Nvidia (NASDAQ:NVDA) moved lower last week as investors digested earnings reports from the hyperscalers. It’s an interesting dance between Nvidia and these major tech companies, which play dual roles as both customers and potential competitors.

Claim 55% Off TipRanks

Forget margin or options. Here's how the pros trade NVDAFor Nvidia, its position at the top of the GPU market has driven record-breaking growth quarter after quarter. Demand for the company’s hardware shows no signs of slowing, and the broader trend in hyperscaler spending continues to build.

Just last week, both Amazon and Alphabet confirmed this trajectory (Alphabet even raised its expected spending for 2026). However, there’s another side to this coin, as both hyperscalers are developing their own silicon solutions.

That’s the narrative investors ran with, viewing it as a zero-sum game where progress with Google’s TPUs and Amazon’s Trainium chips would, by definition, come at the expense of Nvidia’s future sales. Alphabet announced plans to sell TPUs to select cloud customers for use in their own data centers, while Amazon said its chips business had surpassed $20 billion in ARR.

Believing that the company’s hardware moat is becoming “less absolute,” long-time Nvidia fan Beth Kindig is taking her foot off the gas pedal, at least for the next few years.

“While I still believe Nvidia Corporation will reach $20 trillion by 2030, I believe much of that 310% return is likely to be back-half weighted in the years of 2028-2030,” explains the 5-star investor.

It’s not just the rise of custom silicon behind this shift, Kindig argues. Nvidia’s CUDA software ecosystem, long a cornerstone of its dominance during the AI training phase, is starting to carry less weight as workloads move toward inference and alternative serving platforms and frameworks gain traction.

Another concern for the investor is the reported Rubin delays due to the worldwide shortage of HBM4 memory products. Kindig calls this “terrible timing,” as it gives custom silicon more time to catch up with Nvidia’s next-gen products while providing additional incentive for hyperscalers to diversify their supply chain.

That doesn’t mean that she’s losing faith in Nvidia’s long-term prospects, however. Kindig is adamant that the company’s multiyear catalyst, i.e., its strong product roadmap, remains intact. However, she worries that the market is still valuing the company through its hardware moat, just as its durability is starting to soften.

“While an AI enthusiast can sit back, relax and discuss specifications and other fandom, an investor must always answer — is my capital better deployed elsewhere?” asks Kindig.

For this year and next, the long-time Nvidia supporter believes the answer is yes. Kindig is therefore assigning NVDA a Hold (i.e., Neutral) rating. (To watch Kindig’s track record, click here)

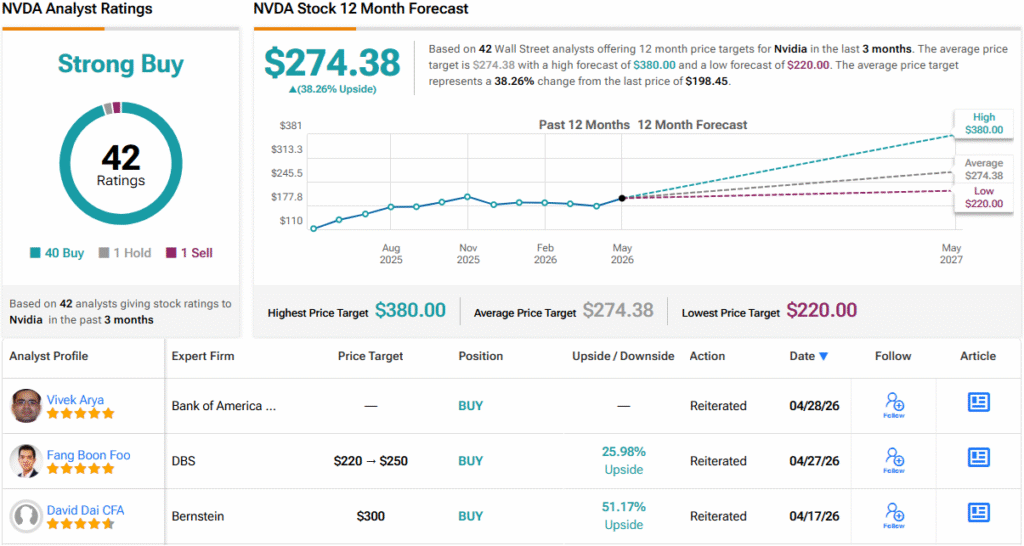

Wall Street clearly won’t be a receptive audience for this message. With 40 Buys, 1 Hold, and 1 Sell, NVDA enjoys a Strong Buy consensus rating. Its 12-month average price target of $274.38 points to a potential upside of 38%. (See NVDA stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.