Seagate Technology (STX) reinforced the artificial intelligence (AI) storage bull case with a strong Fiscal Q3 2026, keeping me bullish on the stock. Record revenue and improving free cash flow suggest that hyperscale AI demand is becoming more durable rather than just a short-term spending spike. The quarter also showed improving operating leverage, with margins and cash generation both rising sharply.

Claim 55% Off TipRanks

Trade STX with leverageSeagate provides mass-capacity data storage technology and solutions globally, with hard disk drives (HDDs) at the center of its revenue model.

Record Revenue Confirms the Demand Floor

The Q3 FY2026 earnings report highlighted a business consistently beating estimates. Revenue rose 44% year-over-year to $3.1 billion against a $2.96 billion consensus, while non-GAAP earnings per share (EPS) of $4.10 topped the $3.50 analyst forecast. The non-GAAP gross margin reached 47%. Management now expects next quarter’s gross margin to increase to more than 50%, an all-time high.

Data center storage dominated the mix, accounting for 80% of revenue and 88% of exabytes shipped. Seagate delivered 199 exabytes, up 39% year-over-year, while data center revenue reached $2.5 billion, up 55% year-over-year and 12% sequentially. Nearline capacity stands nearly fully committed through the end of 2027. For Fiscal Q4, management guided revenue of $3.45 billion, plus or minus $100 million, with non-GAAP EPS of $5, plus or minus $0.2.

One of the most important reasons to own Seagate shares is that the business is generating cash at a level that gives management real flexibility. The latest data shows trailing-twelve-month free cash flow of about $2.63 billion and quarterly free cash flow of $953 million, up 57% quarter-over-quarter. That cash supports debt reduction, dividends, buybacks, and continued investment in next-generation products without forcing the company back into the market for capital.

Heat-Assisted Magnetic Recording Sustains the Technology Lead

The structural bull case for STX also rests on heat-assisted magnetic recording (HAMR) technology, which enables higher data density per drive without proportional increases in unit shipments. Mozaic 4, the second-generation HAMR product, began revenue shipments in late March 2026 and delivers up to 44 terabytes (TB) per drive, roughly 30% more than its predecessor. Management expects Mozaic 4 to account for the majority of HAMR exabyte shipments exiting calendar 2026.

Meanwhile, the next-generation product, Mozaic 5, will target 50 TB per drive with qualification shipments planned for late 2027.

In other words, Seagate can grow revenue and margins by raising capacity per unit rather than increasing shipment volumes. As cloud customers demand more storage density per rack, the HAMR lead translates into sustained pricing power and higher dollar content per drive, making the earnings trajectory more defensible than the company’s historical cyclicality suggests.

Balance Sheet and Valuation Risks Ease as Earnings Growth Accelerates

Seagate’s primary investment risk remains its balance sheet. Stockholders’ equity was negative as recently as Fiscal 2025, and leverage levels were high. However, the company has made progress, retiring $641 million of gross debt in the March quarter, bringing year-to-date gross debt reduction to approximately $1.1 billion, and net leverage improved to 0.7x. Given the strengthened financial discipline and consistent cash generation, Fitch Ratings recently upgraded Seagate’s credit rating.

Customer concentration is the other structural concern. Data center customers account for 80% of revenue, so any sustained pullback in hyperscaler capital expenditure would directly affect results. The build-to-order contract framework provides a meaningful buffer, but investors should monitor cloud spending trends and HAMR qualification timelines closely.

At a forward price-to-earnings (P/E) ratio of roughly 30.85x on a next-twelve-months basis, Seagate is no deep-value stock. However, non-GAAP EPS rose 115% year-over-year in Q3, and the Q4 guidance midpoint of $5 implies further sequential acceleration. Furthermore, the price/earnings-to-growth (PEG) ratio of about 1.01 suggests earnings growth still offers meaningful value relative to the headline multiple. Finally, Seagate stock supports a dividend yield of about 1.02%.

As long as Seagate continues to meet its HAMR milestones and maintains its high operating margin, I believe the stock has room for multiple expansion.

Three ETFs for Diversified Technology Exposure

For investors seeking diversified technology exposure without the STX single-stock risk, three exchange-traded funds (ETFs) may provide structured alternatives to owning Seagate directly. The Roundhill Memory ETF (DRAM), with approximately 5% STX weighting, targets the global memory and storage hardware ecosystem. The Invesco AI and Next Gen Software ETF (IGPT), which holds about 3.3% STX, provides broader exposure to AI infrastructure across storage, software, and semiconductors.

Finally, the Harvest Tech Achievers Growth & Income ETF (HTA), with roughly 5% STX, blends tech growth with dividends for yield-oriented portfolios.

Is STX a Buy, Sell, or Hold?

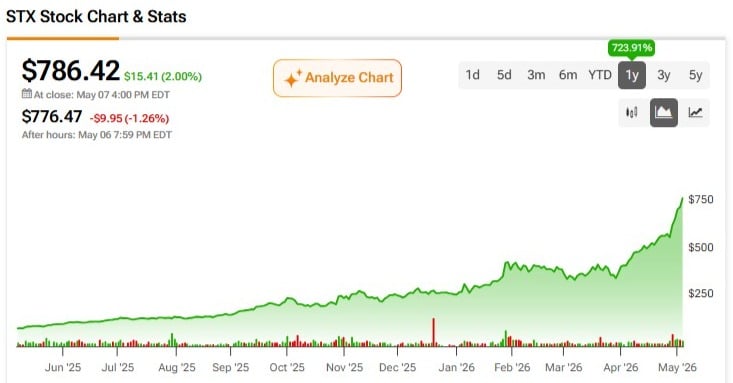

Seagate Technology currently carries a Strong Buy consensus rating on TipRanks, based on 17 analyst ratings assigned in the past three months, consisting of 14 Buys, three Holds, and no Sells. The average 12-month price target for STX is $758.94, implying a downside of approximately 3.4% from the current share price of $786.42.

Conclusion

I remain bullish on STX because Seagate’s results reflect a company in a structural upcycle, not at a cyclical peak. Record free cash flow, confirmed order visibility through calendar 2027, an accelerating HAMR roadmap, and a positive outlook by management are not typical of a business approaching peak earnings.

The balance sheet and customer concentration risk deserve continued monitoring, but the direction of travel on both fronts looks positive. For investors willing to accept the single-stock and customer-concentration exposure, STX presents a compelling case that earnings power has been durably upgraded.