SanDisk (SNDK) stock was down about 6% in Friday’s pre-market trading despite reporting market-beating results for the third quarter of Fiscal 2026, driven by robust demand for data storage solutions. SNDK stock has rallied more than 360% year-to-date and 3,300% over the past year, as the artificial intelligence (AI) boom has sparked the demand for memory and storage solutions. Some analysts think that the post-earnings sell-off reflected profit-booking by investors following a stellar rally.

Claim 55% Off TipRanks

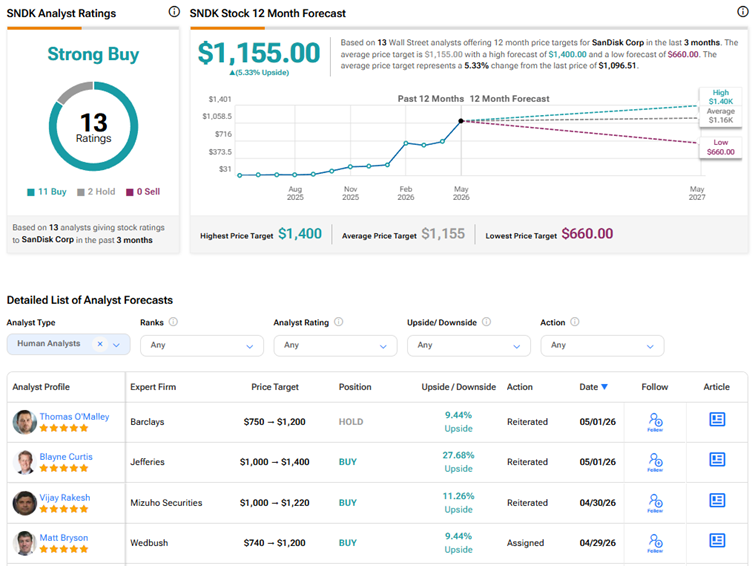

New trading tool for SNDK bullsSanDisk Delivers Strong Q3 Earnings

SanDisk reported a 251% year-over-year jump in its Q3 FY26 revenue to $5.95 billion, way ahead of the Street’s expectation of $4.72 billion. Meanwhile, adjusted earnings per share (EPS) of $23.41 crushed the consensus estimate of $14.62 and reflected a significant improvement from an adjusted loss per share of $0.30 in the prior-year quarter.

The notable surge in profitability reflected higher revenue and a jump in gross margin to 78.4% from 22.7% in Q3 FY25. SanDisk is benefiting from a shift in its mix toward the “highest-value end markets,” mainly data centers.

CEO David Goeckeler said the company is moving to a new business model built on multi-year customer engagements that are supported by financial commitments. SanDisk expects this transformation to drive higher and more durable earnings power.

Looking ahead, SanDisk expects fiscal fourth-quarter revenue in the range of $7.75 to $8.25 billion and adjusted EPS between $30 and $33.

Analysts React Positively to Q3 Print

Following the Q3 FY26 results, Mizuho analyst Vijay Rakesh increased his price target to $1,220 from $1,000 and reiterated a Buy rating. The 5-star analyst noted the solid Q3 results and the strong Q4 FY26 revenue guidance, which was well ahead of the Street’s consensus of $6.65 billion. Rakesh also highlighted SanDisk’s robust gross margin outlook, which reflects pricing tailwinds.

He added that pricing remains strong, with supply expected to remain tight through 2026. The analyst estimates the Q4 FY26 average selling price (ASP) to rise by 22%. Rakesh also noted SanDisk’s transition to a new business model, with a remaining performance obligation (RPO) of $42 billion across three customers, and upside potential from adding two customers and higher pricing trends.

Meanwhile, Bank of America Securities analyst Wamsi Mohan increased his price target for SanDisk stock to $1,550 from $1,080 and reiterated a Buy rating. Mohan noted the company’s strong Q3 beat and “massively” better-than-expected Q4 FY26 outlook. He observed that while bit shipments were down quarter-over-quarter, datacenter bits grew double digits while consumer and client bits declined. The 5-star analyst added that pricing was strong across the board (up 137% quarter-over-quarter), resulting in 233% sequential growth in data center revenue.

Mohan highlighted that SanDisk signed three multi-year deals (new business models or NBMs) in Q3 FY26 and two additional contracts in Q4, with active talks with “several other customers.” The three deals will provide at least $42 billion in contractual revenue, with the company guaranteed $11 billion in payments in the event of contract termination. The analyst believes this arrangement offers some protection to SanDisk in a downcycle, when customers could pull back on capacity commitments. Overall, the analyst remains bullish on “valuation, undervalued JV [joint venture] assets, eSSD [enterprise solid state drives] share gains in C26, & long-term potential for industry consolidation.”

Is SNDK a Good Stock to Buy Now?

Given robust demand tailwinds, Wall Street has a Strong Buy consensus rating on SanDisk stock based on 11 Buys and two Holds. The average SNDK stock price target of $1,155 indicates 5.3% upside potential.

This price target could be revised as more analysts react to SanDisk’s Q3 FY26 results and outlook.