SoundHound AI (SOUN) has delivered strong revenue growth as demand for AI voice technology continues to rise across industries like automotive, restaurants, and customer service.Still, despite the company’s rapid expansion, the stock has struggled to build momentum, with SOUN shares falling more than 26% over the past six months. Looking ahead, sentiment around SOUN remains divided.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

Some investors view the recent sell-off as a buying opportunity, pointing to the company’s strong revenue growth and debt-free balance sheet. Others remain cautious due to concerns around profitability, valuation, and increasing competition in the crowded AI space. For investors with a higher risk tolerance, the sharp decline may offer a chance to buy a fast-growing AI stock at a lower valuation.

For context, SoundHound AI focuses on voice recognition and natural language processing, providing AI-powered solutions for multiple industries.

SoundHound AI Growth Is Slowing

Last week, SoundHound reported Q1 revenue of $44.2 million, up 52% year-over-year and ahead of Wall Street expectations. However, despite the solid results, investors remain concerned that SoundHound’s growth is beginning to slow. While 52% revenue growth is still strong, it marks a sharp slowdown compared to Q1 2025, when the company’s revenue surged 151% year-over-year.

Typically, high-growth companies see quarterly revenue growth accelerate faster than their full-year outlook, but that trend has not played out for SOUN in recent quarters, which may help explain why the stock has struggled to build momentum.

Profitability Concerns

While SOUN continues to show strong revenue growth, profitability remains a key concern for investors. The company is still posting losses as it spends heavily on expansion, acquisitions, and AI development. In Q1 2026, it reported a loss of $0.06 per share, better than Wall Street estimates of a $0.10 loss.

Even though the latest loss was better than expected, SoundHound has yet to prove it can consistently deliver positive earnings or free cash flow. As a result, many investors remain cautious, especially as competition in the AI sector heats up and markets shift focus from growth to profitability.

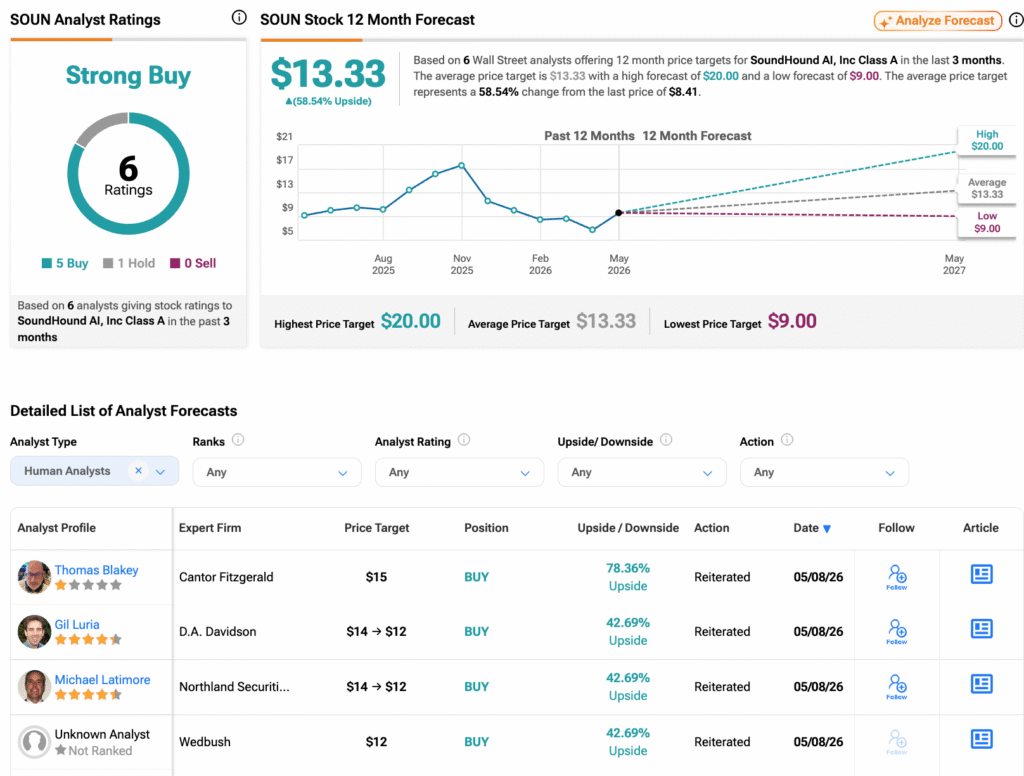

Analysts Cut SOUN Price Targets

Following the results, analysts largely maintained their Buy ratings on SOUN, but the lower price targets suggest that near-term upside expectations may be cooling.

Four-star-rated DA Davidson analyst Gil Luria reduced his price target on SoundHound from $14 to $12. He noted that the company began 2026 with revenue above expectations, supported by broad-based demand across multiple industries. However, he also highlighted earnings pressure and execution risks that could limit short-term upside despite strong long-term growth potential.

Similarly, Northland’s top-rated analyst, Michael Latimore, also cut his price target from $14 to $12, implying more than 35% upside from current levels. He pointed to slightly better-than-expected Q1 revenue driven by solid adoption of SoundHound’s AI platform, but noted that weaker profitability — due to ongoing growth and technology investments — led to lower adjusted EBITDA forecasts.

Is SOUN a Good Stock to Buy?

According to TipRanks, SOUN stock has received a Strong Buy consensus rating, with five Buys and one Hold assigned in the last three months. The average SoundHound stock price target is $13.3, suggesting a potential upside of 58.54% from the current level.