As energy production transitions towards cleaner energy, companies like TransAlta (TAC) grapple with the dual imperatives of providing greener energy practices while maintaining shareholder value. This Canadian power producer is at a significant junction and is closely watched by market participants for decisive moves to unlock future growth potential. Recently announced quarterly results were in line with the company’s expectations, though marked a pullback in revenues.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The stock has jumped roughly 9.5% in the past few days, and the shares currently offer relative value, suggesting the company presents an appealing option for investors looking for clean energy exposure. Still, more conservative investors might want to hold off and look for further confirmation of improvement in the company’s financial results before taking action.

TransAlta Powering Meta’s Clean Energy Goals

TransAlta is a company focused on developing, producing, and selling electric energy. Its assets include hydroelectric, wind and solar, gas, and coal electrical-generating capacities. TransAlta also has battery storage facilities and is involved in power, natural gas, and environmental product trading.

Significant recent events include the start of commercial operations at its 200 MW White Rock East and Horizon Hill wind facilities in Oklahoma, which are expected to contribute over $100 million to the company’s adjusted EBITDA annually. In particular, the Horizon Hill Wind Project concluded a significant construction program in 2021, adding 800 MW of contracted renewable electricity to TransAlta’s portfolio.

This further expands the company’s U.S. renewables fleet to over one GW and has attracted Meta Platforms Inc. (META) as a customer, who has contracted the facility’s total capacity to provide clean electricity to support Meta’s goal of powering its operations with 100% wind and solar energy.

TransAlta’s Recent Financial Results & Outlook

The company posted financial results for Q2 2024, experiencing higher operational efficiency, with adjusted availability increasing to 90.8% from 84.6% in the previous year. Production also showed a growth of 4.02%, with figures standing at 4,781 GWh against last year’s 4,596 GWh. However, despite the operational growth, revenues and earnings decreased to C$582 million and C$94 million, respectively, against last year’s C$625 million and C$79 million. Adjusted EBITDA of $312 million, compared to $387 million for the same period in 2023, and earnings per share (EPS) of C$0.18 marked a decline from the previous year’s C$0.23.

As of quarter end, the company reported available liquidity of C$1.7 billion, including C$350 million in cash. The company’s Board of Directors has also announced a quarterly dividend of C$0.06 per common share, equating to a dividend yield of 2.53%.

Management has given guidance for 2024, projecting an Adjusted EBITDA range of C$1,150 million – 1,300 million. The Free Cash Flow (FCF) is expected to fall between C$450 million – 600 million, with FCF per share ranging from C$1.47 – 1.96. An annualized dividend per share is pegged at C$0.24.

What Is the Price Target for TAC Stock?

The stock had been on a downward trend for much of the past year, but it turned a corner and rebounded, climbing 11.84% in the past three months. The shares trade near the middle of the 52-week price range of $5.90 – $10.18 and show positive price momentum, trading above the 20-day (7.07) and 50-day (7.01) moving averages. With a P/S ratio of 1.01x, the stock trades at a relative discount to the Independent Power Producers industry, which sports an average P/S ratio of 1.43x.

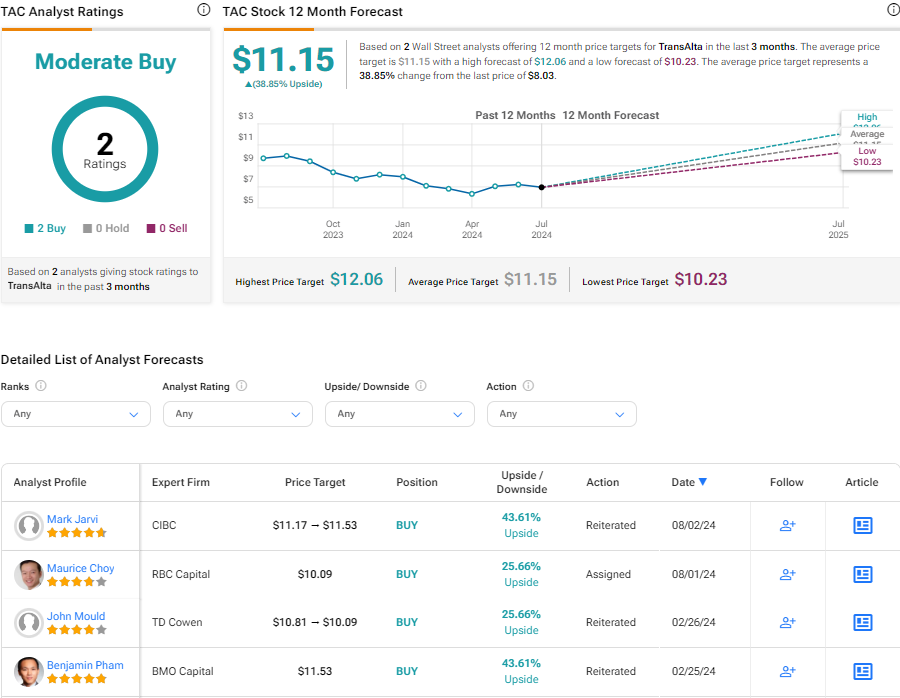

Analysts covering the company have been constructive on the stock. TransAlta is rated a moderate buy based on the most recent recommendations and price targets issued by two analysts. The average price target for TAC stock is $11.15, representing a potential 38.85% upside from current levels.

Final Thoughts on TransAlta

TransAlta is making promising strides in renewable operations. Despite a slight dip in revenues and earnings, the firm’s latest developments – including the initiation of operations in Oklahoma’s Horizon Hill and White Rock East wind facilities – are expected to significantly enhance its annual adjusted EBITDA. Its growing appeal has made it a potentially appealing target for investors seeking to add clean energy exposure to their portfolio.