Super Micro Computer (SMCI) saw its shares soar more than 18% in after-hours trading on Tuesday as the AI server and infrastructure company reported results for its third quarter of Fiscal Year 2026. While SMCI reported weaker-than-expected revenue for its fiscal third quarter, investors focused instead on a sharp recovery in profit margins and a strong outlook for the rest of the year.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Earnings Beat and Margin Recovery Drive Confidence

Supermicro’s strong earnings beat helped drive the rally, with the company reporting adjusted earnings of $0.84 per share, well above Wall Street estimates of $0.62 per share.

At the same time, the sharp recovery in profit margins also boosted investor confidence. Non-GAAP gross margins climbed to 10.1% from 6.3% in the previous quarter, easing concerns that rising competition in the AI server market was forcing the company into heavy price cuts.

The recovery also suggests Supermicro is gaining more traction in higher-value AI rack systems, which carry better profit margins and strengthen the company’s position in the fast-growing AI infrastructure market.

Revenue Miss Seen as a Short-Term Delay

Revenue for the quarter came in at $10.2 billion, missing Wall Street estimates of $12.3 billion. However, investors largely looked past the shortfall after CEO Charles Liang said the miss was mainly due to “customer site readiness.”

In other words, many customers are still preparing their data centers for the power and cooling needs required to run advanced AI systems. That suggests the issue is more about delayed deployments than weak demand.

The company’s strong growth numbers also supported that view. Revenue still surged 123% year over year, while Supermicro’s backlog reached record levels, showing demand for AI infrastructure remains strong.

Strong Guidance Adds to Investor Optimism

The rally also gained support from Supermicro’s resilient outlook. The company updated its fiscal 2026 revenue guidance to a range of $38.9 billion to $40.4 billion. While the new range was slightly below its earlier target of “at least $40 billion,” investors appeared relieved that the guidance cut was not more severe following the revenue miss.

Management’s outlook suggests the company still expects delayed AI server shipments to move through later this year. Supermicro also projected fourth-quarter sales of up to $12.5 billion, reinforcing expectations for a strong finish to the year.

At the same time, strong results from Advanced Micro Devices (AMD) added to optimism across the AI hardware sector. Investors see Supermicro as one of the key companies benefiting from the global buildout of AI infrastructure, as demand for high-performance AI servers continues to rise.

What Investors Will Watch Next

Despite the strong rally, investors are still watching a few risks closely. One major focus is Supermicro’s inventory levels, which stood at $11.1 billion. Investors will want to see how quickly the company can convert that inventory into revenue and cash flow in the coming quarters.

The company is also still dealing with a DOJ investigation tied to export controls. However, for now, Wall Street appears far more focused on Supermicro’s improving margins, strong AI demand, and bullish outlook for the rest of the year.

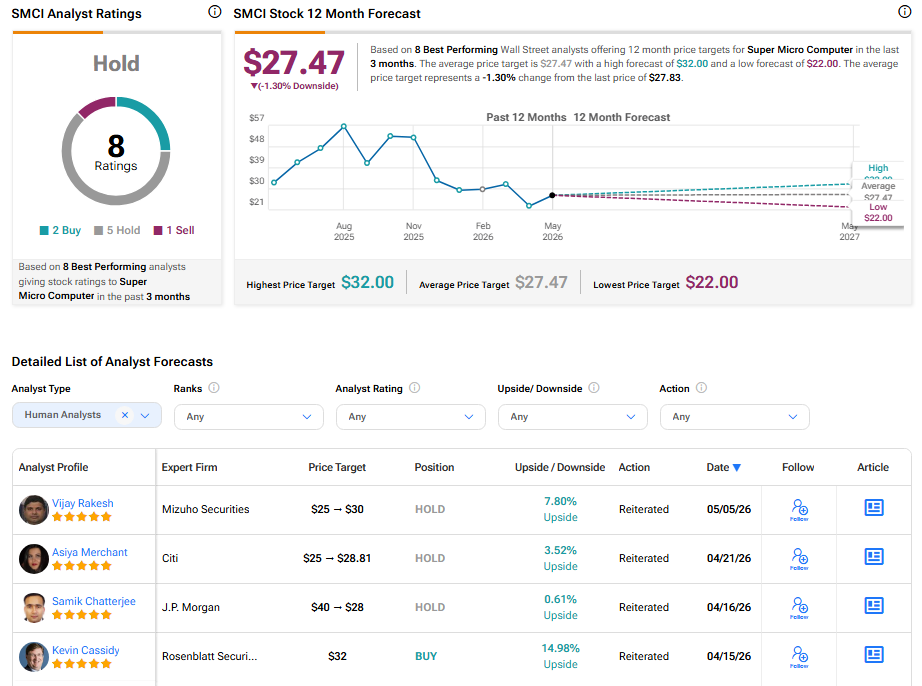

Is SMCI a Good Stock to Buy in 2026?

According to TipRanks’ consensus, SMCI stock has a Hold rating, based on three Buys, eight Holds, and two Sells assigned in the last three months. Super Micro’s share price target of $30.53 implies an upside of 12.71% over current trading levels.