SanDisk (SNDK) and Western Digital (WDC), two key players in the memory and storage space, saw their price targets raised by Cantor Fitzgerald, reflecting strong demand trends and improving pricing. Top Cantor analyst C.J. Muse raised his price target on SanDisk to $1,400 (from $1,000) and on Western Digital to $500 (from $420), while maintaining Overweight ratings on both stocks.

Claim 55% Off TipRanks

Forget margin or options. Here's how the pros trade WDCIt is worth noting that Muse ranks 11 out of more than 12,000 analysts tracked by TipRanks. He has a success rate of 77%, with an average return per rating of 73.90% over a one-year timeframe.

For reference, both SanDisk and Western Digital are set to report third-quarter Fiscal 2026 results on Thursday, April 30. For SNDK, Wall Street expects revenue of $4.69 billion and earnings per share (EPS) of $14.45. Meanwhile, WDC is projected to post EPS of $2.40 on revenue of $3.25 billion.

Why the Analyst Is Bullish on SanDisk

For SanDisk, the analyst expects another strong beat and raise, driven by broad demand across hyperscale, consumer, and client markets. At the same time, tight supply is pushing prices higher, which is supporting earnings growth.

In addition, Muse believes SanDisk could soon announce long-term supply agreements, similar to those seen in the DRAM market. These deals could improve pricing visibility and create a more stable revenue base.

Reflecting stronger pricing trends, the analyst raised his estimates. He now expects 2026 revenue and EPS of $29.3 billion and $110, and 2027 revenue and EPS of $34.0 billion and $125 — both well above consensus.

Looking ahead, limited capacity expansion in NAND is likely to keep supply tight through 2028, which could extend the current cycle. As a result, SanDisk remains a top pick.

Western Digital Benefits from Pricing and Margin Upside

Turning to Western Digital, the analyst also expects a strong beat and raise, supported by robust nearline demand. Customers are shifting toward higher-capacity products, which is helping drive pricing higher.

At the same time, cost reductions are expected to support margin expansion. Muse sees a path to over 50% gross margins in the near term, with potential to reach 60% by late 2028.

Another key factor is the balance sheet. Following the monetization of its SanDisk stake, Western Digital now has no debt. This positions the company to return more cash to shareholders through buybacks and dividends, with over $9 billion in repurchases possible through 2028.

Given these trends, the analyst raised his estimates to $14.7 billion in revenue and $12.55 EPS for 2026, and $18.2 billion and $18.50 for 2027, both above consensus expectations.

Which Is the Better AI Memory Stock, According to Analysts?

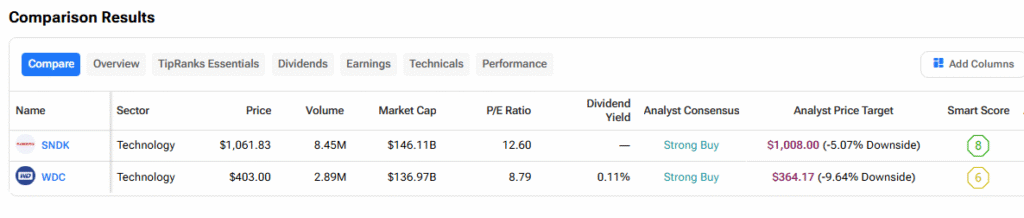

Turning to Wall Street, both SanDisk and Western Digital carry a Strong Buy consensus from analysts. SNDK has an average price target of $1,008.00, implying about 5% downside from current levels.

Similarly, WDC’s average price target of $364.17 suggests roughly 10% downside, pointing to more limited near-term upside for both stocks despite their bullish ratings.