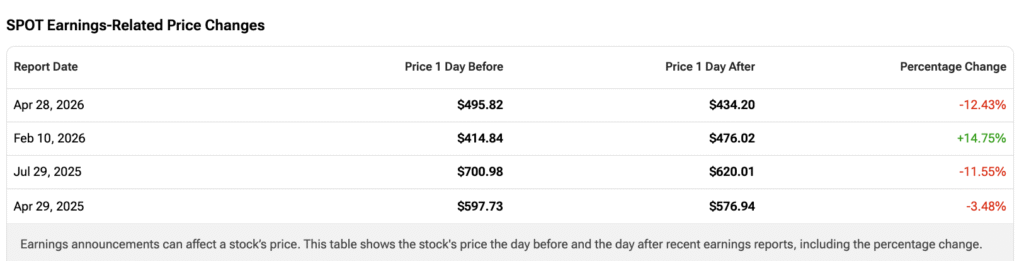

Spotify’s (SPOT) recent sell-off seems too harsh given the strength in margins and cash flow reported in Q1. The stock looks like a buy following its sharp valuation correction, with shares falling roughly 13% after the company reported its Q1 results. In my view, the sell-off was understandable, given softer Q2 operating income guidance and slower Premium subscriber growth.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

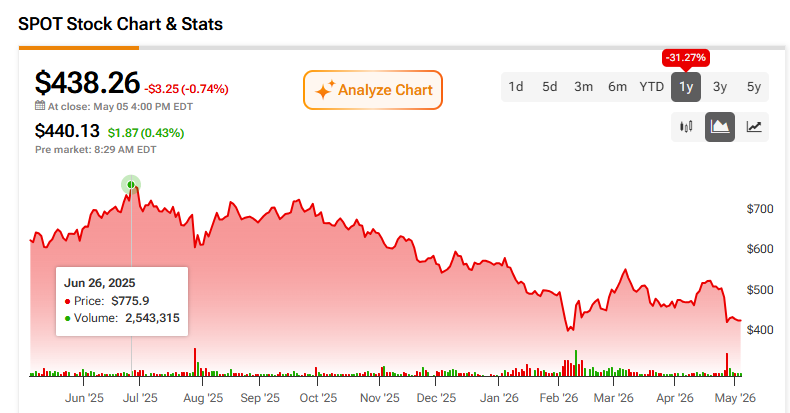

That reaction also looks even more severe given the significant correction SPOT had already seen from its all-time highs in the middle of last year. Therefore, I find it difficult to argue that this digital music, podcast, and video service is still priced for perfection the way it was roughly a year ago. The business remains fundamentally healthy, and the recent pullback appears to have created a better entry point for long-term investors, which supports my bullish stance at the moment.

The Growth Slowdown Behind Spotify’s Sell-Off

Looking back over the past 12 months, and especially the last six, Spotify shares have performed very poorly. After reaching $775 per share in June 2025, the stock now trades at around $438, implying roughly 35% upside to the market’s consensus price target.

So, what has driven such a sharp correction in Spotify shares?

