Intel (NASDAQ:INTC) is one of the shining stars this year, seemingly turning its fortunes around just over a year into the tenure of CEO Lip-Bu Tan. The company’s most recent earnings report provided another boost for INTC, which has shot up by more than 30% since last week’s print.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

On the one hand, it’s easy to see why the market responded so enthusiastically. The company’s Q1 2026 revenue of $13.6 billion exceeded guidance by $1.4 billion and represented year-over-year growth of 7%.

Data Center and AI revenue of $5.1 billion grew at an even faster pace of 22% year-over-year. With AI shifting into inference and agentic workloads, CPUs are expected to become increasingly important. That’s created “unprecedented demand for silicon,” as company management was happy to trumpet in its earnings release.

Could this herald even more growth up ahead for INTC’s share price? Top investor Geoffrey Seiler isn’t so sure that’s the right conclusion to draw.

“In my view, Intel just happened to be in the right place at the right time, with hyperscalers now scrambling for server CPUs,” states the 5-star investor, who is among the top 3% of stock pros covered by TipRanks.

Seiler certainly appreciates that Intel has succeeded in growing its revenues. And it wasn’t just the “surging demand” for CPUs that helped boost sales, as the foundry business also saw revenues increase by 16% to hit $5.4 billion.

However, he also points out that the foundry segment’s operating losses were “elevated” at $2.4 billion for the quarter. (“The company still has issues with its foundry business,” he adds.)

Moreover, he’s not convinced that Intel is the right horse to bet on when it comes to CPUs, arguing that AMD is a better play.

“It actually looks much more like a case of the company stumbling into a hot trend than anything else,” adds Seiler.

Of course, the huge jump in the company’s share price has made it significantly more expensive. That’s another reason to avoid jumping into INTC, explains the investor.

“Its valuation is now to the moon,” says Seiler. “I’d stay away.” (To watch Seiler’s track record, click here)

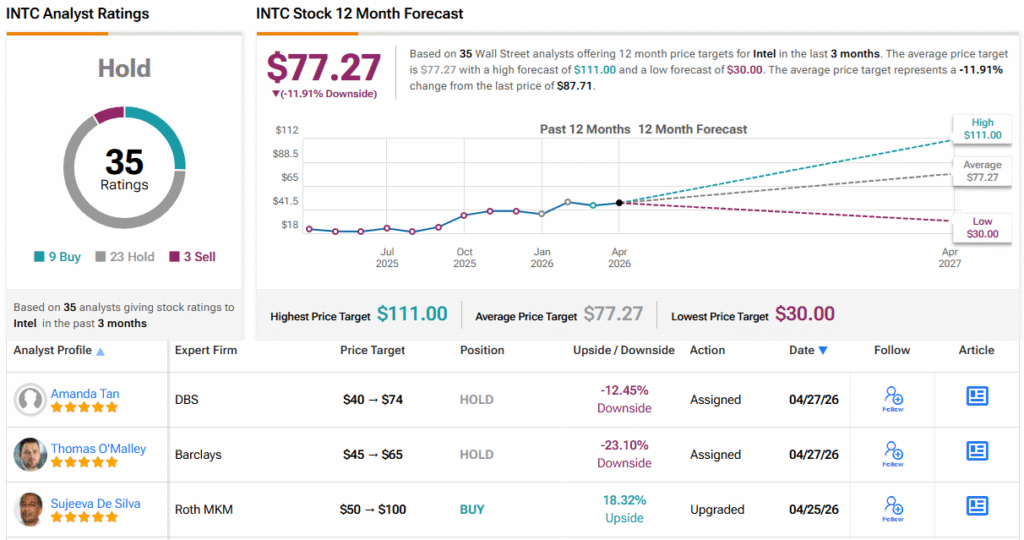

For its part, Wall Street is reflecting a cautious approach. With 9 Buys, 23 Holds, and 3 Sells, INTC carries a consensus Hold (i.e., Neutral) rating. Its 12-month average price target of $77.27 points to losses in the low double-digits. (See INTC stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.