Suncor Energy disclosed that it would record a non-cash after-tax impairment charge of C$425 million on its share of the White Rose asset and West White Rose project in Q420.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Cenovus Energy (CVE) is the operator of the asset and the project. CVE shares lost 2.1% in Monday’s after-hours trading before closing 2.3% higher on the day.

Cenovus Energy and Suncor Energy (SU) hold 72.5% and 27.5% in the White Rose asset, respectively. Cenovus, Suncor, and Nalco own 69%, 26%, and 5%, respectively in the West White Rose project.

The West White Rose project was planned to access 200 million barrels (gross) of crude oil and extend the life of the White Rose field by 14 years. However, the recent acquisition of Husky by Cenovus on Jan. 4, 2021 has raised questions about the future of the West White Rose Project. The operator is in discussions with government bodies to determine its future.

Suncor Energy said that the impairment charge would not affect its 2021 guidance as the White Rose field will remain on line producing as expected. The guidance did not include any major capital spending on the West White Rose project in 2021.

As part of its 2021 guidance reported on Nov. 30, the company said it expected debt repayment in 2021 to be between C$500 million and C$1 billion. It also disclosed a capital program of between C$3.8 billion and C$4.5 billion and declared a share buyback program of C$500 million.

In reaction to the guidance, Barclays analyst Christopher Tillett on Dec. 2 raised the price target on SU stock to C$31 from C$29 and reiterated a Buy rating. The new price target implies 46% upside potential.

The guidance is “incrementally positive” compared to previous forecasts, according to Tillett. (See SU stock analysis on TipRanks)

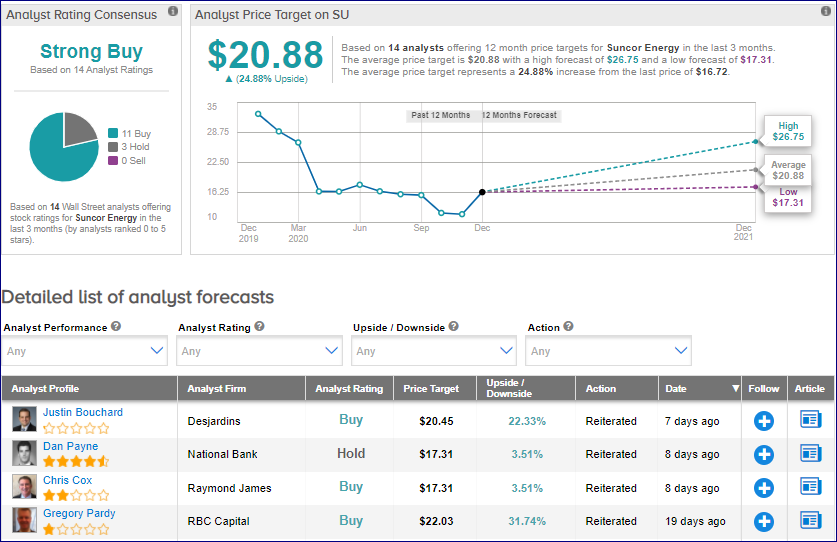

From the rest of the Street, the stock scores an analyst consensus of a Strong Buy based on 11 Buys and 3 Holds. The average analyst price target of $20.88 implies upside potential of close to 25% to current levels.

Related News:

Monday’s Market Snapshot: Here’s What You Need To Know Right Now

EasyJet Suspends Non-EU Voting Rights to Comply with Brexit – Report

Centene To Snap Up Magellan Health For $2.2B; Shares Climb