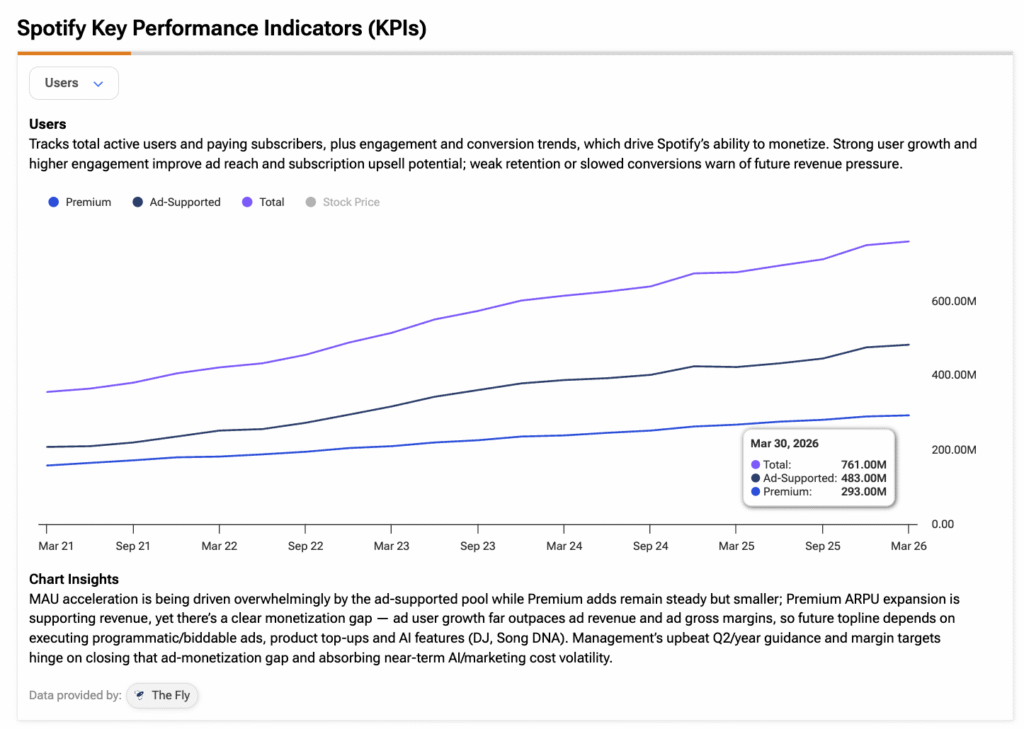

In my view, Spotify emerged from a period when the market had been pricing in a near-perfect combination of subscriber growth, pricing power, and margin expansion. Until mid-2025, that made sense. Spotify still appeared to be delivering a very strong mix of all three. In Q2 2025, for example, Premium Subscribers grew by 8 million sequentially and 12.2% year-over-year, which helped sustain the bullish narrative and justify a much richer valuation.

To give some perspective, in July 2025, some data showed that Spotify shares were trading at quite demanding multiples of 9.2x sales and 87x forward earnings.

The problem was not that Spotify stopped growing. It was simply that growth normalized too quickly for what the market had been pricing in. Premium subscriber growth slowed from a low-double-digit pace in mid-2025 to high single digits in Q1 2026, while sequential net adds fell to just 3 million. For a stock that had already rallied sharply into July 2025, that was more than enough to trigger a valuation reset.

Spotify’s Valuation No Longer Looks Priced for Perfection

However, looking more closely at Q1 results, recent momentum, and the current post-sell-off multiples, Spotify shares may now be at levels that look too harsh.

To begin with, Spotify’s valuation has been completely repriced since its all-time highs. SPOT now trades at about 4.6x sales and roughly 29.7x forward earnings, clearly showing that the market has stopped paying an extreme premium for the business. The multiples are still not exactly “cheap,” but Spotify no longer looks priced for perfection.

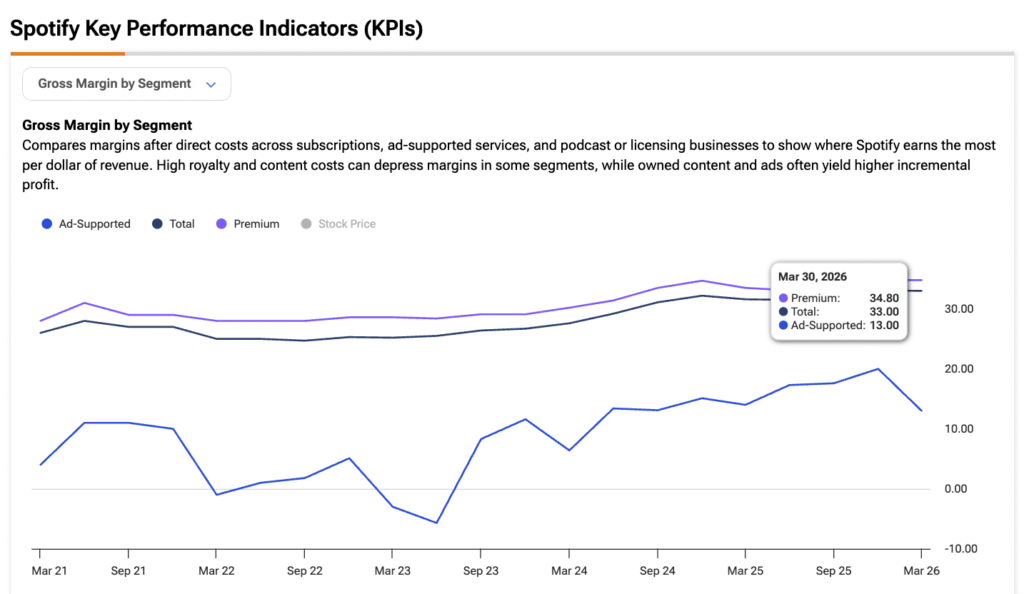

Furthermore, arguably the strongest part of the post-sell-off bull case is that even with user growth slowing, the profitability story has continued to improve significantly. Spotify posted a 13% increase in gross profit, reaching €1.50 billion, or about $1.74 billion, while expanding gross margin to 33%. The company also lifted operating income by 40% year-over-year, reaching a 15.8% operating margin, up 370 basis points year-over-year. On top of that, Spotify generated €824 million or about $954 million in free cash flow, up 54% year-over-year.

Above all, this shows that the Spotify thesis is shifting from just user growth to scaling durable earnings and cash flow.

