After delivering one of the most aggressive re-ratings in the AI trade, Palantir (NASDAQ:PLTR) is running into a more complicated phase. The stock is down by 20% this year as investors reassess just how much of its AI-driven growth is already priced in, with valuation compression across software and rising concerns that generative AI could begin to erode, rather than reinforce, parts of the traditional enterprise software stack.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

That sets up a pivotal moment heading into next Monday’s 1Q26 earnings report. Going into the print, Rosenblatt analyst John McPeake believes the momentum seen in 4Q25 is carrying into 1H26, and anticipates a strong showing and outlook.

“Although there is free-floating anxiety in the market about what AI could do to any company with the label software attached to it, we think Palantir is one of the few software companies actually seeing real growth driven by enterprise AI,” the analyst went on to say.

In addition, despite ongoing geopolitical tensions in the Middle East, McPeake believes Palantir has room to outperform its Q1 targets – projecting revenue and adjusted EBIT growth of 74% and 123% year over year, respectively – while also leaving the door open for an upward revision to full-year guidance, currently set at 61% and 83% growth.

McPeake also notes that recent checks indicate continued strength over the near to medium term. Based on discussions with former commercial and government representatives, Palantir appears to be maintaining the “fast time-to value” of its product suite, with no clear signs of slowing demand in the market. For organisations that have the capacity and resources to implement its solutions, McPeake thinks there is “no faster way to get the full benefits of enterprise AI.”

The analyst also says there appears to be “no substantive deceleration” in revenue growth relative to the 70% reported in Q4 and the 74% guided for Q1, with his expectations slightly above broader Street estimates. McPeake thinks a key differentiator for Palantir vs. other software names is that AI has contributed to a genuine, organic acceleration in its growth rate, whereas other enterprise software vendors have generally seen stable or modestly slowing growth while relying on AI add-ons.

The sense from McPeake’s checks is that over the foreseeable 3-to-5-year horizon, Palantir’s growth outlook appears strong. Beyond that period, however, there are concerns that AI providers could either become direct competitors or be combined with other solutions in ways that replicate its capabilities. How this would happen remains unclear, but McPeake believes this is “one of the key aspects of the software fear trade.”

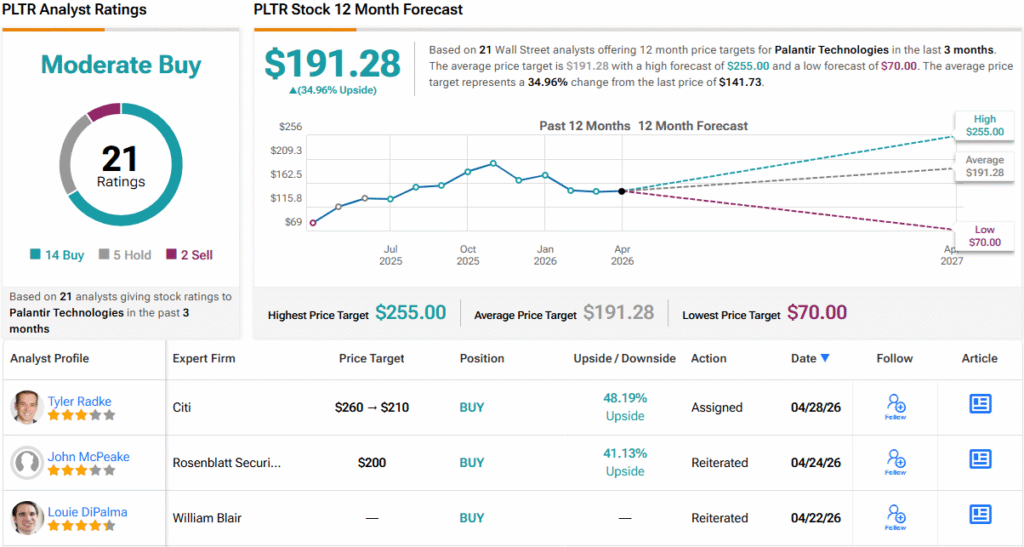

For McPeake, however, Palantir remains a stock to own, assigning a Buy rating alongside a $200 price target, implying a 41% upside over the next 12 months. (To watch McPeake’s track record, click here)

The broader Street leans in the same direction, with 13 analysts joining McPeake on the bullish side, alongside 5 Holds and 2 Sells, resulting in a Moderate Buy consensus for Palantir. The average price target stands at $191.28, implying ~35% upside over the next year. (See PLTR stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.