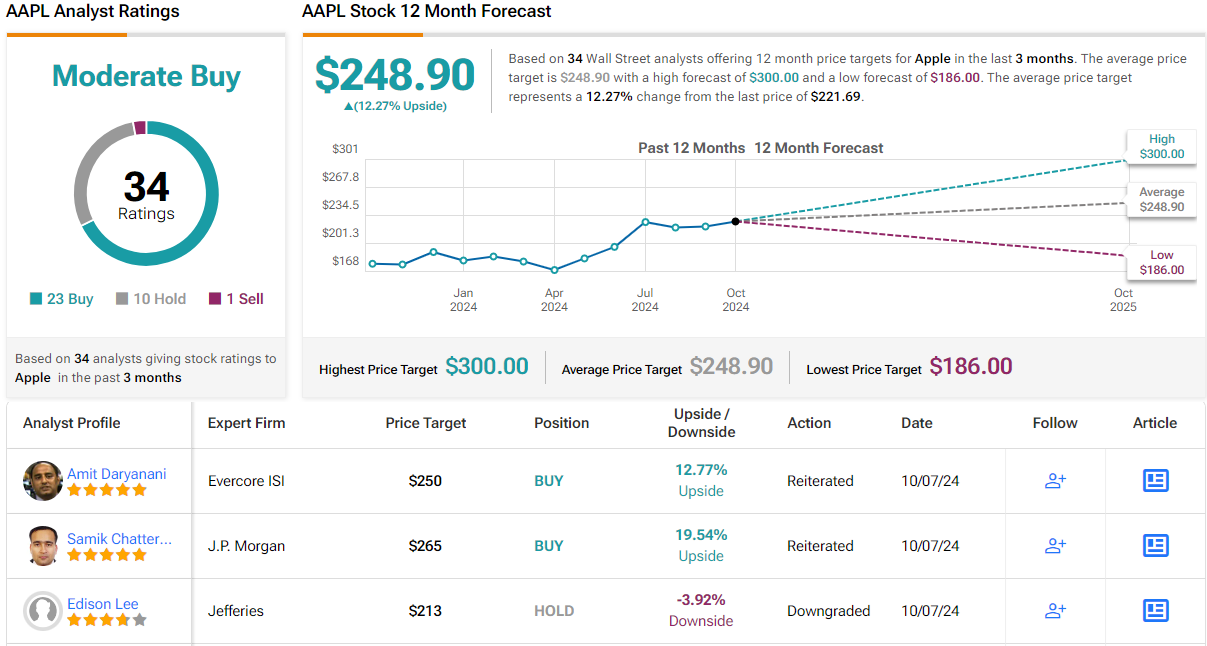

As such, Lee assumed coverage of AAPL with a downgrade from Buy to Hold (i.e., Neutral) with a $212.92 price target. The figure factors in a 12-month drop of ~4%. (To watch Lee’s track record, click here)

Meanwhile, the Street’s average price target is a more bullish $248.90, implying a potential 12% upside from current levels. Overall, the stock holds a Moderate Buy consensus rating, based on 23 Buys, 10 Holds, and 1 Sell. (See Apple stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.