Palantir Technologies (PLTR) is scheduled to announce its Q1 2026 results on Monday, May 4, after the market closes. Heading into earnings, expectations are running high as the stock remains closely tied to the AI-driven market rally. Investors will be watching whether the company can sustain its strong growth momentum and justify its premium valuation.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

For context, Palantir Technologies is a data analytics and AI software company that helps governments and businesses manage large, complex datasets. Wall Street expects Palantir to report Q1 2026 earnings per share (EPS) of $0.28, which would mark 115% year-over-year growth, while revenue is projected to rise 74% to $1.54 billion. Here are the 3 key things investors should watch closely in the upcoming earnings release.

1. U.S. Commercial Revenue Growth

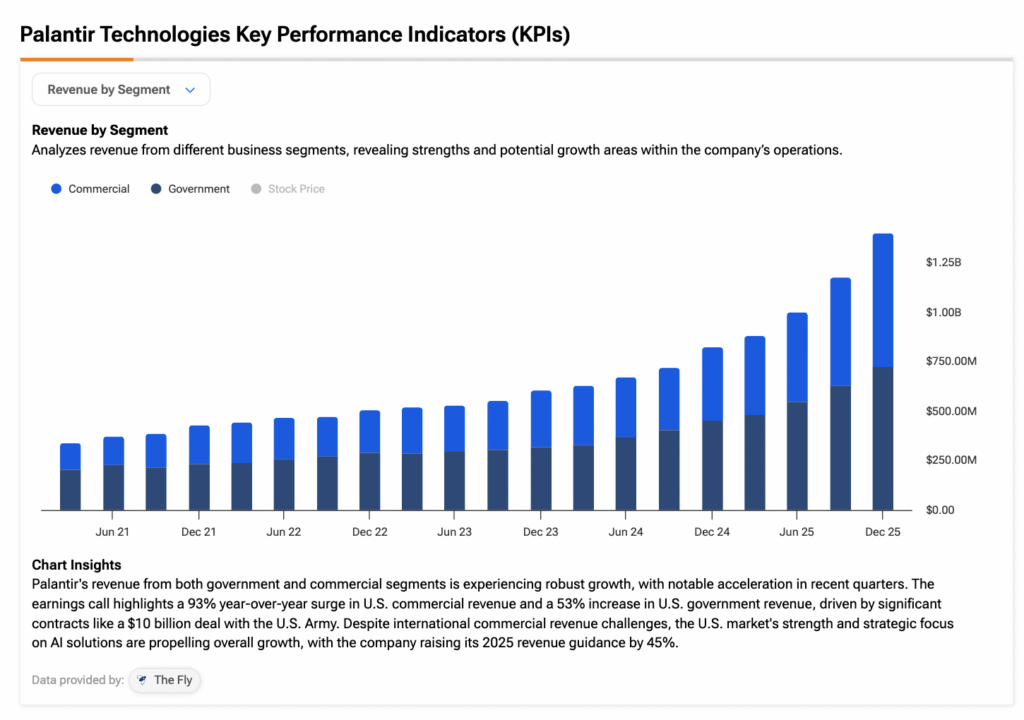

This is the biggest number Wall Street is watching. Investors want to see if strong demand for Palantir’s AI Platform (AIP) was still driving fast growth in its U.S. commercial business. In the previous quarter, U.S. commercial revenue grew 137% year-over-year to $507 million.

Some investors worry that Anthropic could become a bigger competitor and pressure Palantir’s commercial business. However, many believe Palantir’s competitive advantage is stronger than it looks. Its key strength is its ontology layer, which helps organize complex business data into a structured system that AI can use more safely and effectively. Combined with faster sales cycles and deep enterprise integration, this gives Palantir a wider moat and helps protect demand from large business customers.

2. Government Contract Momentum

Palantir is not your typical enterprise software company, as more than half its revenue comes directly from U.S. defense, intelligence, and federal contracts. In 2025, U.S. government revenue grew 55% year-over-year to $1.855 billion.

