EV maker Rivian Automotive (RIVN) reported its Q1 earnings last week. Our AI analyst has kept a neutral view of the stock following those results.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

TipRanks’ A.I. Stock Analysis tool has reiterated a Neutral rating on the stock. It assigns Rivian a score of 46. Its price target is $14, which implies a 1.93% downside.

Weak Financial Performance

For context, TipRanks’ AI Stock Analysis provides automated, data-backed evaluations of stocks across key metrics, offering users a clear and concise view of a stock’s potential.

In summary, our AI analyst said that Rivian’s score is held down primarily by weak financial performance – large ongoing losses, heavy cash burn, and higher leverage – and a technically weak price trend being below major moving averages.

Offsetting this, the earnings call last week showed tangible strategic progress and improved liquidity with R2 launch progress, targeted cost reductions, and strong Software & Services growth. However, near-term profitability guidance remains challenging.

As seen below, its share price is also trailing the S&P 500 quite significantly.

Feeling Positive

Let’s look in more detail at some positive factors identified by our AI analyst.

- Software & Services Recurring Revenue – Sustained 49% YoY growth in Software & Services (Q1 revenue $473 million, $181 million gross profit) builds a higher-margin, recurring revenue stream. Over 2–6 months, this diversifies revenue, improves blended gross margins and provides profitable cash flow leverage as vehicle hardware scales.

- Strengthened Strategic Funding & Partnerships- Material partner capital, plus cash and DOE financing, meaningfully extends runway. This durable funding reduces short-term dilution risk, underpins Georgia plant build and R2 ramp, and supports capex and autonomy investments through multi‑year execution.

- R2 Cost Reductions and Production Scaling – Structural R2 cost targets (BOM ~50% of R1, non‑BOM >50% lower) and start of saleable R2 production create durable unit‑economics improvements. If achieved, these reductions materially lower break‑even volumes and support sustainable automotive gross margins as scale increases.

Feeling Negative

- Large Cash Burn and Negative Free Cash Flow – Persistent negative operating and free cash flow means the business remains reliant on external capital to fund operations and capex. Over the medium term this constrains strategic optionality and raises refinancing exposure if markets tighten.

- Elevated Leverage and Large Debt Stock – Elevated leverage combined with ongoing losses increases financial risk. Over 2–6 months, higher interest and covenants (notably DOE loan terms) limit flexibility for incremental spend or financing and raise exposure to adverse macro or commodity moves.

- Ramp Complexity and Margin Headwinds – R2 back‑half ramp, launch complexity, regulatory credit volatility and ramp‑related costs (depreciation, SBC) depressed automotive margins. These execution and mix risks can delay durable margin recovery and keep adjusted EBITDA losses elevated through the ramp period.

Is RIVN a Good Stock to Buy Now?

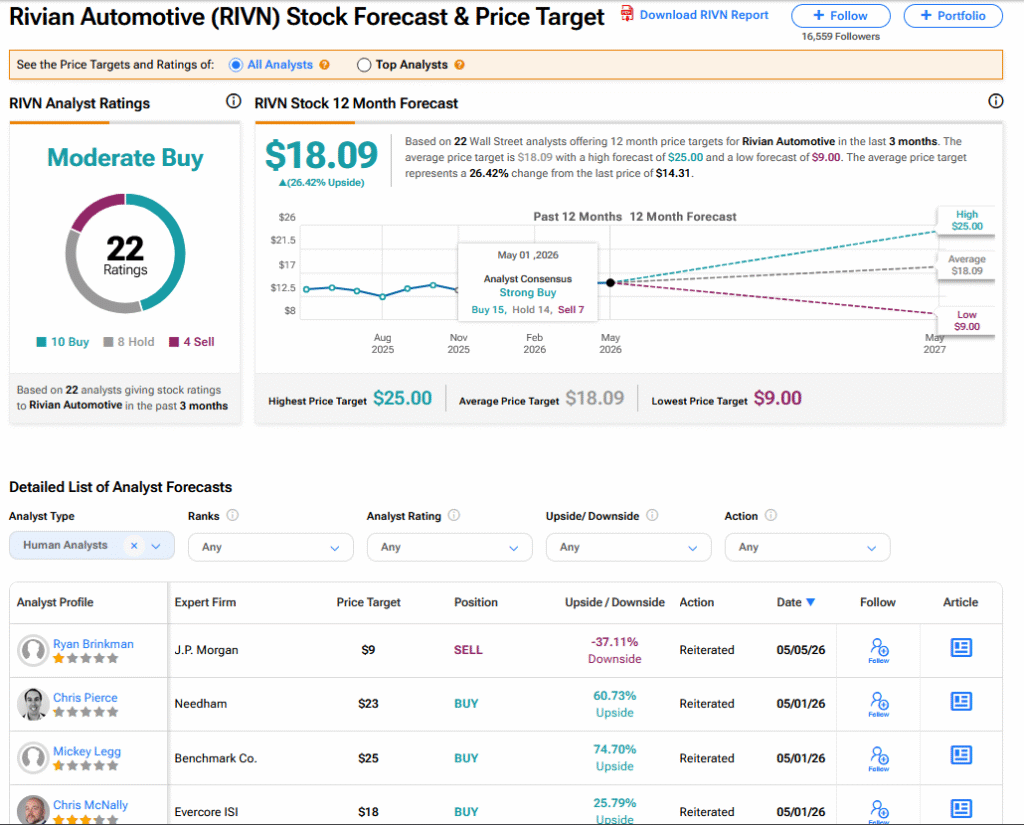

On TipRanks, RIVN has a Moderate Buy consensus based on 10 Buy, 8 Hold and 4 Sell ratings. Its highest price target is $25. RIVN stock’s consensus price target is $18.09, implying a 26.42% upside.