PayPal Holdings (PYPL), the U.S.-based digital payments firm, announced during its Tuesday Q1 2026 earnings call that it plans to cut about 20% of its staff and rebuild its business. Following the report, PYPL shares jumped over 3% pre market but later fell by more than 10% as results failed to impress investors. Although its profit and revenue beat Wall Street’s estimates, the firm issued a soft Q2 outlook, sparking a negative market reaction.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

PayPal Bets on Cuts and AI to Turn Things Around

PayPal’s workforce cuts are part of a broader reorganization plan expected to roll out over the next two to three years. The firm had about 23,800 employees at the end of 2024, meaning the cuts could affect more than 4,500 jobs.

Notably, PayPal’s new CEO Enrique Lores said the layoffs are not because of the firm’s earnings results but are aimed at removing excess layers from its structure.

During the earnings call, executives also shared details on the earlier plan to split operations into three business units. This includes a separate division for its Venmo P2P payment platform.

Alongside the job cuts, Lores pointed to plans to employ AI to simplify processes and reduce overlap across teams. However, no clear timeline or specific AI rollout details were provided during the call.

Meanwhile, PayPal said these initiatives are expected to yield at least $1.5 billion in savings over the next two to three years, adding that the full amount will be reinvested to support future growth.

Why PayPal’s Investors Reacted Negatively

PayPal posted stronger-than-expected Q1 2026 results, with revenue rising about 7% year over year to $8.35 billion and EPS coming in at $1.34, above analyst forecasts. Meanwhile, transaction margin dollars, a key profit metric, also grew 3% to $3.8 billion.

However, the positive results were offset by weaker Q2 guidance, which drove the negative market reaction. PayPal said it expects Q2 adjusted EPS to decline about 9% year over year, suggesting that the Q1 strength may not carry over.

At the same time, rising competition from big tech firms like Apple (AAPL) and fintech players such as Klarna (KLAR) and Stripe continues to weigh on growth. Responding to the developments, Evercore ISI (EVR) analysts described PayPal’s results as “a placeholder.” They said that investors are waiting for clearer strategy signals before turning positive on the stock.

Is PayPal Stock a Buy or Hold?

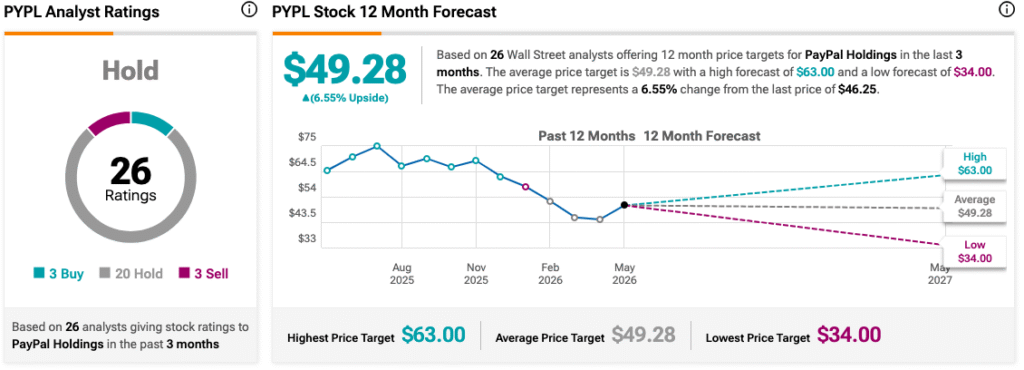

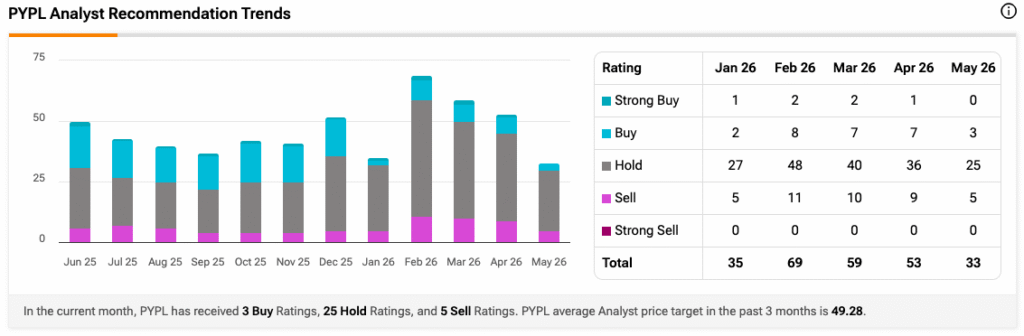

PayPal stock currently carries a Hold rating from 26 analysts tracked by TipRanks over the past 3 months. Out of the 26 analysts, 3 recommend a Buy, 3 suggest a Sell, while 20 rate the stock a Hold. Meanwhile, PYPL’s 12-month price target is projected at an average of $49.28, implying a downside of around 3.02% from its current price. For more information on this stock’s ratings, performance, and price targets, visit the TipRanks Stocks Comparison Center.