Any meaningful budget cuts or contract delays hit the company’s top line directly — not indirectly, as is often the case with most tech companies. Investors should closely watch whether Palantir Technologies is renewing its existing government contracts or quietly losing some deals. New contract wins, especially in defense AI and NATO-related international programs, will also be an important sign of future growth. In addition, management’s comments about the federal pipeline will matter, as any change in tone could signal stronger or weaker demand ahead.

Below is a screenshot showing Palantir’s revenue breakdown across commercial and government segments.

3. Forward Guidance and Outlook

PLTR stock is down almost 22% year-to-date as software stocks face broader selling pressure and valuation concerns. Since PLTR trades at a premium multiple of over 100x earnings, strong future guidance matters just as much as current results.

The company needs to show continued revenue growth, strong demand for its AI platform, and confidence in future contracts to justify that valuation. If Palantir raises its full-year outlook, it could support the stock. But even one weak guidance update could make investors worry the stock is too expensive.

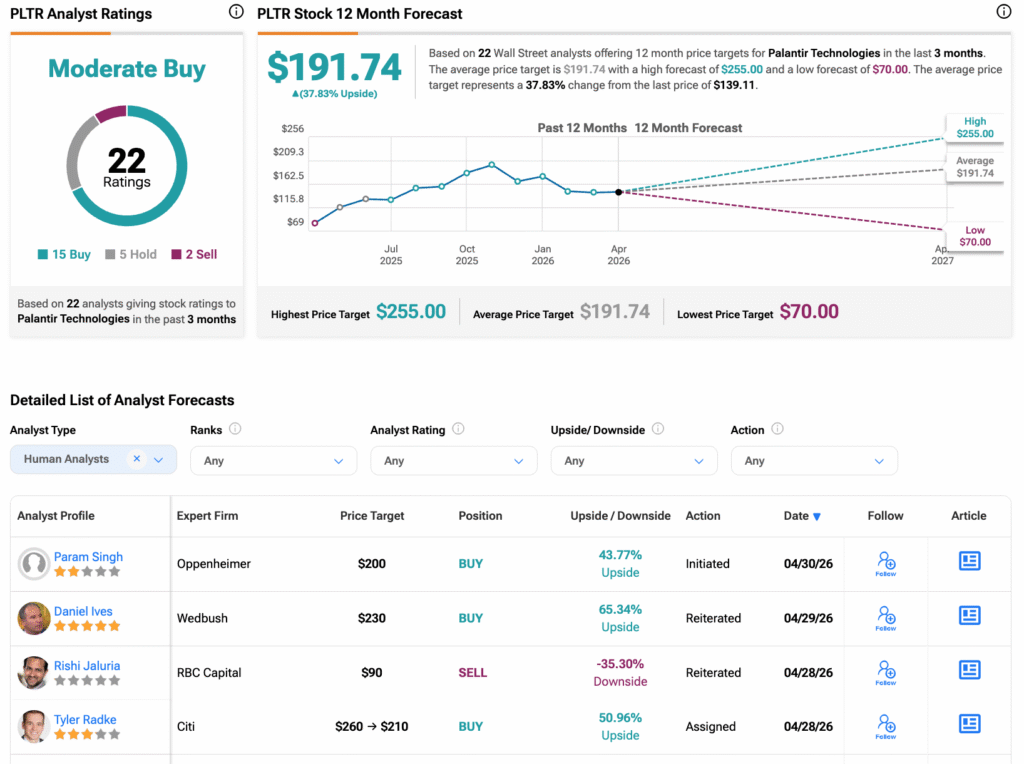

Is Palantir Stock a Buy?

Turning to Wall Street, PLTR stock has a Moderate Buy consensus rating based on 15 Buys, five Holds, and two Sells assigned in the last three months. At $191.74, the average Palantir stock price target implies an upside of 38% from current levels.