Palantir Technologies (PLTR) stock has pulled back about 8% over the past month, bringing the year-to-date decline to more than 19%. Despite the data analytics company’s impressive fundamentals, PLTR stock has been under pressure due to concerns about its lofty valuation, fears of disruption by AI startups like Anthropic, and a shift to safer bets amid geopolitical tensions. Ahead of Palantir’s Q1 earnings on May 4, most analysts covering the stock remain bullish on its prospects and see strong upside.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

On Friday, campaigners from Minneapolis urged the Swiss National Bank (SNB) to sell its $1.1 billion stake in Palantir, citing the role of its technology in the U.S. immigration crackdown. However, according to Reuters, SNB chairman Martin Schlegel defended the central bank’s investment strategy, saying that its huge foreign-currency portfolio was designed to support its monetary policy.

Meanwhile, Wall Street expects Palantir to report EPS (earnings per share) of $0.28 for Q1 2026, reflecting 115% year-over-year growth. Revenue is projected to rise 74% to $1.54 billion. Palantir has been delivering rapid growth across its government and commercial businesses, driven by the demand for its Artificial Intelligence Platform (AIP). Investors will focus on the company’s ability to sustain its strong momentum, especially given ongoing concerns about AI disruption. In fact, short seller Michael Burry commented earlier this month that Anthropic is “eating Palantir’s lunch.”

Analysts’ Views Ahead of Palantir’s Q1 Earnings

Recently, D.A. Davidson analyst Gil Luria reiterated a Hold rating on Palantir stock following a webinar with Duane Massie, the founder and CEO of SigmaIQ (a Palantir partner for managed services), and Ryan Mead, Head of Commercial at SigmaIQ. The 4-star analyst highlighted that the discussion was focused on PLTR’s “competitive differentiation” as AI innovation continues to transform the market. The discussions increased Luria’s confidence in PLTR’s dominant position and its ability to sustain long-term growth.

He highlighted that Duane and Ryan dismissed the narrative that frontier model providers will displace Palantir and added that the company works alongside top AI model providers to help enterprises scale AI across the whole business, avoiding siloed use. In fact, demand for PLTR’s platform has increased since the start of the “AI craze catalyzed by continued innovation from frontier model providers.”

While Luria believes that “Palantir is the best story in all of Software,” he remains on the sidelines only due to the stock’s valuation.

Meanwhile, William Blair analyst Louie DiPalma reiterated a Buy rating on PLTR stock, noting that the Department of Defense’s budget request, which included a $2.3 billion funding request for Palantir’s Maven Smart System (MSS), provides multiyear visibility relative to his estimated $500 million-plus revenue run-rate. Given the recent selloff, the 4-star analyst believes that there is now a “clear valuation basis” to buy PLTR stock. He explained that while PLTR stock appears expensive when valued using a sales multiple, its valuation is “reasonable” based on free cash flow.

Is PLTR a Good Stock to Buy Now?

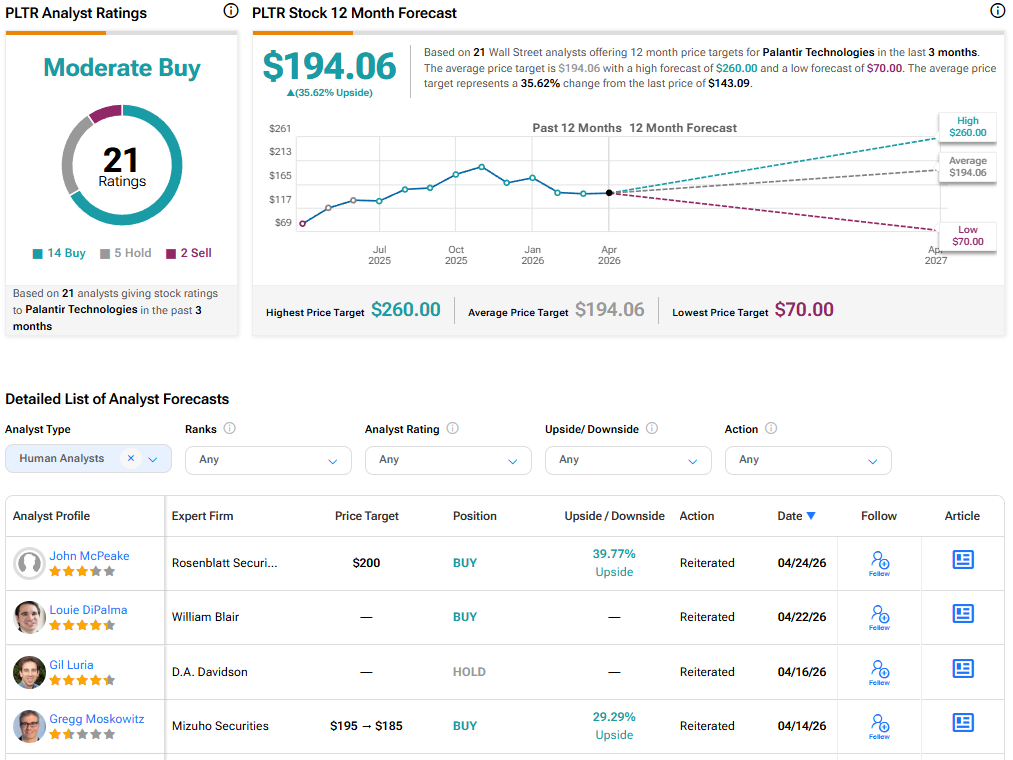

Heading into Q1 earnings, Wall Street has a Moderate Buy consensus rating on Palantir Technologies stock based on 14 Buys, five Holds, and two Sells. The average PLTR stock price target of $194.06 indicates 36% upside potential.