Shares of swimming pool and associated products distributor Pool Corp. (NASDAQ:POOL) are trending lower today after the company posted a mixed set of second-quarter numbers. Revenue dropped 9.5% year-over-year to $1.9 billion but surpassed estimates by $10 million. EPS at $5.89 though, missed expectations by $0.23.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

By top line, this was the second-best quarter for POOL yet with the operating margin rising 220 basis points to 17.6% as compared to pre-pandemic levels. At the same time, the quarter was characterized by a slow start to the swimming pool season while maintenance activity also remained tepid.

The company has managed to pare down its debt by $410.8 million to $1.2 billion at the end of June 2023 and now expects EPS for the year to range between $13.14 and $14.14. At the midpoint, this points to an impressive 21% compounded annual growth in the bottom line from 2019.

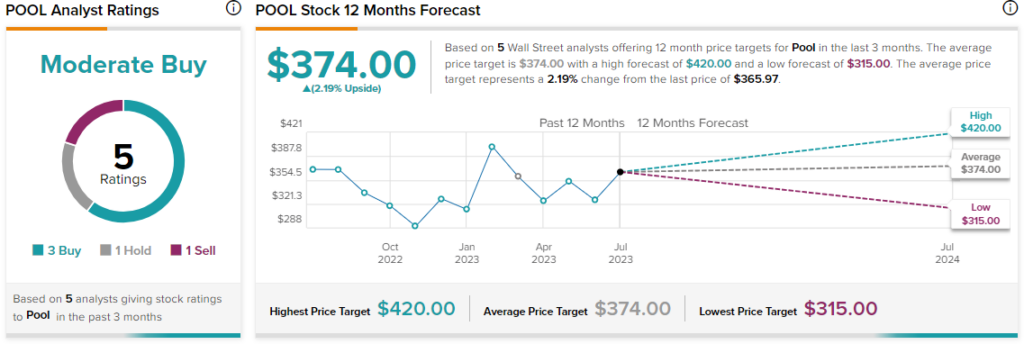

Overall, the Street has a $374 consensus price target on Pool alongside a Moderate Buy consensus rating. Shares of the company have popped nearly 21.6% year-to-date. Concurrently, short interest in the stock remains elevated at about 10.8% at present.

Read full Disclosure