ServiceNow’s (NOW) post-earnings sell-off looks overdone after what was, in fact, a solid quarter. Last week’s print showed the business process automation leader still delivering strong growth, solid margins, and rising demand across the platform, even as investors once again focused on a few near-term concerns. The core story here hasn’t broken.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

ServiceNow is still expanding, deepening its role in the enterprise, and finding new ways to monetize artificial intelligence (AI) rather than being threatened by it. If anything, the pullback has made the stock more attractive by pushing valuation into more reasonable territory. That is why I remain bullish on NOW stock.

Q1 Results: Another Excellent Quarter

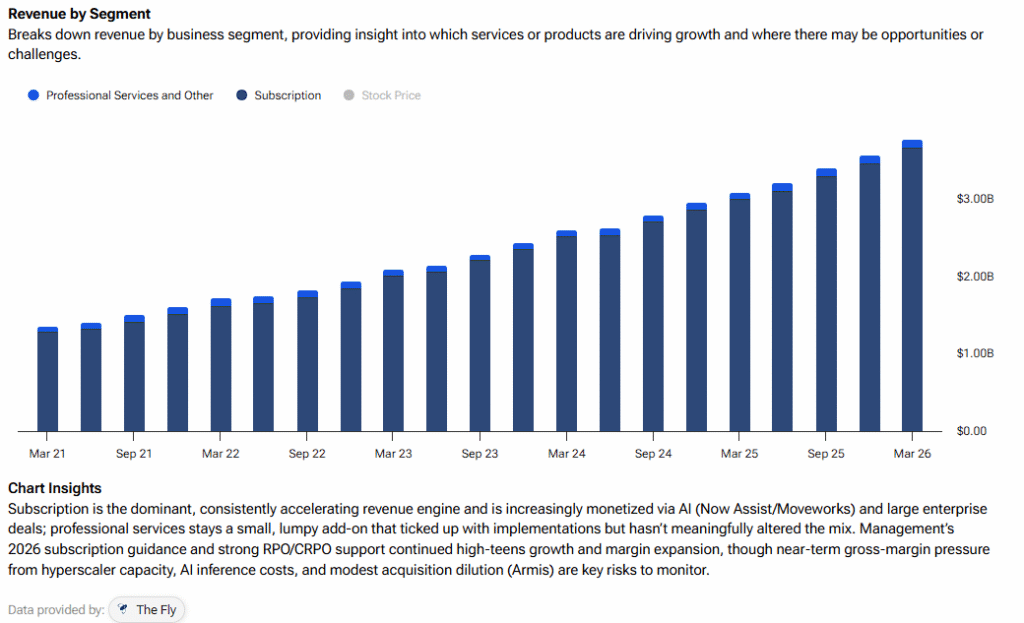

Despite investors’ prolonged pessimism about ServiceNow, its Q1 results were once again excellent. The company posted revenue of $3.77 billion, up 22% year-over-year and ahead of its own guidance. However, the part that really stands out is subscription revenue, which reached $3.67 billion. I would argue this is quite impressive in an environment where investors are constantly worried that enterprise software spending will slow. Instead, ServiceNow is still putting up growth that looks unusually solid for a company at this scale.

Margins were strong too, with adjusted non-GAAP operating margin reaching 32%. That is usually what you want to see from a company at this stage. ServiceNow is still investing big, but without sacrificing profitability or cash generation. Moreover, on the call, management sounded confident, noting that ServiceNow is becoming more central to how companies manage AI across the business, not less relevant because of it. That is the key point.

While some worry AI could make parts of software easier to replace, ServiceNow is trying to make itself the system companies rely on even more. The guidance increase backs that up, with full-year subscription revenue now expected to be nearly $15.8 billion.

Interestingly, growth is no longer coming solely from Information Technology (IT); ServiceNow is expanding across Human Resources (HR), customer service, and workflow tools broadly. This makes the story much bigger, as the AI piece adds to it. Products like Now Assist are scaling quickly because they help companies automate routine work practically. So customers are naturally spending. I believe that instead of AI weakening the software model, it is giving ServiceNow another reason to become more deeply embedded in how large companies operate.

The Mid-East Speed Bump and the Margin Mirage

So, why did the stock extend its sell-off after the earnings report? Well, it feels like the market was looking for any excuse to sell, and they found it in a couple of factors that, in my view, are totally overblown. For starters, management flagged some delayed deal closures in the Middle East due to regional geopolitical tensions, which created a 75-basis-point headwind. The market interpreted “delays” as “the end of growth,” ignoring that CFO Gina Mastantuono confirmed some of those deals had already closed in April.

Second, there were some grumbles about gross margins contracting slightly to 81.5%. Some analysts are worried that the cost of running AI infrastructure will eat the business alive. Nevertheless, I view this as an investment phase. You can’t build a world-class AI platform without spending a little on the plumbing.

The market is treating this like a lasting loss of profitability rather than a strategic spend that is already driving more than 130% year‑over‑year growth in customers spending over $1 million on its AI product, Now Assist. It’s a classic case of missing the forest for the trees.

Generally, the “SaaS-pocalypse” narrative has created a cloud of fear over the entire sector. Then again, ServiceNow’s Q1 results showed absolutely no sign of a slowdown. In fact, they showed acceleration in new logo wins and net‑new annual contract value (ACV), with several segments posting more than 50% year‑over‑year growth. When you have a company growing that fast while retaining such a sticky customer base, a sell-off like this could be a gift.

NOW’s Valuation Is Too Cheap

Now, following the recent plummet, ServiceNow is trading at levels we haven’t seen in a long time relative to its earnings power. The consensus earnings per share (EPS) estimate for FY2026 now stands at $4.12. This implies a forward P/E of just under 22x at today’s share price levels. It is rather bizarre for a “Rule of 50+” company, meaning its growth rate plus margin exceeds 50, to be trading at a multiple usually reserved for much slower-growing legacy firms.

Even if ServiceNow doesn’t achieve a single basis point of margin expansion from here, which is unlikely given its scale, EPS is still set to rise at over 20% per year just by tracking revenue growth. At 22x earnings, you are essentially getting that growth for free. I believe the market is so blinded by the “AI threat” that it’s ignoring the “AI reality” of ServiceNow, becoming more profitable and more essential today than it was a few years ago.

Is NOW Stock a Buy, Sell, or Hold?

Despite the stock’s prolonged sell-off, ServiceNow still has a Strong Buy consensus rating on Wall Street, based on 34 Buy, four Hold, and just one Sell ratings. Furthermore, NOW’s average price target of $143.03 implies roughly 58.13% upside potential over the next 12 months.

Final Thoughts on the Opportunity

The current disconnect between ServiceNow’s operational excellence and its share price marks a rare opportunity in my book. The market focuses on temporary geopolitical disruptions and infrastructure costs, while the company is quietly cementing its position as the backbone of the AI-driven enterprise. At 22x forward earnings, the risk-to-reward ratio is heavily tilted in favor of the bulls. I’m staying the course and selling long-term out-of-the-money (OTM) puts at these levels. I am Long NOW.