Rivian (RIVN) stock fell 8.4% on Friday even after the electric vehicle (EV) maker reported a narrower-than-anticipated loss for the first quarter of 2026. Investors were disappointed by the decline in gross profit, warnings about margin pressure stemming from the R2 launch, and continued cash burn. Let’s look at the reactions of analysts from Mizuho, Needham, and Goldman Sachs to Rivian’s Q1 performance.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Mizuho Remains Bearish on RIVN Stock, While Needham Stays Bullish

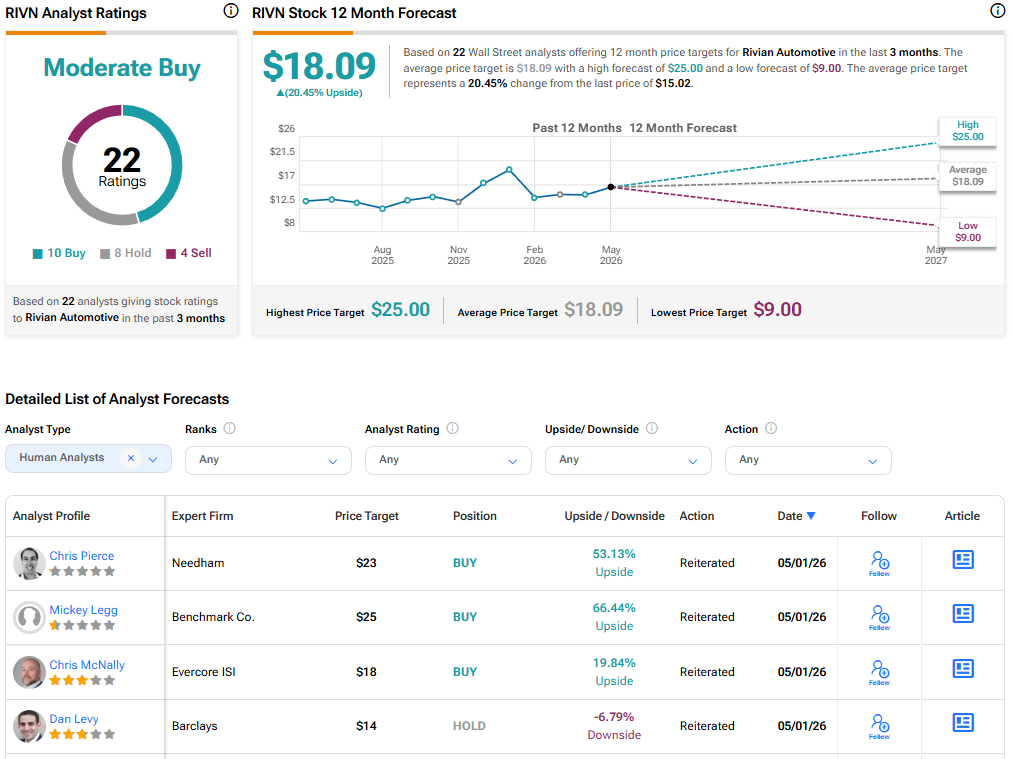

Mizuho analyst Vijay Rakesh raised his price target for RIVN stock to $13 from $11 and reiterated a Sell rating. The 5-star analyst noted that Q1 revenue of $1.38 billion was almost in line with the consensus, and the company reiterated its previous guidance of about 64,500 deliveries for 2026 (at the midpoint). He noted that Rivian’s R2 production is on track, with deliveries expected to be weighted toward the second half of the year.

Rakesh highlighted that R2 is expected to be dilutive to Q2 and Q3 2026 margins, with a rebound expected in the fourth quarter. While Rivian continues to execute, the analyst remains bearish on the stock due to challenges in the North American EV market.

In contrast, Needham analyst Chris Pierce reiterated a Buy rating on RIVN stock with a price target of $23, citing “R2 now transitioning from narrative to reality as saleable production begins and customer deliveries approach.” The analyst noted that early signs of vehicle readiness indicate Rivian can grow beyond its core audience, but successful execution will be critical.

Pierce added that Rivian’s decision to expand the Georgia Phase 1 plant’s capacity to about 300,000 units reflects a solid demand outlook over the medium term, but also makes the full build-out increasingly dependent on strong execution. While the EV demand backdrop remains softer than expected, the analyst continues to see upcoming delivery milestones and early conversion trends as key catalysts to improve sentiment and support a more meaningful ramp into 2027.

Goldman Sachs Retains Hold Rating

Meanwhile, Goldman Sachs analyst Mark Delaney slightly lowered his price target for Rivian stock to $16 from $17 and reiterated a Hold rating. The 5-star analyst remains constructive on Rivian’s long-term opportunity, citing R2 volume growth and the company’s ability to grow its software & services business, including its autonomous capabilities. Delaney also noted that Rivian continues to expect to start deliveries later in Q2 2026. He expects the served market for R2 across the U.S. and Europe to be about 4 million units, compared to about a 1 million addressable market size for the R1 in the U.S.

That said, Delaney thinks it’s still early to assess the ramp rate and R2 volumes, and whether it will help Rivian deliver positive free cash flow. Given the still-limited visibility into the magnitude of R2 profit contribution, especially amid the existing supply chain backdrop and ongoing cash use, the analyst prefers to stay on the sidelines.

“However, if we become incrementally positive on the trajectory for Rivian’s profits over the next 12-24 months, then we could be more constructive on the stock,” concluded Delaney.

Is Rivian Stock a Buy, Sell, or Hold?

Overall, Wall Street has a Moderate Buy consensus rating on Rivian stock based on 10 Buys, eight Holds, and four Sells. The average RIVN stock price target of $18.09 indicates 20.5% upside potential.

These price targets/ratings could be revised as more analysts react to Rivian’s Q1 results.