Spotify’s (SPOT) surge in free cash flow makes the recent sell-off difficult to ignore. While the music streaming platform has recently seen a slowdown in top-line growth, I do not believe this tells the full story of what is improving underneath the surface. Spotify is gradually becoming a more efficient business, with stronger margins, better monetization, and cash flow generation that would have been hard to imagine a few years ago.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

In the meantime, the ongoing sell-off has pushed SPOT’s valuation down to quite attractive levels. With free cash flow growth now enabling the company to take advantage of lower share prices through rising share buybacks, SPOT’s investment case looks particularly compelling today. Accordingly, I am bullish on the stock.

The Steady Beat of Growth

The word ‘deceleration’ tends to make investors flinch, but in Spotify’s case, it risks obscuring the more important story. Yes, Spotify has seen its top-line growth cool from the frantic above-20% days of the early 2020s. However, look more closely at the constant-currency numbers, a much fairer yardstick given the current FX volatility, and you see a robust 14% climb. At this scale, such growth is nothing but impressive, with Spotify adding 10 million Monthly Active Users, bringing the total to 761 million.

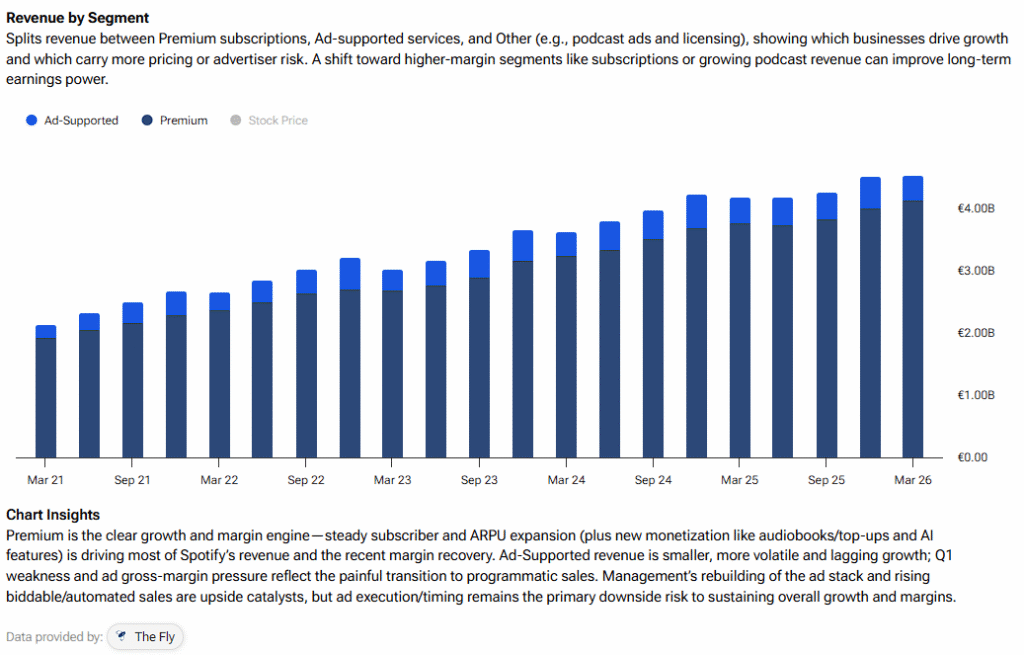

Importantly, Spotify has a high-quality user base, supported by the fact that spending a few dollars a month to stream your favorite music is an affordable luxury, one that has become a utility-like expense for many consumers. Specifically, premium subscribers hit a record 293 million, up 9% year-over-year, showing that people are happily willing to pay for the service despite multiple price hikes over the last 18 months.

Notably, during the earnings call, Daniel Ek pointed out that even with higher price tags, churn remains remarkably low. It turns out that once you’ve spent a decade building your “Discover Weekly” and your library of “Liked Songs,” Spotify actually enjoys high “switching costs.”

On the advertising side, the ad stack rebuild is finally paying off. Biddable programmatic ads, which are high-margin, now account for more than one-third of ad revenue. This shift from dull radio-style ads to sophisticated, data-driven placements is what makes the top line look so sturdy, even if ad revenue is less predictable than subscription-based cash flow.

Cracking the 30% Ceiling

Beyond solid revenue growth, Spotify’s progress toward profitability is what really supports the bull case. The bears have historically argued that Spotify will never make real money because the music labels take most of it. Well, those bears will have to find a new argument at this point, as gross margins hit a record 33% in Q1. This is a massive leap that signals the company is finally achieving the “economies of scale” it has been promising for years.

Notably, Spotify is no longer just a passive middleman for the big three labels with limited options, as it has diversified into audiobooks and video podcasts, shifting the mix toward higher-margin verticals. As it turns out, that new mix is indeed significantly more profitable. The scale they’ve reached means they finally have the leverage to dictate the terms rather than just accept them, as was the case in its very early stages, when they had to do whatever it took to penetrate the market.

More importantly, management is signaling that margins will only go higher from here as they continue optimizing their original-content spend and lean into AI-driven personalization. This should keep users engaged longer without necessarily increasing the cost of the content they are consuming. It’s a beautiful thing to see a business model reach this kind of tipping point, where every additional user starts dropping much more heavily to the bottom line.

A Free Cash Flow Powerhouse

Despite all these positive developments, Spotify stock has cratered lately. This, in turn, has made the stock particularly cheap today, especially as the revenue growth and margin expansion combo is driving superb free cash flow growth. Because Spotify operates on an asset-light, capital-light model, free cash flow is expected to continue expanding as it grows from here.

In Q1 alone, free cash flow hit a record $954 million, while the last-12-month figure is now sitting at a staggering $3.67 billion. Looking at the consensus estimates, the ramp-up is even more impressive. FCF is set to hit $4.04 billion in FY2026 and is projected to surge to $4.80 billion in FY2027.

What is the company doing with all this cash? Well, as I mentioned, they operate a capital-light model. It’s not like they are building new factories to fund future growth. So instead, they are returning cash back to shareholders. They repurchased about $1.13 billion over the past 12 months, and roughly $406 million in Q1 alone.

The trend is following free cash flow growth, meaning we will likely see repurchases accelerate, especially given the increasingly attractive share price and valuation, with SPOT trading at roughly 22x FY2026 expected FCF, and about 18x the FY2027 expected FCF, respectively. The Interactive Media sector median is at about 33x, and SPOT appears to be trading at a discount compared to the broader market.

Is SPOT a Buy, Sell, or Hold?

Despite the stock’s poor performance in recent months, Spotify still has a Strong Buy consensus rating on Wall Street, based on 20 Buy and four Hold ratings. Notably, no analyst rates the stock a Sell. In addition, SPOT’s average price target of $591.09 implies over 34% upside potential over the next 12 months.

Final Thoughts

Spotify’s extended sell-off from last summer’s highs seems to overlook what is actually going on in the business. Sure, growth has cooled compared to a few years ago, but that’s normal for a company with hundreds of millions of MAUs already on the platform. What matters is that the company is generating far more per user than before, and cash flow is now strong enough to fund large-scale buybacks. At today’s price, I still think the stock looks appealing, especially given the predictable, utility-like traits of the streaming platform, which add a wider margin of safety to Spotify’s investment case.