The Q2 Guide Wasn’t Terrible, but It Wasn’t Clean Either

To avoid sounding like a perpetual bull, the key issue in the Spotify thesis is clearly forward-looking. Q2 guidance was weak in some areas, although I do not think it would be fair to call it a “terrible” outlook.

First, on the positive side, Premium subscriber net adds are expected to improve from over 3 million in Q1 to over 6 million in Q2. Monthly Active Users (MAUs) are also expected to grow by 17 million. Spotify also guided for €4.8 billion in revenue or about $5.55 billion, and a gross margin of 33.1%, slightly above the 33% reported in Q1. In other words, there are no real signs of a demand collapse.

The more questionable part is exactly where the company needed to offset the slowdown in Premium subscribers: operating income. Spotify reported €715 million or $836.83 million in operating income in Q1, but guided for €630 million, or about $737.34 million in Q2. This means that even with a higher top line, operating profit is expected to decline sequentially. According to management, this is mainly due to higher investment in marketing, cloud, and AI.

In my view, the Q2 guide has two sides. There was no collapse in demand, but operating leverage became less clean. That is not necessarily serious enough to break the bullish thesis, but it is serious enough to warrant some correction in a stock still priced at a meaningful premium.

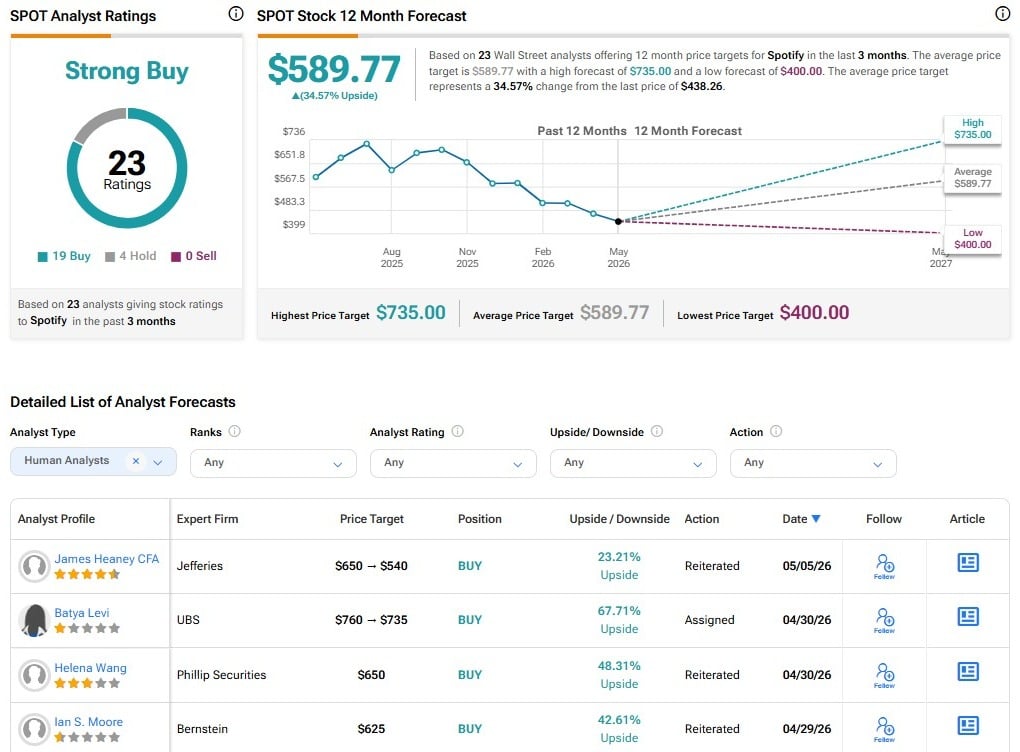

Is SPOT a Buy, According to Wall Street Analysts?

The consensus among Wall Street analysts for Spotify shares is a Strong Buy. This is based on 23 ratings issued over the past three months, including 19 Buys and four Holds. The average price target is $589.77, implying potential upside of 34.57% from the current share price.

The Bull Case Still Holds after Q1

I wouldn’t say investors’ knee-jerk reaction to Spotify stock after Q1 was “irrational.” However, a double-digit drop seems a bit harsh because the guidance did not point to any structural deterioration in users, revenue, or gross margin. To me, it looks more like a reaction to a stock that was still being judged by a standard of perfect execution.

Still, after this sharp reset, I see Spotify more as a buying opportunity than a stock to avoid. The valuation is no longer as stretched as it was in mid-2025. At the same time, the business continues to show healthy demand, expanding margins, and strong free cash flow. Q2 guidance does suggest that operating leverage may be less linear in the short term, but I do not think that is enough to undermine the broader bull case. For that reason, I am bullish on SPOT following the sell-off.