Pfizer (PFE) delivered a solid Q1, reinforcing that the pharmaceutical giant’s core business remains relatively resilient even as COVID-related revenue continues fading into the background. However, I remain bearish on Pfizer because the company still faces significant long-term challenges tied to patent expirations, pipeline uncertainty, and an increasingly competitive drug-development environment.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

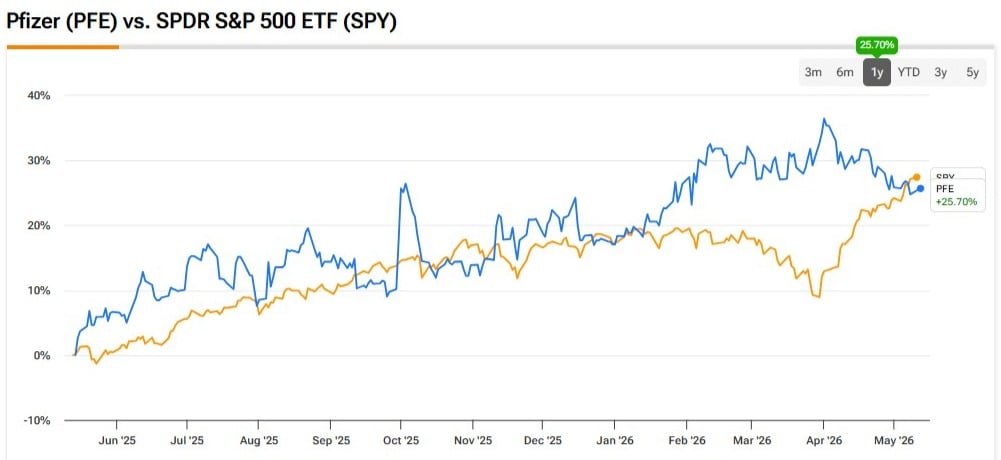

Pfizer’s stock is up nearly 12% over the past 12 months, trailing the S&P 500’s (SPX) gain of more than 30% over the same period. In my view, that underperformance reflects investor skepticism around Pfizer’s ability to return to durable growth after the COVID boom years. While management is emphasizing operational momentum and long-term growth initiatives, I believe the market is still waiting for stronger evidence that Pfizer can successfully navigate the next decade.

Q1 Results Show the Core Business Is Stabilizing

Pfizer’s first-quarter results came out on May 5, and the numbers were clearly better than expected. Revenue came in at $14.5 billion, ahead of consensus estimates of $13.8 billion, while adjusted earnings per share (EPS) of $0.75 topped expectations of $0.72. Importantly, excluding COVID products, operational revenue increased 7% year-over-year.

The quarter also showed encouraging trends across several business segments. Specialty Care revenue climbed 12% year-over-year, driven by continued strength in the Vyndaqel franchise and Xeljanz. Oncology revenue rose roughly 9%, with Padcev continuing to stand out as one of Pfizer’s key growth drivers after expanding 39% year-over-year. The Seagen acquisition is also beginning to look more strategically valuable, with the acquired oncology portfolio delivering 20% operational revenue growth during the quarter.

Management also highlighted positive Phase 3 trial readouts and reiterated its commitment to advancing roughly 20 pivotal studies in 2026. On the surface, this paints the picture of a company with healthy operational momentum and improving execution. Still, I do not think one or two strong quarters fully solve Pfizer’s broader long-term concerns.

The Patent Cliff Still Overshadows the Bull Case

The biggest challenge facing Pfizer remains its looming loss-of-exclusivity (LOE) cliff. Several of Pfizer’s most important products — including Vyndaqel, Eliquis, Ibrance, and Xtandi — face patent expirations between 2027 and 2030. Collectively, these drugs represent billions in annual high-margin revenue.

Management recently gained some breathing room after extending patent protection for Vyndamax-related products through 2031 following settlement agreements with generic challengers. That certainly helps near-term visibility and reduces some downside risk.

However, the broader problem remains intact. Pfizer still faces what many analysts estimate as a $15 billion to $20 billion revenue cliff by the end of the decade. Even if some pipeline assets succeed, there may still be a difficult transition period before new products can fully offset declining legacy revenue. That is why many investors continue to view Pfizer as a “show me” story. Management is targeting high-single-digit revenue growth between 2028 and 2033, but I think those targets still look ambitious given current visibility.

Obesity Could Become a Growth Driver — but Competition Is Brutal

One of Pfizer’s biggest hopes for long-term growth is obesity. The company has continued building out its obesity pipeline following the Metsera transaction and expects multiple Phase 3 studies to advance this year. There is clearly enormous market potential here. Obesity drugs are rapidly becoming one of the largest opportunities in pharmaceuticals, with the total addressable market potentially reaching hundreds of billions of dollars over time.

The issue is that Pfizer is entering an intensely competitive space already dominated by Eli Lilly (LLY) and Novo Nordisk (NVO). Those companies not only have established products but also possess major manufacturing advantages, stronger physician relationships, and deeper commercialization experience in obesity care.

Pfizer’s obesity assets may still become meaningful contributors, particularly if upcoming amylin-combination data impresses investors. However, for now, I see the obesity pipeline more as speculative upside rather than a dependable growth engine that investors can confidently underwrite today.

Margins Could Face Pressure Over Time

Another concern is profitability. Pfizer’s margins have historically benefited from highly profitable blockbuster products. As those products lose exclusivity, margin compression could become a larger issue.

Some Wall Street estimates call for EBIT margin decline toward 30% by 2029 as Pfizer continues investing aggressively in R&D while simultaneously losing high-margin revenue streams.

The company also continues balancing several competing priorities: funding innovation, supporting the dividend, maintaining balance-sheet flexibility, and potentially pursuing acquisitions. That balancing act becomes harder if earnings growth slows.

Valuation Looks Cheap, but Cheap Stocks Can Stay Cheap

On traditional valuation metrics, Pfizer appears inexpensive. The stock trades at a P/E ratio of roughly 14.7, below the sector median of around 17. Its price-to-operating-cash-flow ratio of 12.19 also sits below the sector median of about 14.

The dividend yield, now around 6.70%, will likely continue attracting income-focused investors. Management has also reiterated its commitment to maintaining and eventually growing the dividend.

However, low valuation multiples alone are not enough to make me bullish. In many cases, stocks trade cheaply because the market lacks confidence in future earnings growth. I believe that is exactly the situation with Pfizer today. Without clearer evidence that the pipeline can offset the upcoming LOE headwinds, the stock may continue struggling to achieve meaningful multiple expansion.

Wall Street’s View

According to TipRanks, Pfizer carries a Moderate Buy consensus rating, with eight Buy, 12 Hold, and two Sell ratings. Based on 22 Wall Street analysts offering 12-month price targets, the average target price is $29.22, implying roughly 12.96% upside from the recent share price of $25.87.

Conclusion

Pfizer’s recent operational performance has undoubtedly improved. The company is executing better, oncology momentum looks encouraging, and the core business appears more stable than many feared after the COVID slowdown.

However, I remain bearish on PFE because the long-term picture still lacks clarity. The upcoming patent-expiration cycle is massive, obesity competition is fierce, and management still needs to prove that its pipeline can deliver enough growth to offset future revenue losses. While the valuation and dividend may provide some downside support, I do not yet see enough evidence to justify a more bullish stance on the stock.